What Berkshire's 13F Reveals about Dividend Stocks

Buffett and dividends, he buys them but has never paid one

On May 15, 2026, Berkshire Hathaway filed its first 13F under a new CEO. Greg Abel officially took over from Warren Buffett on January 1, and this filing was the first real look at how he is thinking about the portfolio Warren spent six decades building.

For dividend investors, the answer matters.

Berkshire is not run as a dividend portfolio. But the cash that flows in from these positions has helped fund every Berkshire move for decades. According to the filing, Berkshire collected over $3 billion in dividends last year from just five stocks. That income stream is the engine behind the buybacks, the acquisitions, and the cash pile.

So when Abel made changes in his first quarter, it told us something. Not about which stocks to buy tomorrow, but about how a disciplined capital allocator thinks about quality, price, and patience.

In today’s post, we will discuss:

What a 13F is and why dividend investors should read it

What changed in Berkshire’s Q1 2026 filing

The dividend stocks Berkshire kept

The dividend stocks Berkshire trimmed or exited

What this tells us about building a dividend portfolio

Common mistakes when copying Berkshire

Okay, let’s dive in and learn what we can pull from this filing.

Before we dig in: if you want filings like this one broken down every month, with the math shown, that is exactly what I send. Free to start.

What is a 13F and why does it matter?

A 13F is a quarterly filing the SEC requires from any institutional investment manager with over $100 million in assets under management. It lists their long equity positions as of the end of the quarter.

Berkshire files its about 45 days after quarter end. The Q1 2026 filing covered positions as of March 31, 2026.

Two things matter for dividend investors here.

First, the 13F is backward-looking. Positions may have changed since the snapshot date. So we read it for clues about thinking, not as a buy list.

Second, what stays in the portfolio quarter after quarter often tells us more than what changes. Buffett used to say his favorite holding period was forever. The stocks that survive every quarter for decades are usually the ones with the strongest moats.

That is the lens we want for this filing.

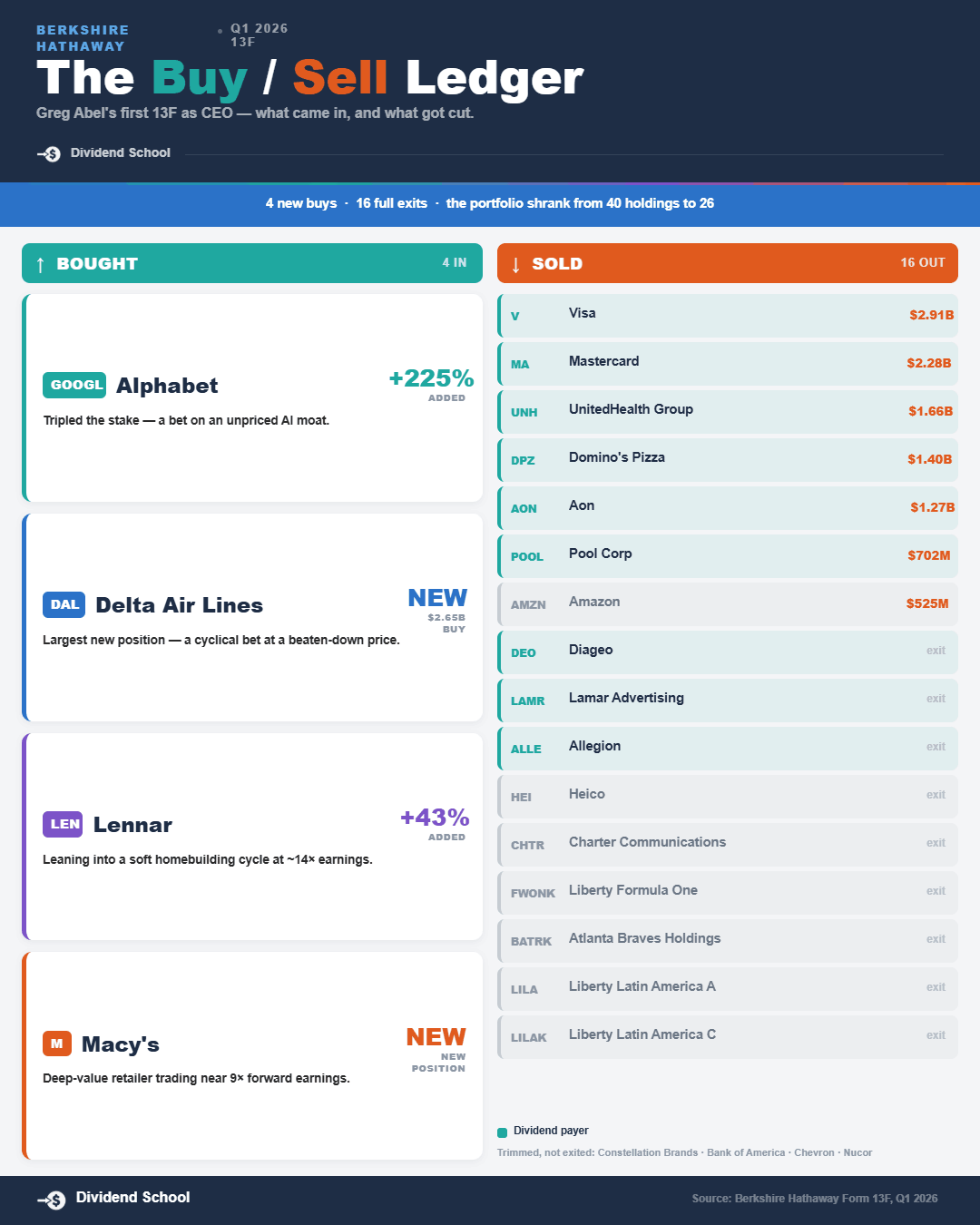

What changed in Q1 2026

The headline numbers from the Q1 2026 13F are clear. Per the Seeking Alpha portfolio tracker:

Total 13F portfolio value: $263.1 billion (down from $274.2 billion in Q4 2025)

Number of positions: 26 (down from 40)

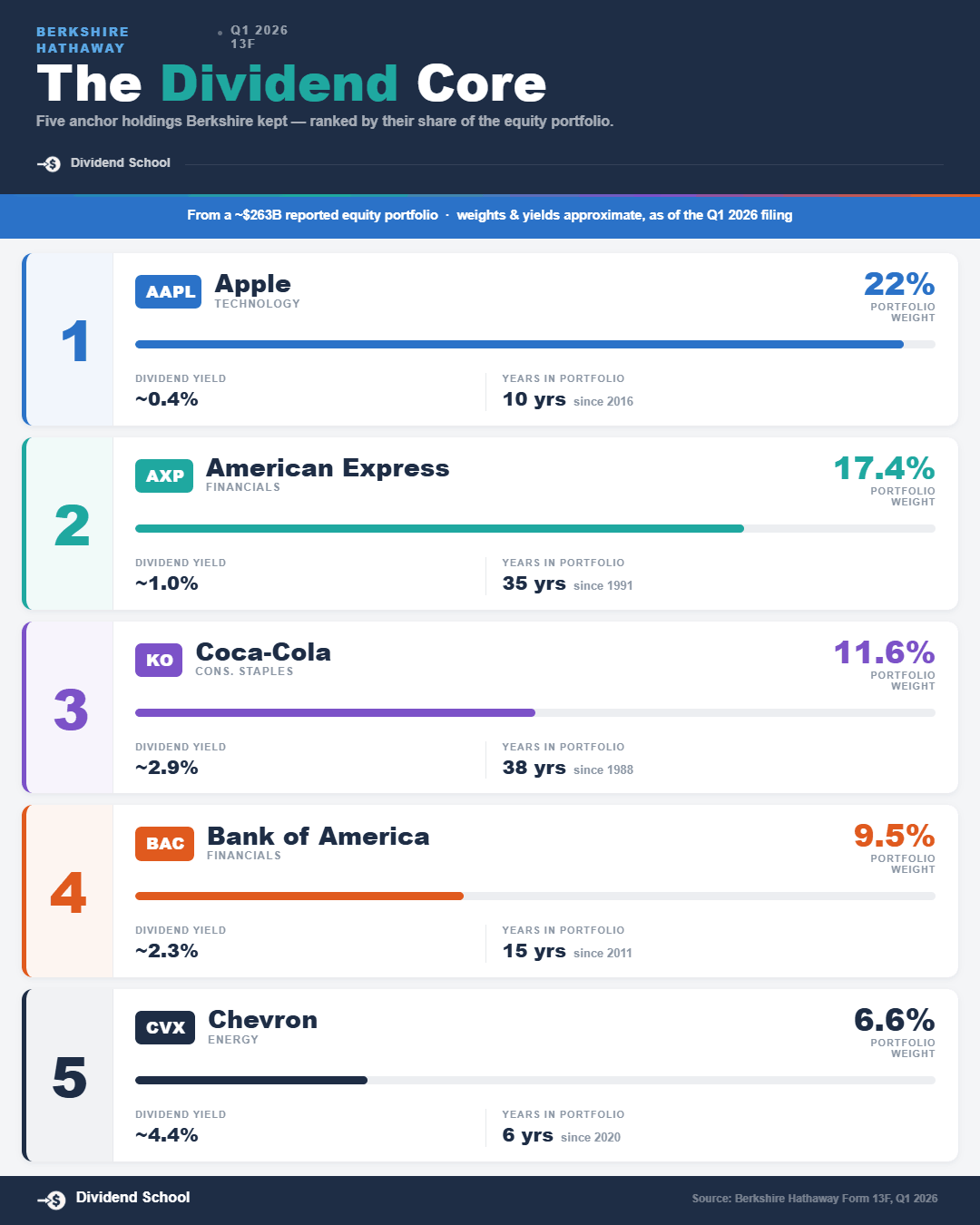

Top five holdings: Apple, American Express, Coca-Cola, Bank of America, Chevron

Top five concentration: roughly 68% of the portfolio

Apple alone: about 22% of the portfolio

The big takeaway is concentration. Abel did not blow up the portfolio. He tightened it.

He sold 16 positions entirely and added a handful of new ones. The full list included Amazon, UnitedHealth, Domino’s Pizza, and smaller dividend names such as Constellation Brands, Lamar Advertising, and Diageo. He also continued the wind-down of the Visa and Mastercard positions that Buffett had been trimming.

Abel did not just sell, though. He made one notable buy.

Berkshire increased the Alphabet (GOOGL) position by 225%. This is unusual territory for Berkshire. Buffett famously avoided Google for years and called it one of his bigger mistakes. Abel apparently sees it differently.

He also opened new positions in Delta Air Lines, Lennar, and Macy’s, all classic value plays at discounted prices.

So what does this mean for dividend investors? Look at what stayed.

If reading a 13F this way sharpens your thinking, that is the whole point of Dividend School. Every month I take one company, pull the numbers straight from the filings, and show you the math the way I just did here. I own the stocks I write about. No black box.

Try it free. Cancel anytime.

The dividend stocks Berkshire kept

The core of the dividend portfolio is intact. Five names do almost all the work.

Apple (AAPL) is roughly 22% of the portfolio. It pays a modest dividend, but the scale of Berkshire’s position means the dollar dividend is enormous. Buffett called Apple “Berkshire’s third business” for a reason.

American Express (AXP) has been in the portfolio since the 1990s. It has the lowest yield of the group at around 1.1%, but the dividend growth rate is the strongest. Amex earns money from card fees, swipe fees, and net interest on revolving balances.

Coca-Cola (KO) is Berkshire’s longest-held position. According to 24/7 Wall St., the company has raised its dividend for 63 consecutive years. It currently makes up nearly 10% of the portfolio. Buffett bought it in 1988 and has not sold a share.

Bank of America (BAC) is the bet on net interest income at scale. It is Berkshire’s fourth-largest holding. The yield is moderate, but the payout ratio sits in the low 30% range, leaving plenty of room for growth.

Chevron (CVX) is the energy anchor. Per the 24/7 Wall St. report based on the 13F, Berkshire still owns 122 million shares, representing roughly 7% of the portfolio. CVX yields about 4.6% with a 38-year dividend growth streak.

These five names share something in common.

They are all dominant in their categories, generate massive free cash flow, and return that cash to shareholders through dividends and buybacks. Every one of them sits on a moat that has been compounded for decades.

The dividend stocks Berkshire dropped

The exits are where the story gets interesting for income investors.

Abel cleaned out a long list of smaller dividend names. Some of these were high-yield positions that Buffett had added in recent years, including:

Constellation Brands (STZ): premium beer and spirits, yield around 2.7%

Lamar Advertising (LAMR): billboards and outdoor advertising, yield around 4.3%

Diageo (DEO): global spirits brands, yield around 5.0%

Domino’s Pizza (DPZ): pizza franchise, modest yield with strong growth

UnitedHealth (UNH): managed care, modest yield with high growth

He also continued reducing the Chevron position from earlier highs and kept trimming Visa and Mastercard, two long-standing payment network holdings.

The pattern is hard to miss.

Abel kept the five biggest, most durable dividend payers. He cut the smaller positions, the recent additions, and the names where the price had probably moved past a comfortable value.

These were not bad businesses. Most of them are excellent companies. But a 13F manager has to deploy capital where the math still works. When a position outgrows its margin of safety, selling becomes part of the discipline.

What this tells us about dividend investing

This is where it gets useful for our own portfolios.

A few lessons jump out of this filing. They are not new ideas, but seeing them play out at the Berkshire scale makes them concrete.

Lesson 1: Concentration is the point.

Most retail investors hold 30, 50, sometimes 100 stocks. Abel runs Berkshire’s stock portfolio with 26 names, and five of them do 68% of the work.

That does not mean you should hold five stocks. But it does mean diluting your best ideas across dozens of mediocre ones probably costs you more than it protects you.

Pick your best dividend ideas, size them appropriately, and let them work.

Lesson 2: Yield is not the goal.

Look at the survivors. American Express yields 1.1%. Apple yields under 1%. Bank of America yields around 2%. Coca-Cola and Chevron sit higher, but none of them are at the top of any high-yield screen.

What every survivor has is durable earnings power. The dividend grows because the business grows. That is the engine.

The names Abel cut include several with much higher current yields. Diageo at 5%, Lamar at 4.3%. He cut them anyway. Yield is a result, not a destination.

Lesson 3: Holding is the hard part.

Coca-Cola has been in Berkshire’s portfolio since 1988. American Express since the mid-1990s. Moody’s for over 20 years.

These returns came from doing nothing for decades. No trading. No timing. Just owning the business and collecting the dividends.

For dividend investors, this is the entire game. We pick well, size right, and then we get out of our own way.

Lesson 4: Selling has a place too.

Abel sold 16 names this quarter. Buffett would have called it cleaning up the desk. The “too hard” pile is real.

When a position no longer fits your thesis or the price runs past your sense of value, selling is part of the process. Holding everything forever is romance. Holding the right things for a long time is investing.

How to use this filing in your own process

When the next 13F drops, here is what I look for:

Top five concentrations. If the biggest names are still there at meaningful weights, the long-term thesis is intact.

Net buys and sells in dividend names. Pay attention to direction, not just headlines. A 5% trim is different from a full exit.

New positions. New names show what the manager finds attractive at current prices.

Aggregate dividend income. Add up the annualized dividends from the top holdings. That number indicates how much cash flow the portfolio is generating.

Use the 13F as a teaching tool, not a shopping list. The filing is 45 days old by the time you see it. Prices have moved. The manager may have already adjusted again.

Common mistakes when reading a 13F

A few traps to avoid.

Mistake 1: Treating it as a buy list.

The temptation is strong. Berkshire bought Alphabet, so let me go buy Alphabet too. The problem is that the filing is a snapshot from 45 days ago. The position size that worked at $X may not work at $X plus 15%.

Read the filing for ideas. Do your own work on price and position sizing.

Mistake 2: Confusing trims for thesis changes.

Berkshire reduced Chevron meaningfully in Q1, but the position is still 7% of the portfolio. That is not a sale. That is rebalancing.

Watch for full exits, large directional moves, and brand new positions. Those are signals. A small trim is often just portfolio management.

Mistake 3: Ignoring the rest of Berkshire.

The 13F covers only the publicly traded U.S. equity portfolio. It does not show the wholly owned subsidiaries, the cash pile, the bond portfolio, or the international holdings.

Berkshire’s full picture includes BNSF Railway, Geico, See’s Candies, and many more. The stock portfolio is one piece of a much bigger machine.

Mistake 4: Assuming the new CEO will think exactly like the old one.

Buffett would not have bought Alphabet. Abel did. Buffett sold the airlines in 2020 and called it a mistake. Abel just bought Delta.

Greg Abel is his own investor. The 13Fs going forward will show his fingerprints, not Warren’s. That is worth remembering as we watch the portfolio evolve.

Investor takeaway

The Q1 2026 filing is the first chapter of a new era at Berkshire. The five anchor dividend holdings are still there. The smaller, higher-yielding names are mostly gone. The portfolio is more concentrated than it has been in years.

For dividend investors, the message is the same one Buffett has been teaching for fifty years. Own a small number of excellent businesses. Pay a fair price. Hold them long enough for the dividends to compound. Sell when the thesis breaks or the price gets silly.

That is the playbook. It has worked through ten recessions, three financial crises, a pandemic, and a CEO transition. It will probably keep working.

That is going to wrap up our discussion for today.

As always, thank you for taking the time to read this post, and I hope you find something of value on your investing journey.

If I can further assist, please don’t hesitate to reach out.

Until next time, take care and be safe out there,

Dave

P.S. If this changed how you read a 13F even a little, that is exactly what Dividend School is for. One full deep dive every month, the math shown, plus the full archive.

Try it free, cancel anytime.

P.P.S. Hit reply and tell me one stock you want me to break down next. I read every reply.