Why Warren Buffett Ignores Earnings (And What He Focuses On Instead)

Most investors are looking at the wrong number.

They obsess over Earnings Per Share.

But earnings are a matter of opinion.

Cash, however, is a cold, hard fact.

I'm going to show you the three-step cash flow filter that separates durable, compounding businesses from the rest.

Start by ignoring the income statement.

At least at first.

Aswath Damodaran calls earnings the "gossamer of accounting."

They are a story, shaped by rules and assumptions.

The cash flow statement is the evidence.

It’s the truth serum for a business.

Earnings include non-cash expenses like depreciation.

Aggressive accounting can make a company look profitable.

But if it isn't generating cash, it's on life support.

This is why the world's best investors start with cash.

It cuts through the fog.

It reveals the true economic engine of a company.

So, how do we measure the cash that truly matters?

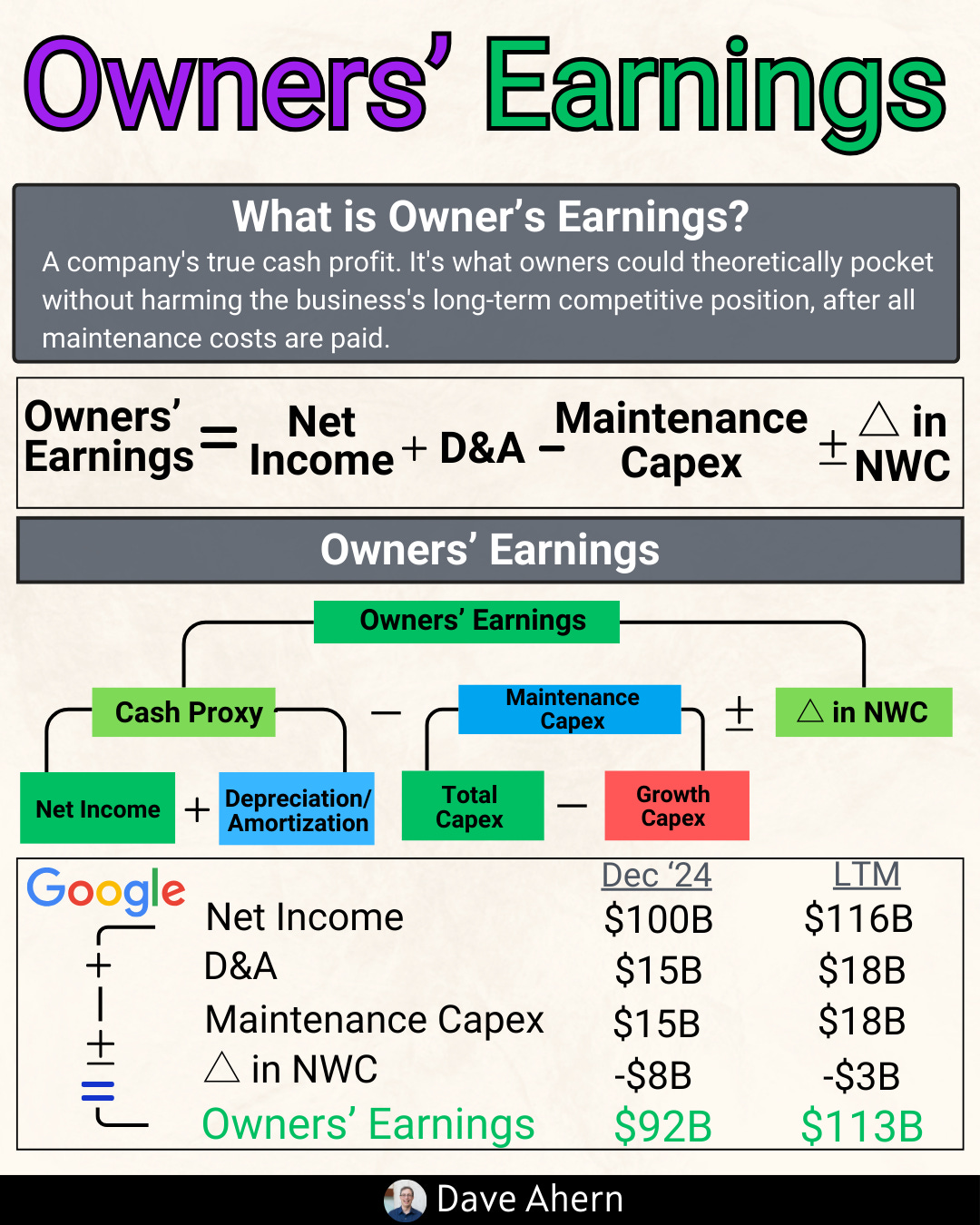

Warren Buffett’s Owner Earnings

You need to calculate what Warren Buffett calls "Owner Earnings."

This is the real prize.

It gets you closer to the cash an owner could pocket at the end of the year.

The standard Free Cash Flow formula can be misleading.

It doesn't distinguish between essential spending and growth spending.

The simple formula is: Cash from Operations - Capital Expenditures.

The problem is this mixes maintenance capex with growth capex.

A better way: Find "maintenance capex" in the filings. This is the cost to simply stand still.

Owner Earnings = Operating Cash Flow - Maintenance Capex.

This is your baseline.

It’s the true cash profit of the business.

Once you have this number, the real analysis begins.

This is the first of three filters.

Great businesses are cash-generating machines.

They do it year after year, like a metronome.

This consistency proves they have a durable competitive advantage.

It's the clearest sign of a strong economic moat.

Pull the last 10 years of Owner Earnings you calculated.

Is the number positive and, ideally, growing?

A single negative year isn't a dealbreaker, but it's a red flag that demands deep investigation.

A business that can’t consistently generate cash is a speculation.

A business that can is a potential compounder.

But a growing river of cash is only part of the story.

How much cash is it generating for every dollar in sales?

This leads to the second filter.

Free Cash Flow Margins

Measure the business's cash-printing efficiency.

This is done with the Free Cash Flow Margin.

It tells you how much real cash is left over from total revenue.

It is one of the purest measures of profitability and operational excellence.

High margins mean the business has pricing power and low capital needs.

The formula is simple: Free Cash Flow / Total Revenue.

Look for margins consistently above 15%. The truly elite businesses live above 20%.

Compare it to its closest competitors. A leader will have sustainably superior margins.

A business that gushes cash is a wonderful thing.

But what it does with that cash is what ultimately creates wealth.

This brings us to the third, and most important, filter.

Management’s Use of Capital

Judge the managers, not just the business.

This is a key insight from Michael Mauboussin.

How management uses the cash it generates is the ultimate test.

Great operators can be terrible capital allocators.

This crucial difference separates good companies from great investments.

Do they reinvest that cash into high-return projects within the business?

Do they buy back shares, but only when the stock is trading below its intrinsic value?

Do they make smart, strategic acquisitions that add value, or do they overpay for growth?

Poor capital allocation is a leaky bucket.

It drains shareholder value, no matter how much cash the business produces.

This three-step filter finds great businesses.

Now, we just need to find a great price.

Use Free Cash Flow to find your margin of safety.

Joel Greenblatt's "Magic Formula" is built on a similar idea.

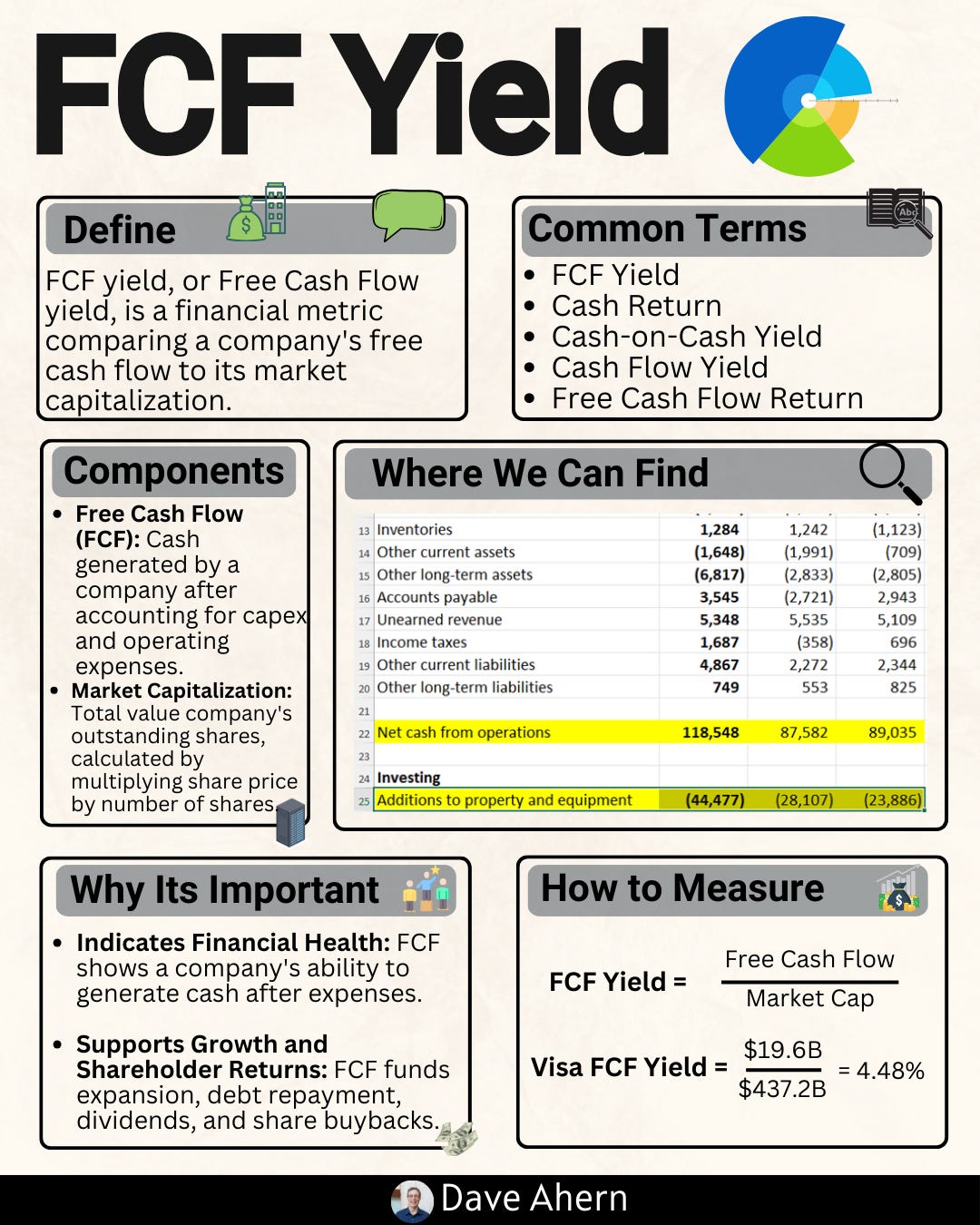

The FCF Yield anchors your decision in business reality, not market hype.

It tells you your potential return on investment if you bought the entire company today.

The formula is: FCF per share / Current Stock Price.

Think of this as your "owner's yield."

Compare this yield to the 10-year treasury bond. A yield significantly higher than the "risk-free" rate suggests you have a margin of safety.

This simple check helps you avoid the biggest mistake: overpaying.

It grounds your investment thesis in cold, hard cash.

Analyzing a business through its cash flow is like having x-ray vision.

You see the bones of the operation.

You see its strength, its efficiency, and how its leaders think.

This is how you find companies built to last.

This framework isn't a secret.

It's a synthesis of the core principles taught by Buffett, Damodaran, Greenblatt, and Mauboussin.

They all reached the same conclusion.

Follow the cash.

What's the biggest challenge you face when analyzing a company's cash flow statement?