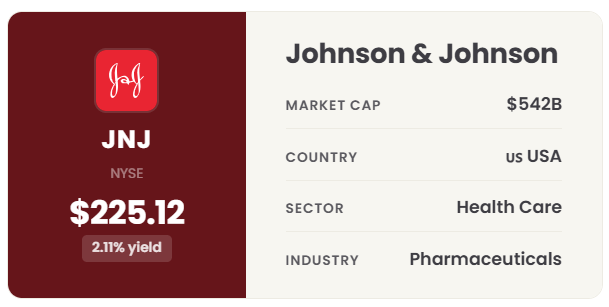

AAA-Rated. 64 Years of Raises. 26x Earnings. Is JNJ Still a Buy at $225?

This is a complete Dividend School member deep dive, unlocked in full so you can see exactly what membership delivers. Members get one of these every month. Analysis as of May 2026; prices and valuation reflect that date.

Dividend safety score of 85. Five-year P/E mean of 21.7x. One of those numbers is reassuring. The other isn't.

1. Business Overview

Johnson & Johnson is not the company it was five years ago. In August 2023, J&J completed the separation of its Consumer Health segment, the business that owned Tylenol, Listerine, Band-Aid, and Neutrogena, by spinning it off into an independent public company called Kenvue.

What remains is a pure-play, two-segment healthcare giant: a prescription-drug business called Innovative Medicine and a surgical-and-interventional-device business called MedTech.

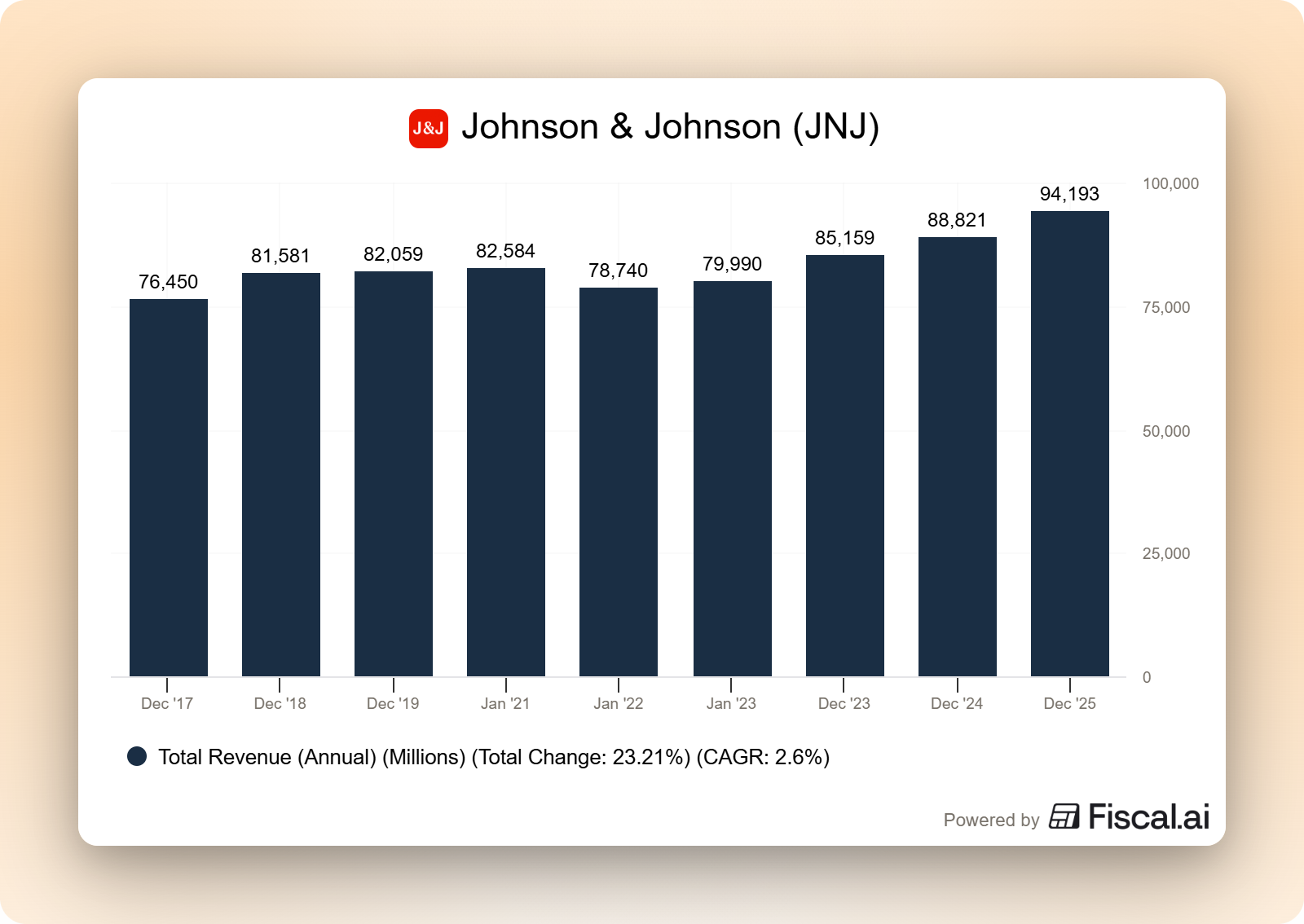

Together they generated $94.2 billion in revenue in fiscal year 2025, up from $78.7 billion in FY2021, with operating margins of 26.8% and free cash flow of $19.7 billion.

The Kenvue separation is the single most important strategic event in modern J&J history.

Consumer Health was the lowest-margin segment in the portfolio, and it carried the talc litigation overhang that had hung over the parent company for nearly a decade. By spinning it off, J&J shed approximately $15 billion of low-margin revenue and concentrated capital and management attention on the two segments where it could earn the highest returns: patent-protected prescription pharmaceuticals and surgical devices that lock in hospital customers.

The financial results are evident in the numbers: ROIC reached a five-year high of 17.0% in FY2025, and operating margins improved by roughly 200 basis points over the period despite gross margin compression from biosimilar competition and Medicare price negotiations.

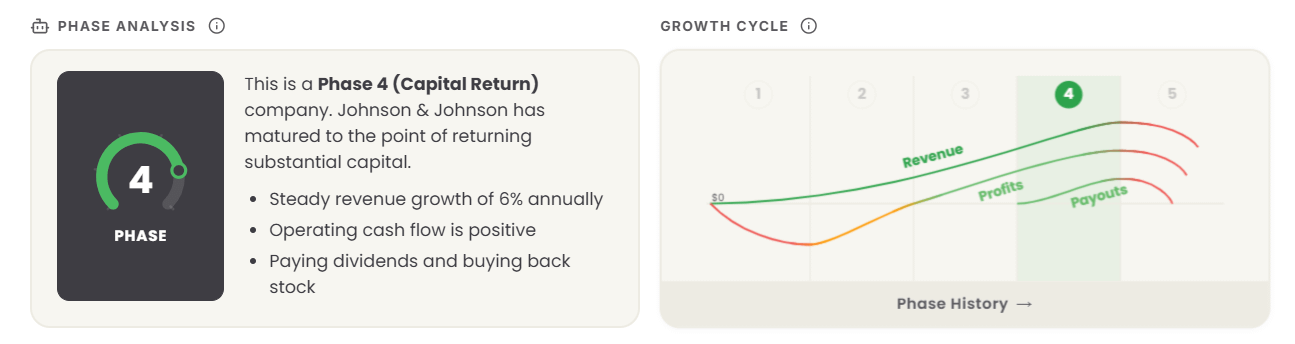

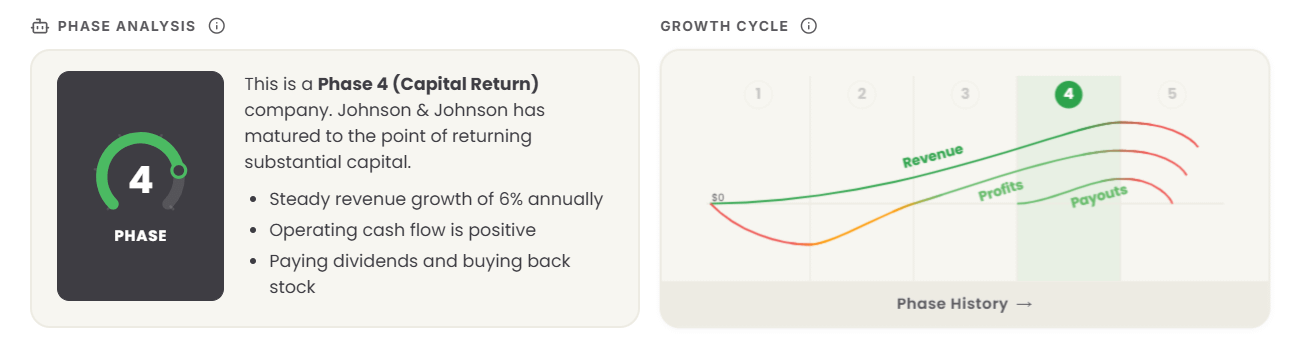

Stock Simplifier classifies JNJ as a Phase 4: Capital Return company, steady mid-single-digit revenue growth, consistently positive operating cash flow, and substantial capital being returned to shareholders through dividends and buybacks.

The composite Stock Simplifier score is 3.8 out of 5, with the Moat rated “Wide” (5), Management rated “Great” (5), Risk rated “Moderate” (3), Growth rated “Below Average” (2), and Valuation rated “Expensive” (2).

That mix is exactly what a serious dividend investor wants to evaluate: a high-quality, slow-growing, mature compounder where the question is not whether the business is durable, but whether you are paying the right price for the cash it produces.

For paid readers thinking about JNJ as a portfolio holding: this is a company built for the back half of a dividend portfolio, not the high-growth front. The investment case rests on three pillars, a wide moat that protects current cash flows, a Dividend King track record of 64 consecutive annual dividend increases, and a balance sheet strong enough to absorb both talc litigation outcomes and patent cliffs without threatening the dividend.

We will test each of those pillars in this analysis.

2. How They Make Money

JNJ earns revenue from two distinct sources, neither of which involves direct consumer relationships in any meaningful way. Understanding the channel structure is essential because it explains why margins, pricing power, and recession resilience look the way they do.

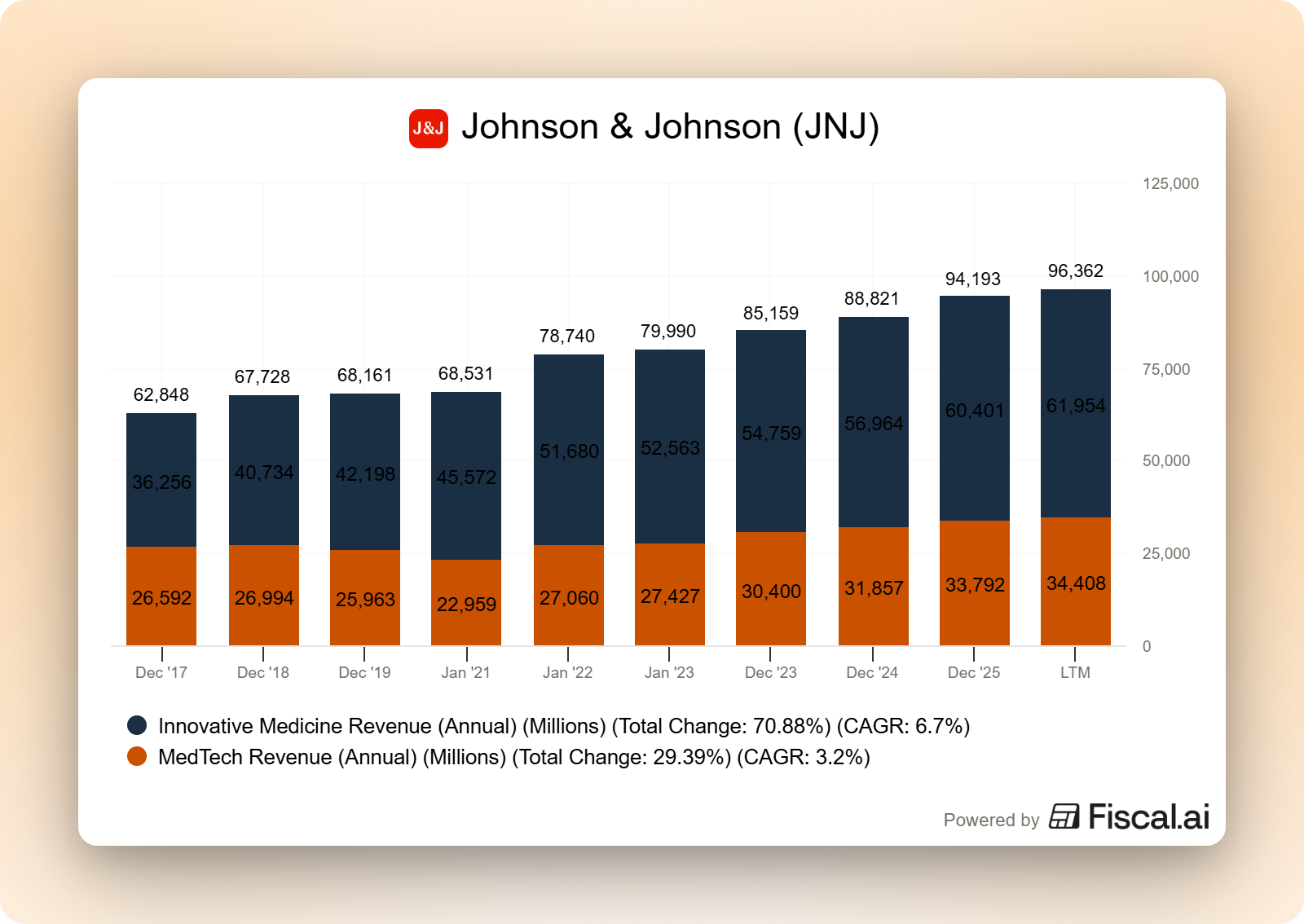

Innovative Medicine ($60.4B, 64% of FY2025 revenue, 84% of pre-tax profit). This is the prescription pharmaceuticals business, organized around five therapeutic areas: oncology, immunology, neuroscience, cardiovascular and metabolism, and pulmonary hypertension.

The customer chain here is institutional, not consumer. Physicians prescribe based on clinical evidence. Hospitals and retail pharmacies distribute. Insurance companies, pharmacy benefit managers (PBMs), and government payors (Medicare, Medicaid, national health systems abroad) decide reimbursement and ultimately pay. The patient receives the drug but rarely makes the purchasing decision. J&J’s commercial success depends on three things in this chain: clinical data strong enough to convince physicians, formulary access negotiated with payors, and lifecycle management of patents to protect pricing.

The marquee Innovative Medicine franchises in FY2025 were Darzalex (daratumumab) for multiple myeloma at $14.35 billion in sales (up 23% year-over-year), Stelara (ustekinumab) for immunology indications at $6.08 billion (down 41.3% as US biosimilars launched in January 2025), Tremfya (guselkumab) for psoriasis and Crohn’s disease at $5.2 billion (up 40.5% as J&J transitions Stelara patients), Erleada for prostate cancer, and Carvykti (CAR-T cell therapy for multiple myeloma) which is scaling rapidly from a small base.

Roughly two-thirds of Innovative Medicine revenue comes from chronic-disease therapies where patients refill prescriptions for months or years, creating predictable recurring revenue streams.

MedTech ($33.8B, 36% of revenue, 12% pre-tax margin). This segment sells surgical instruments, orthopedic implants, electrophysiology catheters, heart-recovery devices, and vision care products.

The customer is the hospital system or ambulatory surgery center. Purchasing decisions are made by a chain that includes surgeons (who have brand preferences and switching costs from retraining), hospital procurement teams (who negotiate aggressively on price), and group purchasing organizations (which aggregate demand across multiple facilities).

Key MedTech franchises include DePuy Synthes in orthopedic reconstruction (hips, knees, spine), Biosense Webster in electrophysiology mapping and ablation catheters, Abiomed in heart recovery (acquired 2022 for $16.6B), and Shockwave Medical in intravascular lithotripsy (acquired 2024 for $13.1B).

MedTech revenue is partly per-procedure (catheters, lithotripsy) and partly capital-equipment-and-consumables (orthopedic implants installed once, then served by follow-up parts and revisions).

Geographic mix (FY2025): United States $53.8B (57% of revenue), Europe $21.5B (23%), Asia-Pacific and Africa $14.0B (15%), Western Hemisphere ex-US $4.9B (5%).

The US weighting has increased modestly over five years from 55% to 57%, reflecting stronger pharma pricing and procedure volumes domestically combined with FX headwinds and tighter government pricing controls internationally.

The US is where JNJ commands the most pricing power and where its 67.9% gross margin is built; international revenue is lower-margin and structurally more constrained by national health system negotiation.

The two segments together generate roughly $94 billion of revenue from selling, in aggregate, into perhaps 6,000 hospital systems, tens of thousands of independent surgical centers, and a global prescribing physician base measured in the millions.

The recurring nature of chronic-disease prescriptions and the switching costs of standardized hospital implant systems are what give the business its predictability rating from Stock Simplifier and its place in this analysis.

3. Financials: Five-Year Look at the Three Statements

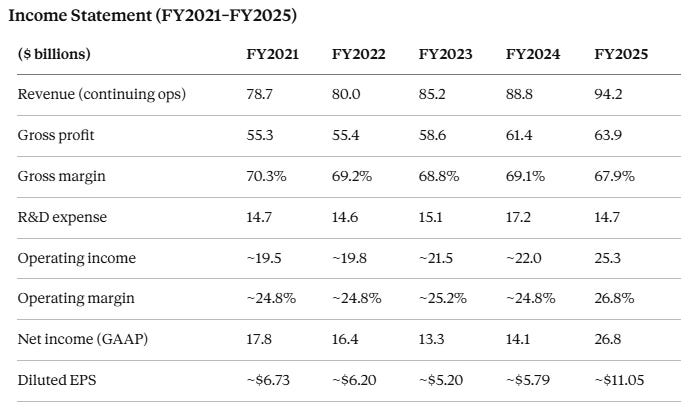

Note: Revenue figures shown on continuing-operations basis (excluding Consumer Health/Kenvue, which was separated in August 2023). Net income volatility in FY2022–FY2024 reflects talc-related litigation reserves and special items; FY2025 net income benefited from non-recurring items including spin-off accounting and tax adjustments. Source: JNJ Form 10-K FY2024 (filed Feb 2025) and Q4/Full-Year 2025 earnings release.

The top line grew at a 4.6% compound annual rate over four years. That number understates underlying momentum because the four-year window straddles the Kenvue separation, which removed roughly $15 billion of consumer health revenue.

On a clean continuing-operations basis, the remaining pharma-and-MedTech business has grown faster, Innovative Medicine compounded at 7.3% over four years and MedTech at 10.1% (boosted by the Abiomed and Shockwave acquisitions).

Gross margin compressed by 240 basis points across the period, primarily from Stelara biosimilar pressure and IRA-driven Medicare price negotiation.

The operating margin expansion to 26.8% in FY2025 came from cost discipline and operating leverage, not pricing — Stock Simplifier’s “sales change due to price” KPI registered -3.1% in FY2025, the most negative in the five-year dataset.

R&D spending of $14.7 billion in FY2025 (15.6% of revenue) is among the largest in pharma. The FY2024 spike to $17.2 billion reflected acquired in-process R&D from the Shockwave deal; the FY2025 figure of $14.7 billion is closer to underlying organic R&D run-rate.

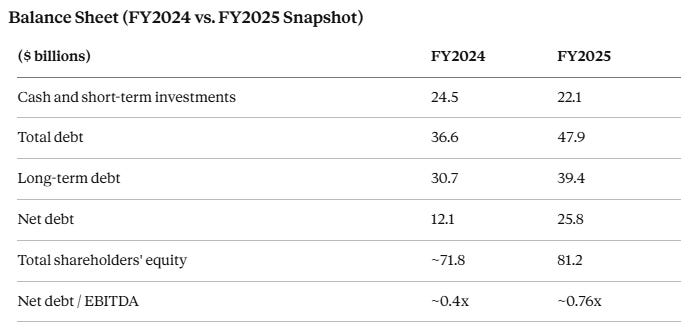

Balance Sheet (FY2024 vs. FY2025 Snapshot)

Source: JNJ 10-K FY2024, JNJ Q4 2025 earnings release.

The balance sheet story over the past two years is the deliberate use of leverage to fund MedTech consolidation.

Total debt rose from $36.6B at FY2024 year-end to $47.9B at FY2025 year-end as J&J financed the Shockwave Medical acquisition and other capital deployment. Even after that increase, net debt-to-EBITDA of 0.76x is investment-grade conservative, well below the 1.0x threshold that scores 100 in our dividend safety model.

Interest coverage remains north of 15x. J&J holds an AAA rating from S&P (one of only two US non-financial corporates with that rating).

The balance sheet, in short, has plenty of capacity to absorb both the remaining talc litigation and additional bolt-on M&A without endangering the dividend.

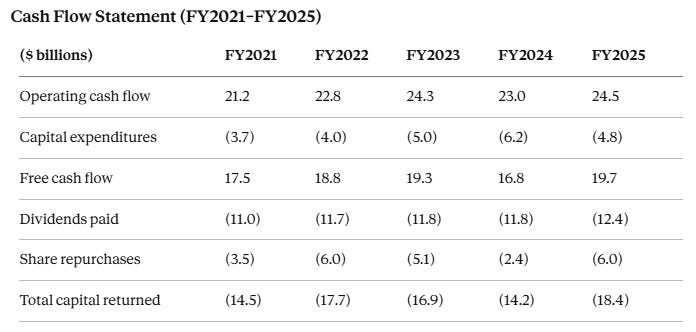

Cash Flow Statement (FY2021–FY2025)

Source: JNJ 10-K filings (FY2021–FY2024) and Q4/Full-Year 2025 earnings release. FCF = OCF – capex. Free cash flow margin in FY2025: 20.9%.

This is the most important table in the article for dividend investors. Three observations stand out.

First, free cash flow has averaged $18.4 billion annually over five years with low volatility — the coefficient of variation is approximately 0.054, well inside the “very stable” zone of our dividend safety model.

Second, dividends paid have grown every year, from $11.0B in FY2021 to $12.4B in FY2025, consuming roughly 63% of FY2025 free cash flow.

Third, total capital returned (dividends plus buybacks) of $18.4B in FY2025 represents 74.7% of operating cash flow and 93% of free cash flow — a textbook Phase 4 capital return profile. The remaining cash funds bolt-on M&A, with larger deals (like Shockwave at $13.1B) financed primarily with debt.

The combination of high gross margins, stable FCF, conservative leverage, and a 64-year dividend growth streak is the financial foundation of the entire investment thesis. We will return to these numbers in the dividend strength section.

In August 2023, Johnson & Johnson did something no $400B+ company had done in a generation: it spun off its single most recognizable business. Tylenol. Listerine. Band-Aid. Neutrogena. Gone, packaged into a new company called Kenvue and sent on its way.

What’s left is leaner, higher-margin, and harder to evaluate. Two segments instead of three. Patent-protected drugs and surgical devices. No more consumer brands, no more talc on the balance sheet (legally, though, as you’ll see, that protection has been less complete than designed).

For dividend investors, the question is simple: is the new JNJ still the dividend fortress the old JNJ was? 64 years of consecutive raises says yes. A 26x P/E against a 5-year average of 21.7x and a free cash flow payout that just crossed 60% say not so fast.

In this 6,000-word paid analysis, I work through every section a serious DIY investor needs: business, financials, moat, management, risks, growth, dividend score, and valuation. By the end, you’ll know exactly what to do with JNJ at $225.

🔒 Read the full breakdown below ↓

4. Moat and Competitive Position

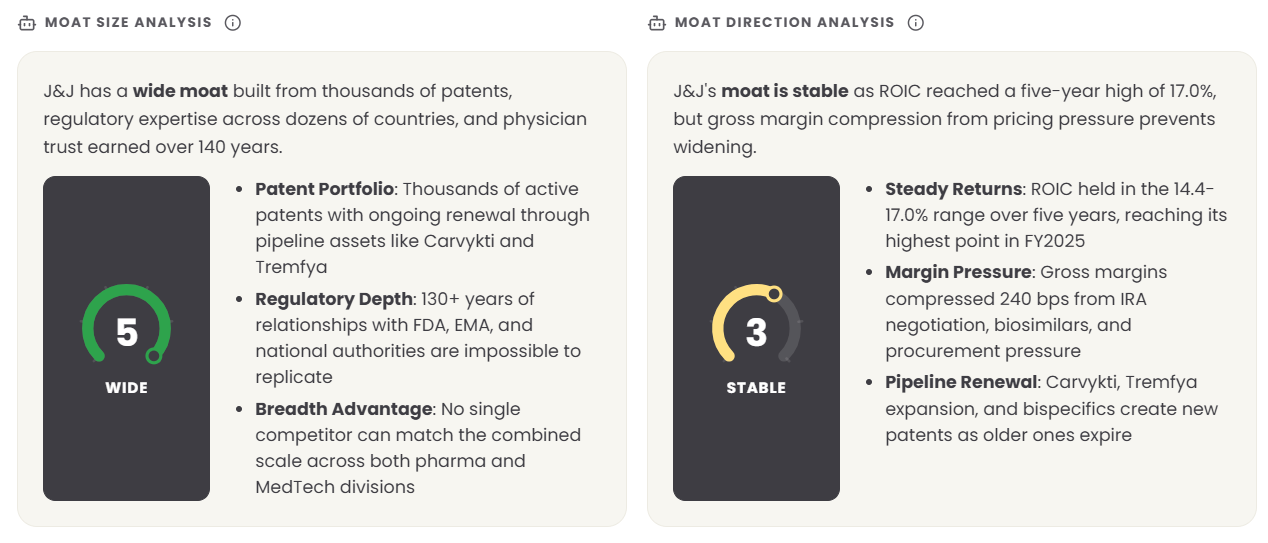

Stock Simplifier rates JNJ’s moat as Wide (5/5) with Stable (3/5) direction, strong protection, but not currently widening.

Drilling into the moat sources, the strongest pillar is intangible assets (patents and regulatory expertise), the second is switching costs in MedTech (moderate rather than high), and the weakest are network effects and low-cost production, neither of which apply to JNJ in any material way.

The “counter-positioning” pillar is flagged as a moderate risk because newer entrants in CAR-T cell therapy and oral immunology drugs could eventually counter-position against J&J’s existing biologics franchises.

The patent portfolio is the largest single moat asset.

J&J holds thousands of active patents across small molecules, biologics, and cell therapies, with continual renewal as new drugs reach commercial approval. The economics are simple: a patent-protected drug like Darzalex earns roughly 80%+ gross margins for the duration of exclusivity, then faces biosimilar competition that compresses pricing by 50–70% over the following two-to-three years.

The Stelara situation is the live case study, peak revenue of roughly $11 billion in 2024, biosimilar entry in January 2025, FY2025 revenue down to $6.08 billion (a 41% drop in one year).

This is the patent cliff in real time.

J&J’s defense is pipeline renewal: Tremfya growing 40%+ as it captures transitioning Stelara patients, Darzalex Faspro extending the multiple myeloma franchise to roughly 2035 patent protection, and the Carvykti CAR-T platform building durable franchise value.

Regulatory expertise is the second-strongest intangible. J&J has 130+ years of relationships with the FDA, EMA, and national health authorities in dozens of countries. Approval timelines, label expansion negotiations, and post-marketing surveillance are areas where institutional knowledge compounds. A new entrant cannot replicate this in less than a decade of building infrastructure.

In MedTech, the moat is structurally different.

Switching costs are moderate because once a hospital standardizes on J&J’s DePuy Synthes knee implant system or Biosense Webster electrophysiology catheters, surgeons must retrain on competing platforms and procurement must restock inventory.

The friction is real but bounded, hospitals do switch when better technology arrives, especially in newer categories. The MedTech moat is also reinforced by surgeon training programs and procedure-specific consumables that lock in recurring per-procedure revenue.

Key Competitors

The competitive set differs by segment because no other major healthcare company has J&J’s exact pharma-plus-MedTech combination.

In Innovative Medicine, the primary competitors are AbbVie (ABBV) in immunology with Humira’s successor Skyrizi and Rinvoq directly competing with Tremfya, Bristol Myers Squibb (BMY) in multiple myeloma with carfilzomib and competing CAR-T (Abecma), Pfizer (PFE) and Merck (MRK) as broad-line oncology and immunology peers, and Eli Lilly (LLY) as the highest-multiple competitor benefiting from GLP-1 weight-loss drug demand.

J&J does not currently have a GLP-1 entrant of consequence, which is one reason its top-line growth screens below pharma peers.

In MedTech, the primary competitors are Medtronic (MDT) across the device spectrum, Stryker (SYK) in orthopedics and surgical instruments, Boston Scientific (BSX) in cardiovascular and electrophysiology (a fast-growing direct competitor in EP), Abbott (ABT) in vascular and structural heart, and Intuitive Surgical (ISRG) in surgical robotics, where J&J’s Ottava platform faces an entrenched incumbent with an installed base measured in tens of thousands of da Vinci systems.

The Ottava delay is the single most discussed competitive vulnerability in MedTech analyst coverage.

What ultimately separates J&J from each of these competitors is breadth.

Pure-play pharma companies cannot replicate the device diversification. Pure-play device companies cannot replicate the pharma profitability. The cross-segment scale enables capital allocation flexibility, J&J can deploy proceeds from a Stelara biosimilar transition into Shockwave Medical without raising capital or shifting strategy.

That combination is rare among healthcare peers, and it is the structural reason Stock Simplifier rates the competitive position Dominant.

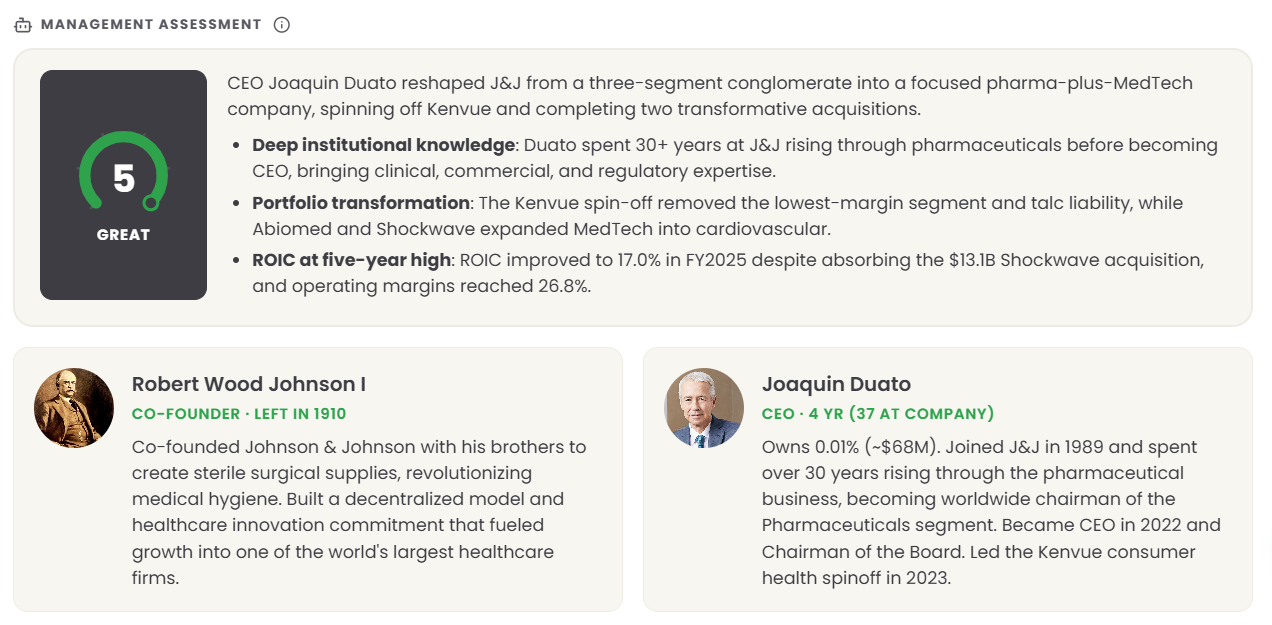

5. Management and Incentives

Stock Simplifier rates Management Great (5/5), the highest band on its framework. The case rests on three points: deep institutional knowledge, a track record of portfolio transformation, and demonstrated capital allocation discipline.

Joaquin Duato is the CEO, having taken the role in January 2022 and added the Chairman role in January 2023.

He has been with J&J for 37 years, joining in 1989 and rising through the pharmaceutical division, eventually serving as worldwide chairman of Pharmaceuticals before becoming CEO.

His tenure has been defined by the Kenvue spin-off (completed August 2023) and two transformative MedTech acquisitions, Abiomed in December 2022 for $16.6 billion, and Shockwave Medical in May 2024 for $13.1 billion. Both were aimed at expanding the cardiovascular footprint within MedTech, and both have generated revenue growth at or above the price paid.

The Kenvue separation is the most consequential portfolio decision in modern JNJ history, and it was Duato’s call to make.

The move removed talc litigation from the parent’s balance sheet (legally, through the Kenvue subsidiary structure, though as we will discuss in the risks section, the legal protection has been less complete than initially designed), eliminated the lowest-margin segment, and concentrated capital on higher-return businesses.

Operating margins expanded by roughly 200 basis points over the period, and ROIC reached a five-year high of 17.0% in FY2025 despite absorbing the $13.1B Shockwave acquisition. By the simplest measurement did capital deployment improve returns on capital?

The answer over Duato’s tenure is unambiguously yes.

CEO compensation and alignment. Per J&J’s 2024 proxy statement, Duato’s total 2024 compensation was $24.3 million, a 14% decrease from $28.4 million in 2023. The package included $1.6 million salary, $10.8 million in stock awards, $4.9 million in option awards, approximately $4.0 million in cash bonuses, and $2.7 million in pension value change.

The CEO pay ratio of 293:1 versus the median JNJ employee places JNJ in the middle of the S&P 500 distribution, high in absolute terms but not unusual for a $542B market cap pharmaceutical company.

Duato’s direct stock ownership is approximately 0.01% of shares outstanding, valued at roughly $68 million at recent prices. That ownership stake represents close to three years of total compensation, high enough to align meaningfully with shareholders, but not high enough to constitute “founder economics.”

The structure of compensation skews toward stock and options that vest over multiple years, which builds alignment over time.

The board includes ten independent directors and follows standard governance practices including annual director elections, majority voting, and an independent lead director. There has been no recent controversy on executive compensation, governance, or board composition that would change the assessment.

Combined with the operational track record, Stock Simplifier’s “Great” rating reflects a management team that has demonstrably created value through portfolio reshaping over the past four years.

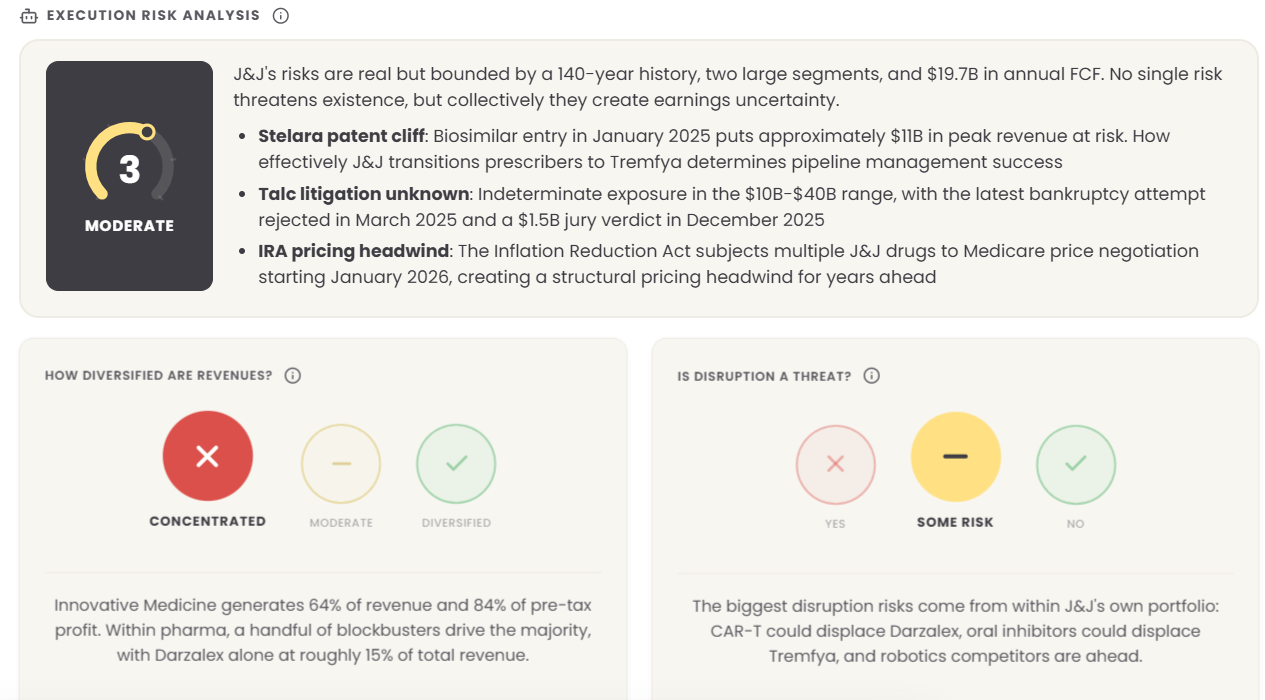

6. Key Risks

Stock Simplifier rates Risk Moderate (3/5), with the qualifier that “no single risk threatens existence, but collectively they create earnings uncertainty.” Three risks dominate the analysis, and a fourth, revenue concentration, is worth flagging as a structural feature rather than a near-term shock.

Stelara patent cliff. Stelara lost US exclusivity in January 2025. FY2025 sales fell 41.3% to $6.08 billion from $10.36 billion in FY2024, and the franchise is expected to continue declining over FY2026-FY2027 as additional biosimilar manufacturers gain market share.

The peak revenue at risk is roughly $11 billion.

The mitigation is Tremfya, which grew 40.5% in FY2025 to $5.2 billion as J&J’s commercial team transitioned Stelara prescribers to the next-generation IL-23 inhibitor.

If Tremfya reaches the $10 billion annual revenue management has guided toward, it will fully replace Stelara’s peak contribution. If it falls short, for instance, if AbbVie’s Skyrizi captures more transitioning patients than expected, the Innovative Medicine growth rate slows materially through 2027.

Talc litigation. This is the most idiosyncratic and least quantifiable risk. J&J has attempted three separate bankruptcy filings to consolidate talc claims under a single settlement, all of which have been rejected by federal courts. The most recent attempt, a $9 billion proposed settlement, was rejected in March 2025 on the grounds that the voting process was flawed.

With bankruptcy off the table, claims now proceed through the tort system. Recent verdicts include a $1.5 billion Baltimore jury verdict in December 2025, a $966 million Los Angeles verdict ($16M compensatory plus $950M punitive), and a $20 million Florida verdict. Approximately 90,000 lawsuits remain pending. Estimates of total exposure range from $10 billion to $40 billion depending on settlement assumptions and the fate of punitive damages on appeal.

J&J generates approximately $19.7 billion of free cash flow annually, so even the high end of the exposure range can be absorbed over several years without endangering the dividend, but the uncertainty drags on the multiple and on management attention.

IRA Medicare price negotiation. The Inflation Reduction Act subjects multiple J&J drugs to direct Medicare price negotiation, with negotiated prices taking effect January 2026 for the first cohort (which includes Stelara, Xarelto, and Imbruvica). Additional drugs join the negotiation list in subsequent years.

The structural effect is a permanent downward step-change in net realized pricing for covered drugs, and lifecycle returns from future drug development are necessarily lower than they would have been under the pre-IRA framework.

This is not a single-year event; it is a multi-year compression of pharma margins across the industry, with J&J bearing a meaningful share given the size of its US Medicare-exposed portfolio.

Revenue concentration. Stock Simplifier flags revenue as Concentrated, Innovative Medicine generates 64% of revenue and 84% of pre-tax profit, and within pharma, a handful of blockbuster drugs drive most of the contribution. Darzalex alone accounts for roughly 15% of the company’s total revenue.

This is structural concentration, not a near-term risk per se, but it means that a setback in any single major franchise (Darzalex label expansion failure, a competitive surprise from a CAR-T entrant, a Carvykti manufacturing-scale issue) would have an outsized effect on earnings.

Disruption risk. Stock Simplifier rates disruption as Some Risk, and the most interesting framing is that the biggest disruption threats come from within J&J’s own portfolio. CAR-T cell therapies (J&J’s Carvykti, plus competitors like Bristol Myers’ Abecma) could eventually displace Darzalex if they prove more durable. Oral IL-23 inhibitors in development could displace injectable Tremfya. Surgical robotics competitors are ahead of J&J in commercialization.

None of these is imminent, but the strategic question for the next decade is whether J&J can lead the technologies that disrupt its own franchises before competitors do.

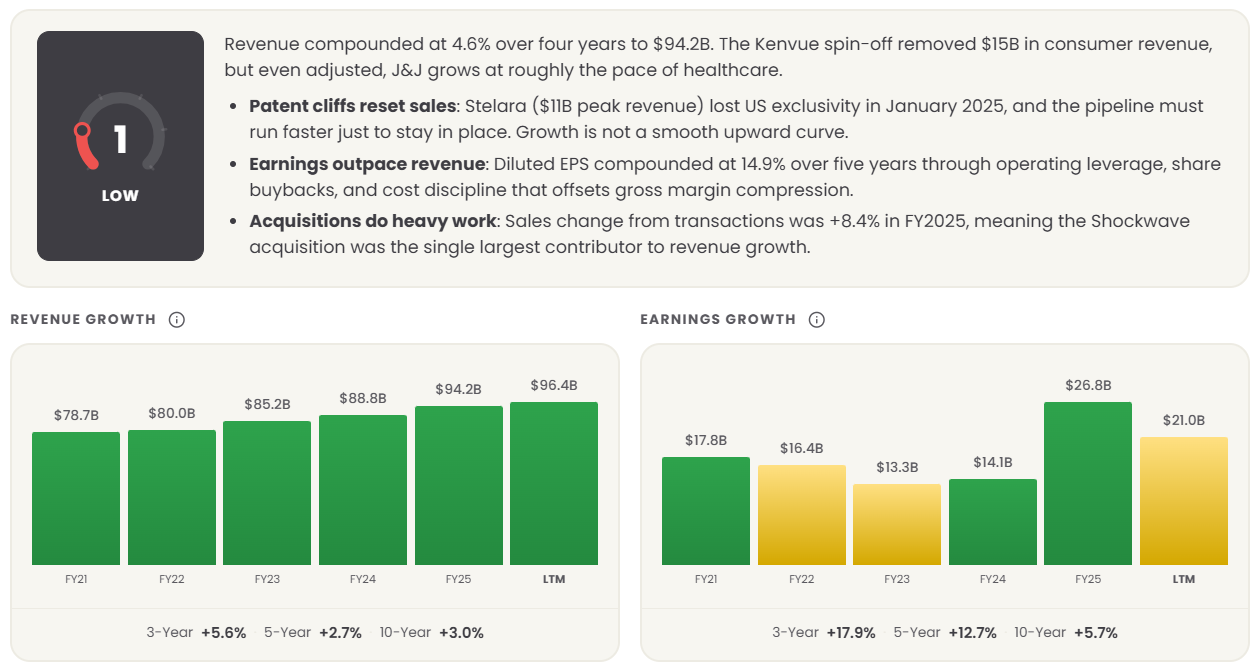

7. Future Growth Prospects

Stock Simplifier rates Growth Below Average (2/5), which warrants the most discussion because it is the most likely source of disagreement between bulls and bears.

The historical numbers tell the story.

Revenue compounded at 4.6% over four years on a continuing-operations basis. The three-year revenue CAGR was 5.6%, the five-year was 2.7% (depressed by Kenvue divestiture), and the ten-year was 3.0%.

Diluted EPS compounded faster, the five-year CAGR was 12.7% and the three-year was 17.9%, but that gap reflects operating leverage, share buybacks, and one-time items rather than underlying top-line acceleration. For a $94B revenue business operating in pharma and devices (both 5–7% secular growth markets), mid-single-digit top-line growth is structurally normal.

JNJ is not gaining significant market share in aggregate; it is growing at roughly the rate of its addressable markets.

The Stelara patent cliff is the single largest near-term drag. Roughly $5 billion of revenue is at risk over FY2025-FY2027 as biosimilar competition compresses Stelara’s franchise from $10.4B in FY2024 toward perhaps $2–3B by FY2027. The pipeline must run faster just to hold Innovative Medicine flat through that transition, let alone grow it.

The growth drivers are real but bounded.

Darzalex is the single most important growth driver, with FY2025 revenue of $14.35 billion growing 23% year-over-year. Label expansion into earlier lines of multiple myeloma treatment is the primary lever, and the franchise’s patent protection now extends to roughly 2035 via the subcutaneous Faspro formulation. Growth in the mid-teens is plausible through FY2028, with deceleration as the franchise approaches saturation.

Tremfya at $5.2 billion in FY2025 (+40.5%) is positioned as the immunology successor to Stelara. The transition depends on how effectively J&J captures its existing Stelara prescribers versus losing them to AbbVie’s Skyrizi and Rinvoq. Management has guided Tremfya toward $10 billion peak revenue, which would require maintaining 15–20% annual growth for the next three to four years.

Carvykti (CAR-T for multiple myeloma) is in early commercialization. Manufacturing complexity limits the pace of scale-up, each dose is custom-made from the patient’s own cells, but also creates competitive barriers. Label expansion into earlier lines of treatment is the lever. If Carvykti becomes a frontline or second-line standard, it could become a $5–10 billion franchise by FY2030.

MedTech acquisitions and organic growth. MedTech grew at a 10.1% four-year CAGR, roughly half from acquisitions and half organic. Going forward, organic growth of 6–8% supplemented by bolt-on M&A is the realistic base case. The Shockwave Medical acquisition added intravascular lithotripsy, a category growing in the high teens.

The Ottava surgical robotics program, if it reaches commercialization, would address a $20B+ market dominated by Intuitive Surgical. This is the largest single optionality bet in the MedTech portfolio, with a wide range of outcomes from transformative to write-off.

Pipeline catalysts. Multiple late-stage assets could move the needle: nipocalimab for generalized myasthenia gravis (FDA-approved as Imaavy in 2025), icotrokinra (oral IL-23 inhibitor for psoriasis, NDA submitted), amivantamab for non-small-cell lung cancer in expanded indications, and ongoing TALVEY (bispecific antibody) commercialization in multiple myeloma.

Each could become a multi-billion dollar franchise if approved and commercially successful.

Industry growth. The global pharmaceutical market grows at 5–7% annually, driven by aging populations, oncology and immunology innovation, and emerging market access expansion. The medical device market grows at a similar 5–7%, driven by procedure volume increases and minimally invasive technology adoption.

J&J’s blended growth rate roughly matches these underlying markets. Neither pharma nor devices offer the secular tailwinds of cloud computing or e-commerce, there is no scenario in which JNJ becomes a 15%+ compounder.

The honest bottom line for paid readers: this is a 4–6% organic top-line grower with 8–12% EPS growth potential through buybacks and operating leverage. That is not a growth stock by any reasonable definition.

It is a high-quality compounder priced for dividend income and capital preservation. If the Stelara-to-Tremfya transition executes cleanly and Darzalex maintains its trajectory through FY2028, the growth profile is defensible. If either falters, the multiple compresses.

8. Dividend Strength: Applying the Dividend Score

This is the section paid readers came here for. We apply our proprietary five-category dividend safety score to JNJ FY2025 and benchmark against the methodology’s worked examples.

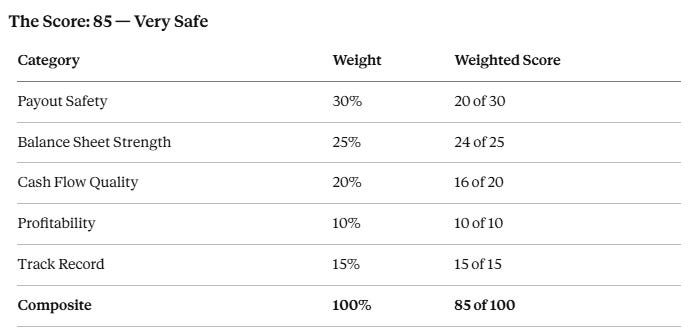

The Score: 85 — Very Safe

Component Breakdown

EPS Payout Ratio: 47% → Score 80. Dividend per share of $5.14 against FY2025 diluted EPS of approximately $11.05. This is comfortably within the safe zone, but not pristine; anything below 30% would score 100. The metric is somewhat distorted by FY2025’s elevated net income (which included favorable one-time items); on normalized earnings, the payout ratio is closer to 55–60%, which would still score 60–80.

FCF Payout Ratio: 63% → Score 60. Dividends paid of $12.4B against free cash flow of $19.7B. This is the weakest single metric in the score and the one to watch most carefully. A score of 60 (between 60% and 75% FCF payout) means dividend coverage is adequate but not abundant. The buyback program, at $6.0 billion in FY2025, sits ahead of the dividend in capital priority order, providing a buffer that could be reduced if cash flow tightens. The combined dividend-plus-buyback consumed 93% of FY2025 FCF, which is normal for a Phase 4 company but leaves little margin if a single bad year hits.

Net Debt / EBITDA: 0.76x → Score 100. Net debt of approximately $25.8B against EBITDA of approximately $34B. Even after the Shockwave acquisition pushed total debt above $47B, the leverage ratio remains well inside the conservative band. AAA credit rating from S&P validates this.

Interest Coverage: ~20x → Score 100. EBIT of $25.3B against interest expense of approximately $1.2–1.5B. Comfortably above the 15x threshold for top score. Even with the recent debt run-up, this metric has a substantial cushion.

Cash / Annual Dividend: 1.78x → Score 80. Cash and short-term investments of $22.1B provides 1.78 years of dividend coverage from cash alone. Above the 1.5x threshold but below the 2.0x threshold for top score. This buffer is more than adequate for any plausible short-term operational stress.

FCF 5-Year CAGR: ~4% → Score 60. Free cash flow growth on a continuing-operations basis has been modest, in line with the business’s overall mid-single-digit growth profile. This is the second-weakest metric and reflects the same growth concerns that are flagged in the broader analysis.

FCF Volatility (Coefficient of Variation): 0.054 → Score 100. Free cash flow has ranged from $16.8B to $19.7B over five years, an extraordinarily tight band. The CoV of 5.4% is well inside the “very stable” category and reflects the recurring-prescription, recession-resilient nature of the business.

Operating Margin 3-Year Δ: +2pp → Score 100. Operating margin improved from approximately 24.8% in FY2022 to 26.8% in FY2025, a meaningful expansion driven by post-Kenvue mix shift and cost discipline.

ROIC: 17.0% → Score 100. A five-year high, well above the 15% threshold for top score, even after absorbing the Shockwave acquisition. This is the strongest evidence that capital is being deployed at returns above the cost of capital.

Consecutive Years of Dividend Growth: 64 → Score 100. JNJ is a Dividend King, having raised its dividend annually since 1962. This is the longest streak in the S&P 500 healthcare sector. The most recent increase was approximately 4.8% in April 2025 (a $ 0.10 quarterly bump). Only a handful of companies in any sector can claim this consistency.

Recession Behavior: Grew Both → Score 100. JNJ raised its dividend through both the 2008–2009 Global Financial Crisis and the 2020 COVID pandemic. The underlying business proved recession-resilient in both periods.

Hard Floor Check

The FCF payout ratio of 63% is well below the 100% hard-floor threshold that would cap the composite at 40. No floor applied.

Interpretation

A composite score of 85 places JNJ in the “Very Safe” bucket, the top tier of the methodology’s four buckets. The score is consistent with the worked example in the dividend safety model (which scored JNJ FY2023 at approximately 83). The two metrics holding the score back from 90+ are the FCF Payout Ratio (60) and the FCF 5-year CAGR (60), both of which reflect the same underlying tension: JNJ generates abundant but not rapidly growing cash flow, and the dividend consumes a meaningful share of it.

What this means for paid readers: the probability of a dividend cut over the next one to three years is very low.

The probability of a dividend freeze (no increase in a given year) is also low but not zero, a worst-case combination of accelerated talc settlements, slower-than-expected Tremfya ramp, and IRA pricing compression could compress FCF enough to force a pause. The probability-weighted base case remains 4–6% annual dividend growth, in line with the historical pace.

Dividend Growth and Yield Context

2020: $4.04 per share

2021: $4.24 (+5.0%)

2022: $4.45 (+5.0%)

2023: $4.70 (+5.6%)

2024: $4.91 (+4.5%)

2025: $5.14 (+4.7%)

2026 annualized: $5.20

The five-year dividend per share CAGR is 4.9%, in line with revenue growth and below the EPS growth rate, leaving room for continued increases. The current yield of 2.11% is slightly below the five-year average of approximately 2.7%, reflecting the share price appreciation of FY2025-FY2026 rather than dividend underperformance.

A holder buying today at $225 is getting roughly the lowest yield JNJ has offered in over a decade, which sets up the valuation question.

9. Valuation

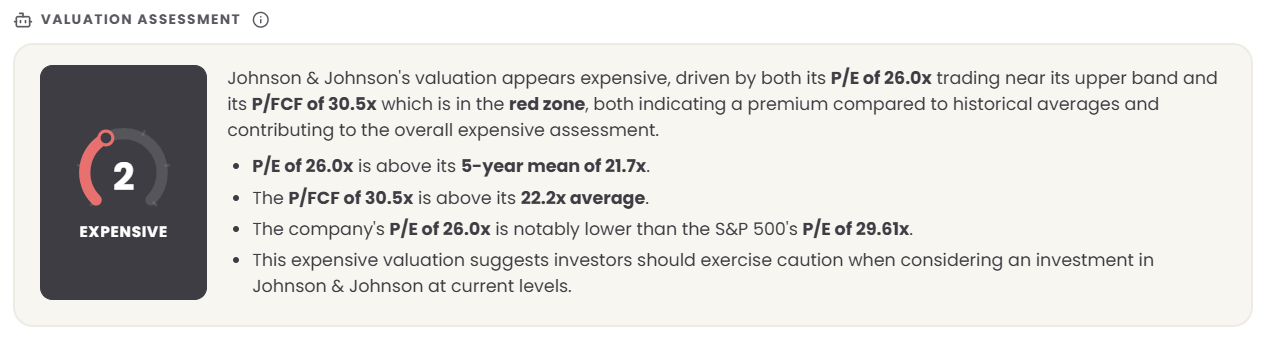

Stock Simplifier rates Valuation Expensive (2/5), which is the second-most-discussed point in the composite (behind growth). The Stock Simplifier framework anchors on three multiples.

P/E of 26.0x is above the 5-year mean of 21.7x. Using GAAP earnings, this is a 20% premium to JNJ’s own recent history. On a normalized basis (smoothing the FY2022-FY2024 talc-related earnings drag), the comparison is closer to a 15% premium.

Either way, the stock trades above its recent multiple band, not within it. The context, the P/E of the S&P 500 itself is 29.6x — means JNJ is cheaper than the market on this metric, but more expensive than its own history.

P/FCF of 30.5x is above the 22.2x five-year average. This is the more concerning multiple for dividend investors because free cash flow is what funds the dividend. At 30.5x FCF, the implied free cash flow yield is 3.3%.

A dividend-and-buyback program consuming $18.4B annually represents a 3.4% total shareholder yield (2.1% dividend + 1.1% buyback at current prices), which approximately matches the FCF yield. There is no meaningful margin for FCF multiple expansion at these levels.

P/E of 26.0x versus the S&P 500’s 29.6x. This is the bull case framing. JNJ trades at a 12% discount to the broader market despite offering higher quality (Wide Moat, Phase 4 capital return, 64-year dividend track record).

On relative valuation terms, the stock is reasonably priced, not aggressively priced.

Synthesis: The honest read is that JNJ is no longer cheap and is not yet expensive in the way a clearly overvalued stock would be.

The five-year P/E band has averaged roughly 17x-22x; the current 26x is at the upper end. Total return over a five-year holding period from current prices likely consists of approximately 2% dividend yield, 1% buyback yield, 4–6% EPS growth, and possibly -1% to -2% multiple compression as the P/E normalizes toward its five-year average.

The midpoint is therefore a 5–8% annualized total return, adequate for a dividend portfolio, but not the double-digit returns available when JNJ traded at 15x earnings in late 2024.

For paid readers framing entry decisions: the stock is buyable for dividend-focused, long-term portfolios at current levels, but the margin of safety is thinner than it has been at most points over the past three years.

A pullback to the $190–$200 range would reset the P/E toward the five-year mean and substantially improve the implied total return.

10. Takeaway

Johnson & Johnson is the single highest-quality dividend stock most paid readers will own, and Stock Simplifier, our dividend safety model, and the FY2025 financials all agree on that. The Wide moat, Great management, 17.0% ROIC, 64-year dividend growth streak, AAA credit rating, and 0.76x net debt to EBITDA combine into a profile that is hard to replicate among the 11,000 public US companies.

The dividend safety score of 85 (Very Safe) confirms the dividend is durable.

The Stelara cliff is real and visible in FY2025 numbers, but the Tremfya transition is executing, the Darzalex franchise is compounding, and the cash flow base is more than sufficient to absorb the talc litigation and pipeline transitions simultaneously.

The two things that are not great about JNJ today are growth and price.

Stock Simplifier’s Below Average growth rating and Expensive valuation rating are deserved. A 4–6% revenue grower at 26x earnings does not produce 12%+ annual returns. It produces 5–8% annual returns with extremely high probability, exactly the profile a dividend-oriented portfolio should welcome, but at a price that demands a long holding period to compound.

The verdict for paid readers:

For existing JNJ holders: continue holding. The dividend safety score, balance sheet strength, and pipeline progress justify staying in the position. The current valuation does not warrant trimming for someone with a 5-year+ horizon.

For investors building a new position: scale in over time rather than buying a full position at $225. A 1%–3% initial position with the balance allocated on pullbacks below $200 would improve the entry multiple and the implied yield.

For investors looking for above-market total returns: JNJ is not the vehicle. Look elsewhere. This stock is a portfolio anchor, not a return driver.

The next twelve months will be defined by three signals worth watching closely: (1) Innovative Medicine segment revenue growth through the Stelara cliff, does the Tremfya/Darzalex/Carvykti trio more than offset the biosimilar drag, (2) talc litigation settlement progress or punitive damages on appeal, which will determine whether the overhang clears or extends, and (3) capital allocation discipline, does the buyback persist near $6B annually, signaling management confidence in the cash flow base. A dividend increase in April 2026 of roughly 4–5% would confirm the trajectory and extend the streak to 65 consecutive years.

This is the textbook Phase 4 healthcare compounder. Pay the right price for it, and it does exactly what a dividend portfolio anchor is supposed to do for the next decade.

That’s a complete Dividend School deep dive. Business, financials, moat, management, risks, growth, dividend safety score, and a valuation with a verdict at the end.

Members get one of these every month, on a stock from my 30-stock Dividend Universe.

This month’s member deep dive covers a consulting giant down 55% from its high, sitting on a net-cash balance sheet, still raising its dividend double digits.. That one stays behind the paywall. This one is yours free, so you know exactly what you’re buying before you spend a dollar.

Here’s what membership includes:

5 Buy First stocks. My highest-conviction dividend picks, the ones I’d buy first if I were starting today.

5 Best Buys every month. Name, yield, thesis, and a Buy Below price on each one.

The full Dividend Universe. Every stock I track, with its safety score and fair value.

The monthly deep dive. The full workup you just read, on a new company every month.

One premium email every week, on a schedule you can set your watch by.

$369 a year or $35 a month, with a 30-day money-back guarantee. If it’s not for you, email me and I’ll refund every dollar. No forms, no friction.

Already a member? The current deep dive is waiting in your library.

Excellent write up