Why Companies Pay (or Don’t Pay) Dividends: The Lifecycle of Capital Allocation

“The best thing a company can do with a profit is reinvest it at a high rate of return. The second-best thing is to return it to shareholders. The worst thing is to reinvest it at a low rate of return.”

— Paraphrasing Warren Buffett’s capital allocation philosophy

Amazon didn’t pay a dividend for 27 years. Johnson & Johnson has increased its dividend for 62 consecutive years. And Meta, a company sitting on billions in cash, didn’t pay its first dividend until February 2024.

Three massive companies. Three completely different approaches to returning cash to shareholders. The question isn’t which approach is “right.” The question is why each company made the choice it did, and what that choice tells us about where the business sits in its lifecycle.

Understanding why companies pay (or don’t pay) dividends is one of the most practical skills a dividend investor can build. It helps you identify which companies are likely to start paying dividends, which ones will keep growing them, and which ones might be paying out more than they can afford.

In today’s post, we will learn:

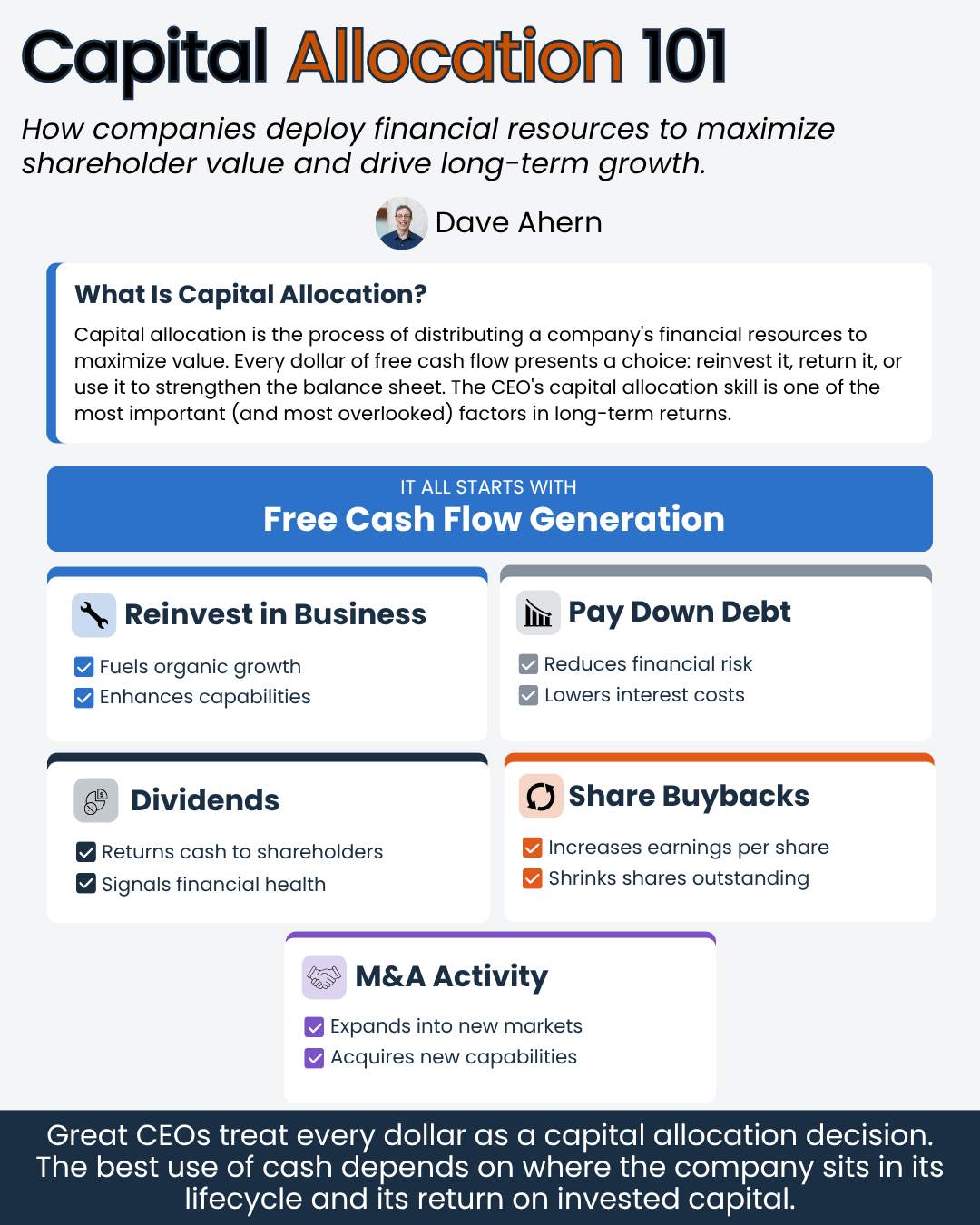

Capital Allocation: The Decision Behind Every Dividend

The ROIC Framework: When Reinvesting Beats Paying Out

The Corporate Lifecycle: From Growth Machine to Dividend Payer

Real-World Examples: Amazon, Meta, and Johnson & Johnson

What This Means for Your Investing Process

Okay, let’s dive in and learn more about why companies pay dividends.

Capital Allocation: The Decision Behind Every Dividend

Every quarter, a company’s management team faces a fundamental question: What do we do with the cash this business generates?

That question is the heart of capital allocation, and every dividend payment is a capital allocation decision. The CEO and board are choosing to send cash to shareholders rather than deploy it elsewhere.

A company has five primary options for its free cash flow:

Reinvest in the business. Build new products, enter new markets, expand capacity. This is organic growth.

Make acquisitions. Buy other companies or assets to grow revenue and capabilities.

Pay down debt. Reduce leverage and improve the balance sheet.

Pay dividends. Send cash directly to shareholders as a regular distribution.

Buy back shares. Repurchase outstanding stock, reducing the share count and increasing each remaining share’s claim on future earnings.

The order matters. Buffett has made it clear throughout his shareholder letters that the best use of a dollar is to reinvest it in the business at a high rate of return. The second-best use is returning it to shareholders. The worst use? Reinvesting it at a low rate of return, which destroys value.

This is why a company that doesn’t pay a dividend isn’t automatically a bad investment. If it can reinvest every dollar at 25% returns, you want it to keep doing exactly that. The compounding works in your favor.

Conversely, a company paying a fat dividend might be telling you something important: it has run out of high-return reinvestment opportunities. That’s not necessarily bad. It just means the company has matured, and its value proposition to shareholders has shifted from growth to income.

The key insight is this: a dividend is not a reward for owning a stock. It signals how the company’s management views its own reinvestment opportunities.

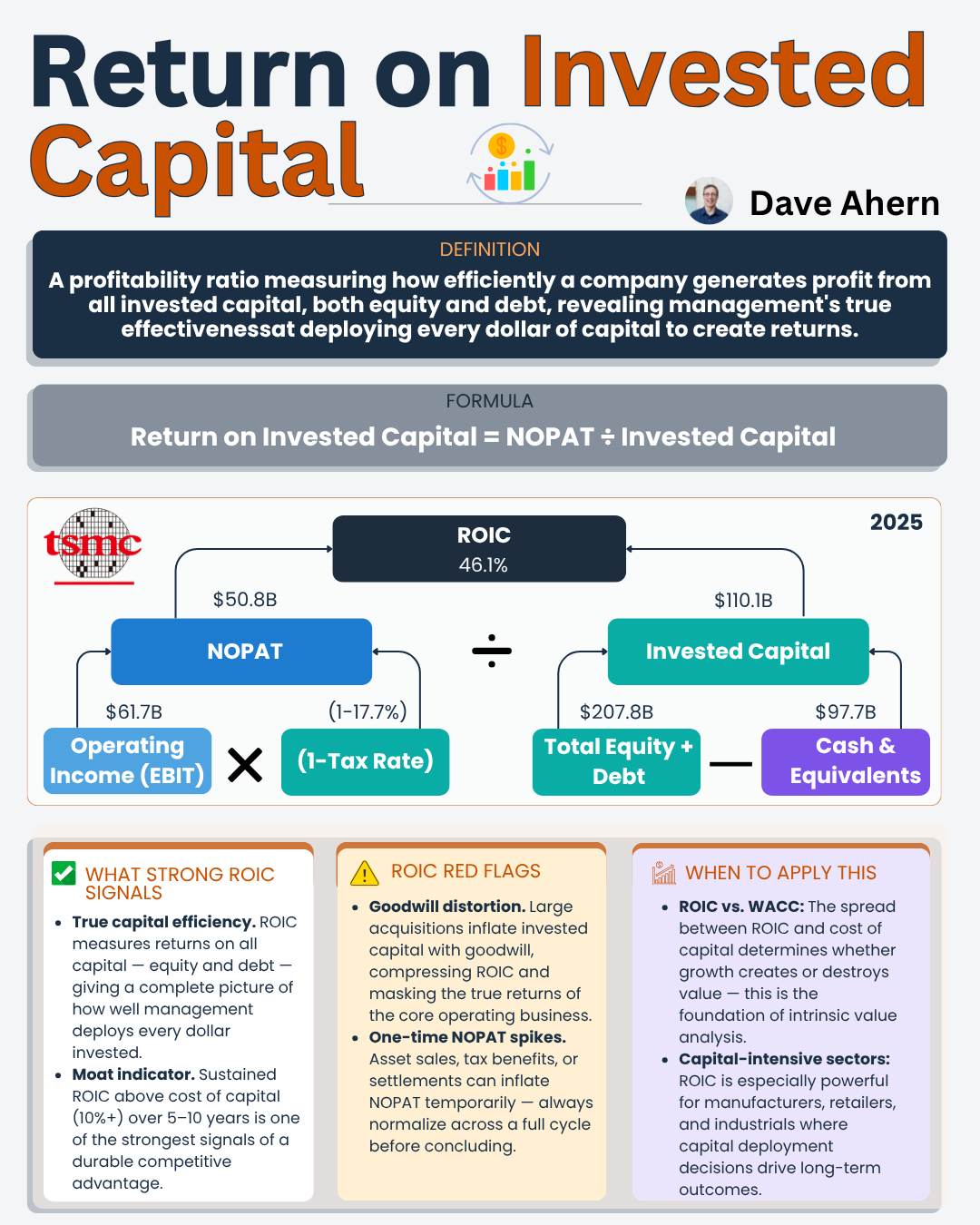

The ROIC Framework: When Reinvesting Beats Paying Out

Let’s put some numbers behind the capital allocation decision. The metric that drives the whole equation is Return on Invested Capital (ROIC).

ROIC measures how efficiently a company converts capital into profit. The formula is straightforward:

ROIC = Net Operating Profit After Tax (NOPAT) / Invested Capital

The decision to pay or not pay a dividend comes down to comparing two numbers: the company’s ROIC and its cost of capital (WACC).

Here’s the simple version. If a company earns 20% on every dollar it reinvests and its cost of capital is 10%, every reinvested dollar creates value. The company should keep reinvesting and skip the dividend.

Now flip it. If a company earns 6% on reinvested capital and its cost of capital is 10%, every reinvested dollar destroys value. The company should return that cash to shareholders, who can invest it elsewhere for higher returns.

Let me make this concrete with a simple example.

Imagine two companies, both earning $100 million in free cash flow. Company A generates a 25% ROIC and reinvests all $100 million. After one year, that reinvestment produces $25 million in additional operating profit. Company B generates a 7% ROIC and also reinvests all $100 million. Its reinvestment produces just $7 million in additional operating profit.

If both companies have a 10% cost of capital, Company A created $15 million in value (25% return minus 10% cost, applied to the $100 million). Company B destroyed $3 million in value (7% return minus 10% cost). Company B’s shareholders would have been better off receiving that $100 million as a dividend and investing it elsewhere.

This is why Buffett described three categories of businesses in his 2007 shareholder letter. The great business earns high returns on capital and needs little additional investment. Good businesses earn adequate returns but require significant capital to grow. The gruesome business requires huge capital and earns low returns. Companies in that first category often start paying dividends because they simply generate more cash than they can profitably reinvest.

The ROIC vs. WACC relationship is the financial engine behind every dividend decision, even if management never uses those exact words.

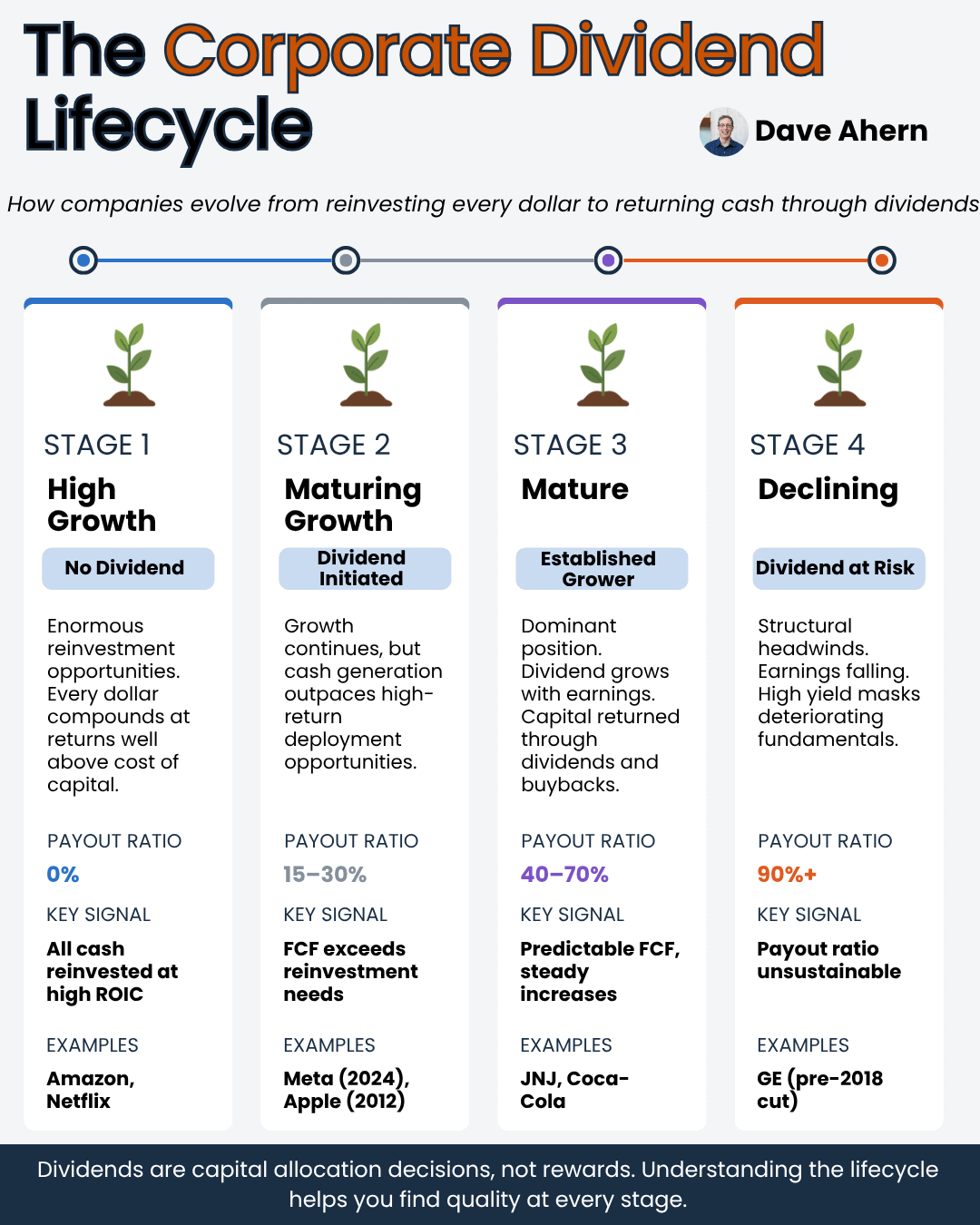

The Corporate Lifecycle: From Growth Machine to Dividend Payer

Companies, like people, go through stages. And the stage a company occupies largely determines whether it pays a dividend, how much it pays, and how quickly that payment grows.

Think of the corporate lifecycle in four stages.

Stage 1: High Growth (No Dividend)

The company has enormous reinvestment opportunities. Every available dollar can be deployed at returns well above the cost of capital. The addressable market is large, and the business is scaling rapidly.

At this stage, paying a dividend would be a mistake. Why send cash to shareholders when the business can compound it at 20%, 30%, or higher? Amazon operated in this stage for nearly three decades. It had so many high-return opportunities (fulfillment centers, AWS infrastructure, Prime ecosystem) that returning cash to shareholders would have slowed the compounding machine.

Capital allocation priority: Reinvest everything. No dividend, minimal or no buybacks. Cash funds growth.

Stage 2: Maturing Growth (Dividend Initiation)

Growth remains strong, but the company starts generating more free cash flow than it can reinvest at high returns. The core business is established. New growth projects exist, but they can’t absorb all the cash the business produces.

This is the inflection point at which many companies initiate dividends. Management is signaling that the business has matured enough to generate excess cash, and they’re confident that cash flow will remain stable enough to sustain regular payments.

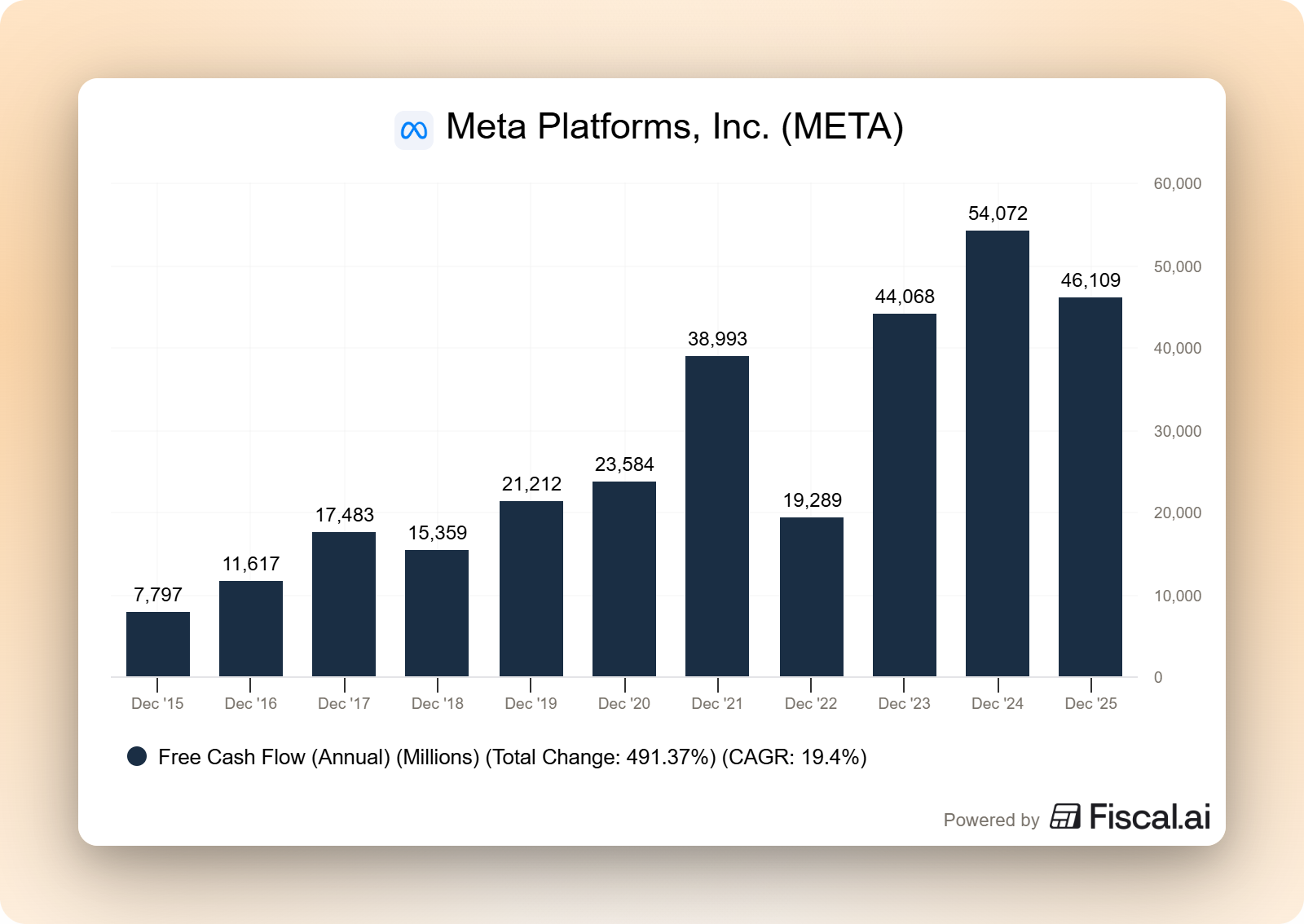

Meta is the textbook example here. For years, the company reinvested aggressively in its platforms, data centers, and the metaverse. But by early 2024, free cash flow had grown so large that even after heavy capital expenditures, the company had billions sitting on the balance sheet with no high-return home. Initiating a dividend was a disciplined capital allocation move.

Apple’s story followed the same arc. The company didn’t pay a dividend for 17 years after Steve Jobs returned. It initiated its dividend in 2012, not because the business was declining, but because cash generation had outpaced reinvestment needs.

Capital allocation priority: Reinvest in growth, but begin returning excess cash. Dividend payout ratios are typically low (15% to 30% of earnings), leaving room for continued investment and dividend growth.

Stage 3: Mature (Established Dividend Grower)

The business has a dominant market position. Growth is steady but slower. Free cash flow is predictable. The company has settled into a rhythm of returning significant cash to shareholders through dividends and buybacks while making targeted reinvestments to maintain its competitive position.

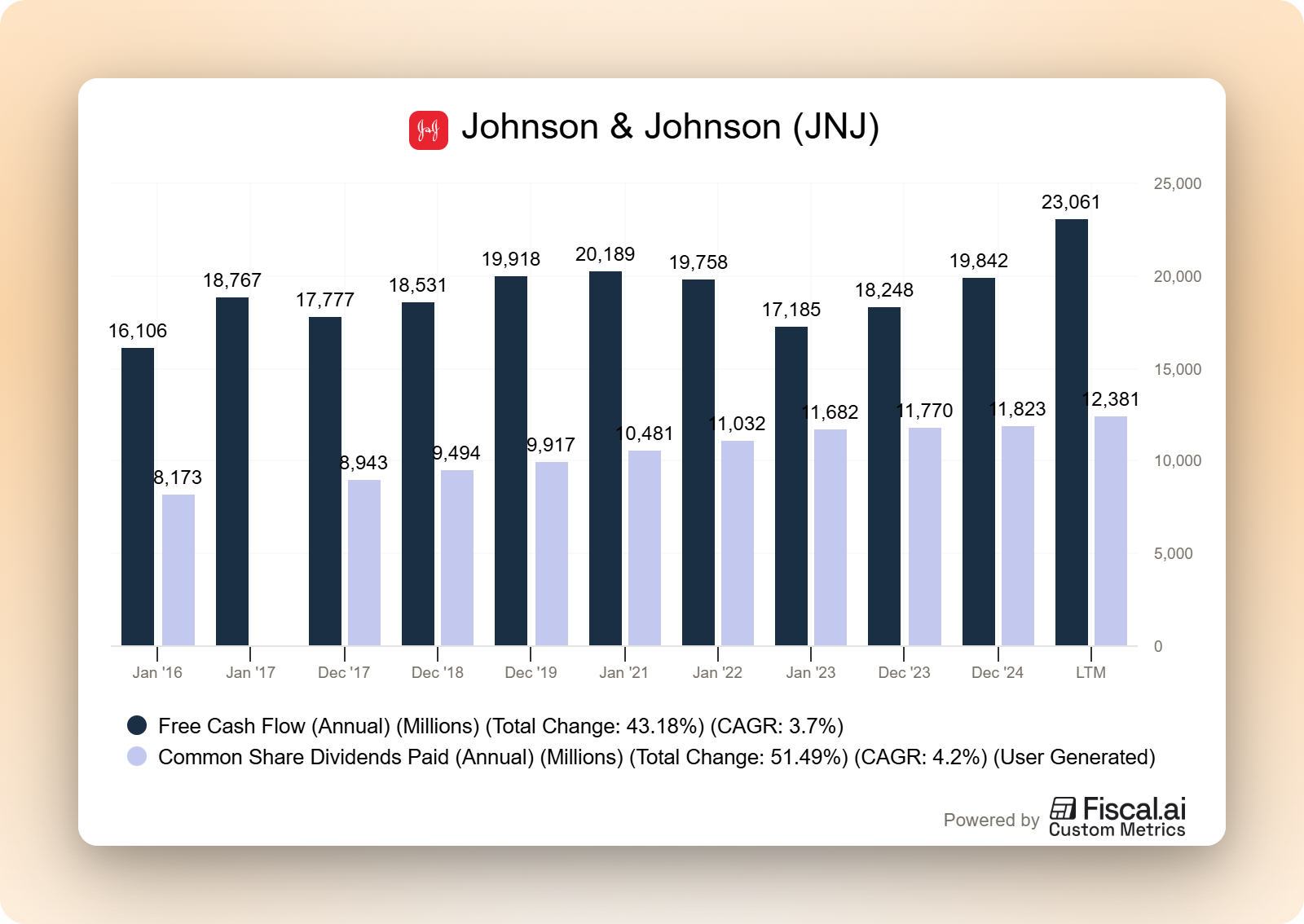

Johnson & Johnson lives here. The company has increased its dividend for 62 consecutive years. Its business generates consistent free cash flow across its pharmaceutical, MedTech, and consumer health segments (the last of which was spun off as Kenvue in 2023). Growth still exists through the pharmaceutical pipeline and surgical robotics, but the reinvestment opportunities are not large enough to absorb all the cash the business produces.

Coca-Cola is another classic example. The company has paid a dividend every year since 1920 and has increased it for 62 consecutive years. Coke’s reinvestment needs are modest because its brand, distribution network, and franchise model require relatively little incremental capital to maintain.

Capital allocation priority: Balance between dividends, buybacks, and selective reinvestment. Payout ratios typically range from 40% to 70% of earnings. Dividend growth tracks earnings growth.

Stage 4: Declining or Challenged (Dividend at Risk)

The business faces structural headwinds. Revenue and earnings are stagnant or shrinking. Free cash flow may be declining. The dividend becomes increasingly difficult to sustain, and the payout ratio creeps higher as earnings fall.

This is where dividend traps live. The stock looks attractive because the yield is high, but that high yield reflects the market’s expectation of a cut. GE provides a cautionary tale. The conglomerate was once a Dividend Aristocrat, but years of poor capital allocation decisions, low returns on invested capital, and mounting debt forced a devastating 92% dividend cut in 2018.

Capital allocation priority: Preserving the business. Cash often goes to debt reduction or restructuring. Dividends may be cut or eliminated. Investors chasing yield at this stage often get burned.

Most investors look at a dividend yield and hope it’s sustainable. Hope isn’t a process.

Below, I’ll show you how to read the signals that tell you whether a dividend is safe, growing, or headed for a cut. We’ll use Amazon, Meta, and JNJ as case studies, and I’ll share the exact evaluation questions I use in my own investing process.

Stop guessing. Start knowing.

Real-World Examples: Amazon, Meta, and Johnson & Johnson

Let’s trace the lifecycle through three companies at different stages.

Amazon: The Perpetual Reinvestor

Amazon has never paid a dividend. For most of its public life, that made perfect sense. The company was building fulfillment infrastructure, launching AWS, developing Prime, and entering new markets at a pace that absorbed every dollar of free cash flow.

The lesson here is straightforward. Amazon’s ROIC on AWS and its logistics network has been well above its cost of capital. Every dollar reinvested created more than a dollar of value. Paying a dividend would have been a poor use of capital.

The interesting question for Amazon going forward is: as AWS matures and free cash flow continues to grow, will the company eventually reach the inflection point at which it initiates a dividend? It is not a matter of if. It is a matter of when. Once reinvestment opportunities can no longer absorb all the cash, the logic of capital allocation will push the company toward returning cash to shareholders.

Meta: The Recent Convert

Meta’s dividend initiation in February 2024 is one of the clearest examples of a company crossing from Stage 1 to Stage 2 in real time.

The signal was clear. Meta’s core advertising business (Facebook, Instagram, WhatsApp) had become a cash-generating machine. Even with heavy spending on AI infrastructure and Reality Labs, the company was generating far more cash than it could deploy at high rates of return. The cash pile on the balance sheet had grown to the point where failing to return it would have been an irresponsible capital allocation decision.

Notice what Meta’s dividend initiation did not mean. It did not mean growth was over. It did not mean the stock was suddenly a “value trap.” It meant the company had matured to the point where its free cash flow exceeded its reinvestment needs. That’s a sign of strength, not weakness.

For investors tracking companies that might initiate a dividend, Meta is the template. Look for businesses with massive free cash flow, growing cash balances, and reinvestment spending that is leveling off relative to revenue. When the gap between cash generation and cash deployment gets wide enough, a dividend often follows.

Johnson & Johnson: The Steady Compounder

Johnson & Johnson represents the mature dividend grower in its purest form.

JNJ’s capital allocation tells the story of a mature company that has found its equilibrium. The company reinvests a portion of free cash flow into its pharmaceutical pipeline and MedTech segments. It makes targeted acquisitions. And it returns the rest to shareholders through dividends and buybacks.

The company’s ROIC has consistently exceeded its cost of capital, but the magnitude of that spread has narrowed over the decades as the business has matured. That narrowing is natural. It’s the financial signature of a company moving from high growth into steady maturity.

For dividend investors, JNJ represents the ideal end state: a company with a durable competitive advantage, predictable cash flows, and a management team that has demonstrated disciplined capital allocation over decades.

What This Means for Your Investing Process

Understanding the dividend lifecycle changes how you evaluate companies. Here are the questions I ask before investing in any company, whether it pays a dividend or not.

1. Where is this company in its lifecycle?

A high-growth company with no dividend requires a different evaluation than a mature dividend grower. Match your expectations to the stage.

2. Is the ROIC consistently above the cost of capital?

If yes, the company creates value whether it pays a dividend or not. If ROIC is declining toward the cost of capital, watch for a shift in capital allocation.

3. Is free cash flow growing faster than dividends?

A growing cushion between free cash flow and dividend payments means the dividend is safe and has room to grow. A shrinking cushion is a warning sign.

4. Why is (or isn’t) this company paying a dividend?

Companies that don’t pay dividends because they have better uses for the cash are very different from companies that don’t pay because they can’t afford to.

5. If the company just initiated a dividend, what triggered it?

Was it a sign of maturing cash flows (positive) or a management gimmick to prop up the stock price (concerning)? Look at the free cash flow trajectory to find the answer.

The most important takeaway is this: dividends are not the goal. Value creation is the goal. Dividends are one way that value flows to shareholders, and the best companies allocate capital to maximize total value, whether that means reinvesting, acquiring, buying back shares, or paying dividends.

As dividend investors, our job is to find companies that create value and distribute a growing share of it through dividends. The lifecycle framework helps us understand when that transition happens and which companies are most likely to sustain it.

Common Mistakes to Avoid

Assuming no dividend means a bad investment.

Amazon, Berkshire Hathaway, and Netflix have created enormous shareholder value without paying dividends. No dividend simply means management believes reinvestment creates more value.

Chasing yield without understanding the lifecycle stage.

A 9% yield on a company in Stage 4 (declining) is far more dangerous than a 1.5% yield on a company in Stage 2 (initiating and growing). The yield tells you the price. The lifecycle stage indicates sustainability.

Ignoring the ROIC trend.

A company with a declining ROIC that continues to reinvest heavily is making a capital allocation mistake. That’s your signal to be cautious, regardless of what the current dividend looks like.

Confusing a dividend cut with a death sentence.

Some companies cut dividends to reallocate capital toward higher-return opportunities. The cut may be painful, but if it leads to better ROIC over time, it could be the right decision. Context matters.

Investor Takeaway

Companies don’t pay dividends because they’re generous. They pay dividends because it’s the best use of their excess cash at that point in their lifecycle. Understanding this changes how you think about your portfolio.

When you see a company like Amazon choosing not to pay a dividend, ask whether its ROIC justifies the reinvestment. When you see Meta initiating a dividend, ask what shifted in its cash flow dynamics. When you see JNJ raising its dividend for the 62nd consecutive year, ask whether the payout ratio and free cash flow trend support continued growth.

The companies that create the most wealth for dividend investors are the ones that move through the lifecycle with discipline: reinvesting when returns are high, returning cash when they’re not, and communicating clearly about why.

That is going to wrap up our discussion for today.

As always, thank you for taking the time to read this post, and I hope you find something of value on your investing journey.

If I can further assist, please don’t hesitate to reach out.

Until next time, take care and be safe out there,

Dave

Most investors look at a dividend yield and hope it’s sustainable. Hope isn’t a process.

Below, I’ll show you how to read the signals that tell you whether a dividend is safe, growing, or headed for a cut. We’ll use Amazon, Meta, and JNJ as case studies, and I’ll share the exact evaluation questions I use in my own investing process.

Stop guessing. Start knowing.

Very Interesting!

Dividends are an output, not a goal. What matters is ROIC vs reinvestment opportunities. Misreading lifecycle leads to overpaying for “yield traps.”