Visa Raised Its Dividend 14%. Amphenol Raised 52%. Here's What Each One Is Telling You.

John Lintner figured this out in 1956. Three companies just proved him right in the last 12 months

When Amphenol raised its quarterly dividend 52% in October 2025, the headline was easy to miss. Just another corporate housekeeping item buried in the earnings release. But a 52% increase isn’t housekeeping. It’s a message.

Dividend increases tell you something that nothing else on the income statement can. They tell you what management actually believes about the future.

In today’s post, we will learn:

Why dividend increases carry a signal no press release can fake

Visa: the quiet compounder

Amphenol: the step-change signal

MSCI: the formula-based signal

A practical framework for reading dividend increases

Common mistakes investors make

Investor takeaway

Let’s dive in.

Why Dividend Increases Carry a Signal No Press Release Can Fake

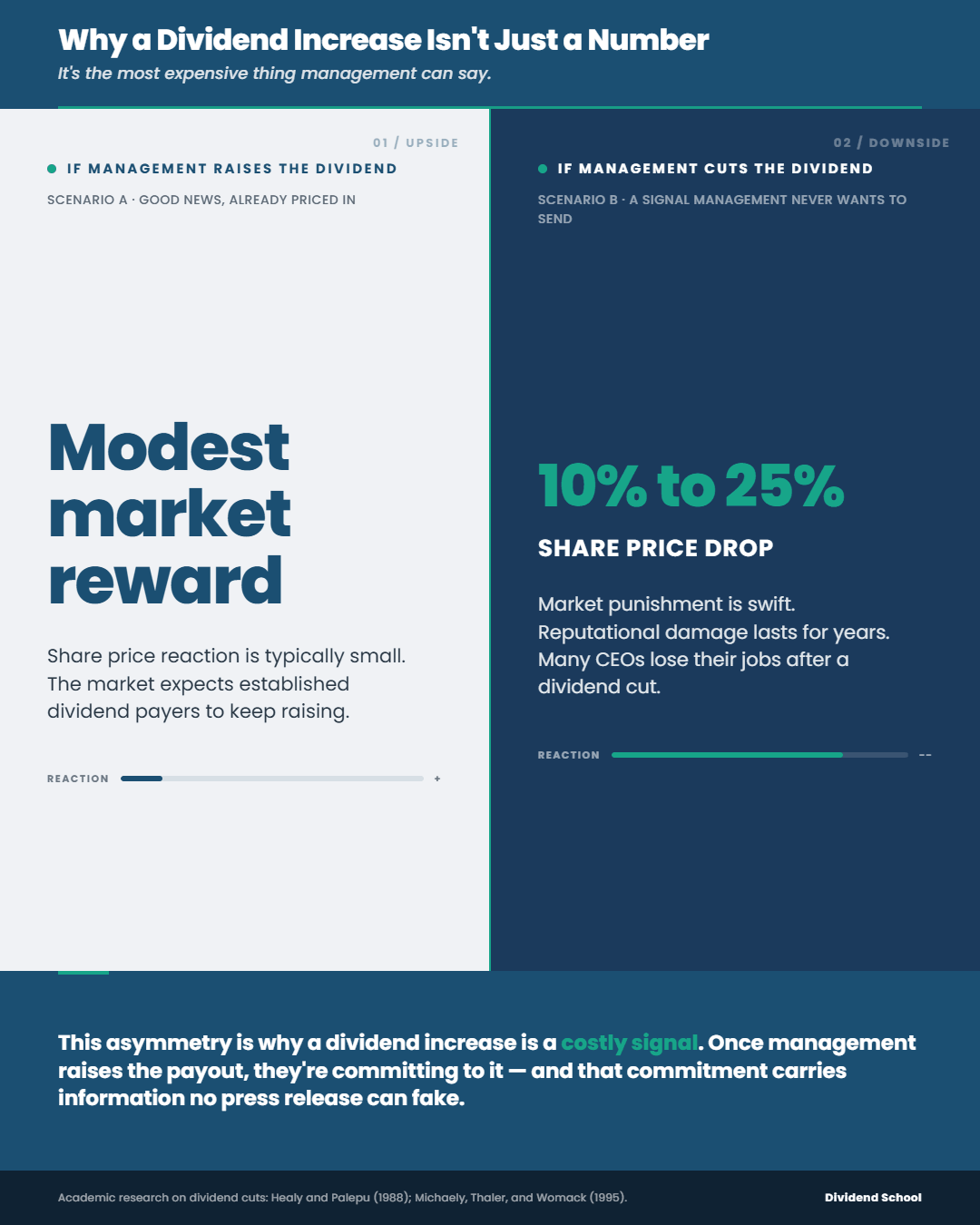

The reason dividend changes carry weight comes down to one word: cost.

Talk is cheap. CEOs can promise growth, raise guidance, or share an exciting product roadmap on an earnings call. Investors hear it, weigh it, and discount it. None of those statements bind management to anything.

A dividend increase is different. Once a company raises its quarterly payout, it has set a new floor. The market punishes a cut faster and harder than almost any other corporate action. Studies of dividend cuts show share prices commonly drop 10% to 25% on the announcement, and the reputational damage lasts years.

Economists call this a costly signal. The cost of being wrong is so high that companies don’t raise the dividend unless management is genuinely confident in sustained free cash flow.

This is why John Lintner’s 1956 research on dividend policy still holds up almost 70 years later. Lintner found that managers smooth dividends and adjust them only when they believe a higher rate is sustainable. They hate cutting dividends more than they enjoy raising them.

That asymmetry is the entire game. A dividend increase reveals what management would never say out loud.

Three current examples make this concrete. Visa, Amphenol, and MSCI each raised their dividend in the last 12 months. Each increase carries a different kind of signal, and each tells you something useful about how management thinks.

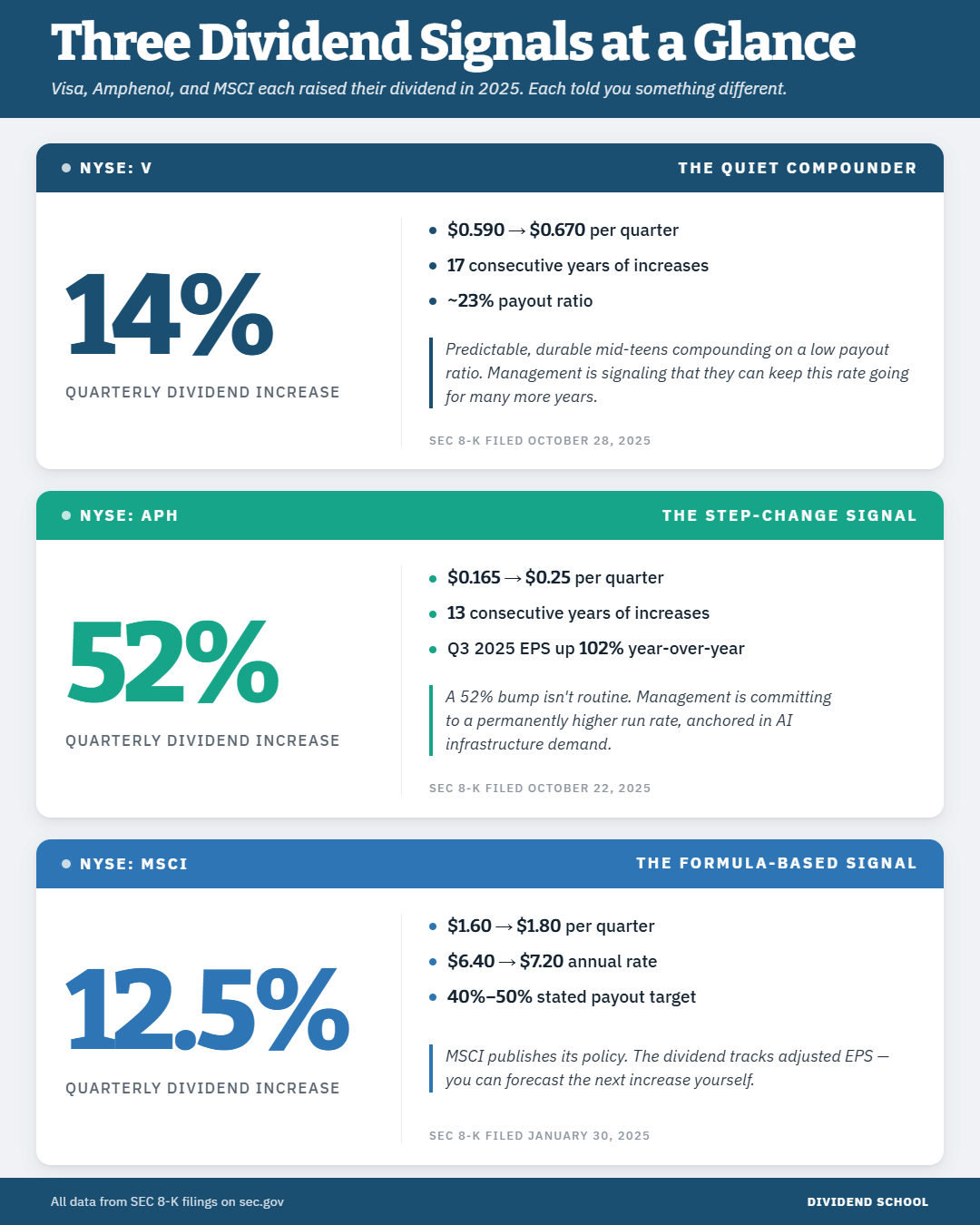

Visa: The Quiet Compounder

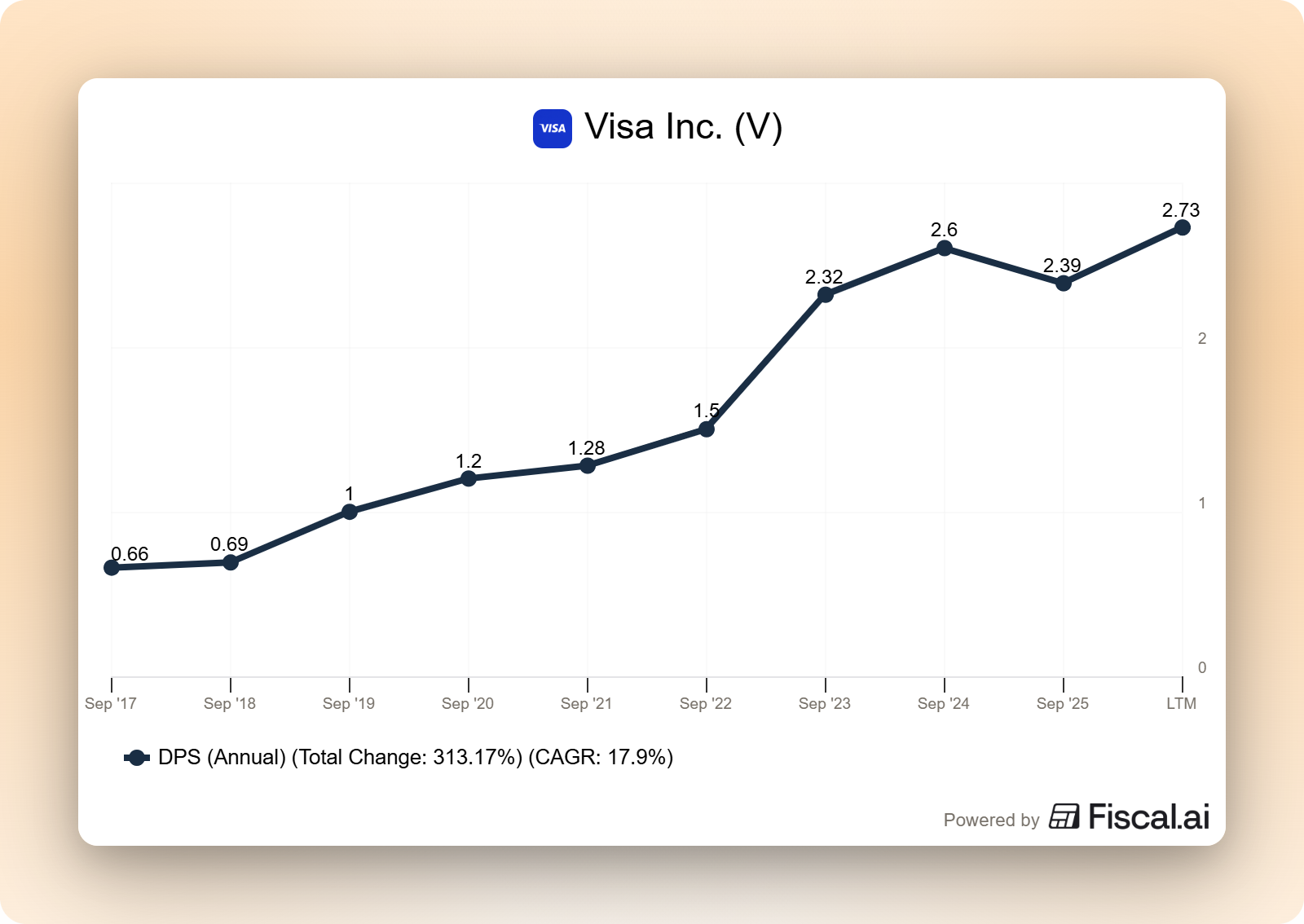

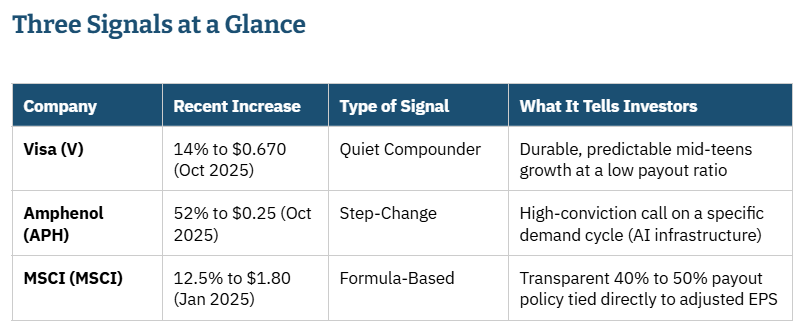

Visa’s signal is consistency.

On October 28, 2025, Visa’s board raised the quarterly dividend 14% to $0.670 per share, up from $0.590. That increase came in a fiscal year in which Visa generated $40.0 billion in net revenue, up 11%, and non-GAAP net income of $22.5 billion, up 14% (Visa fiscal Q4 2025 earnings release, filed as an 8-K with the SEC, October 28, 2025).

What stands out isn’t the 14%. It’s the pattern. Visa has raised its dividend 17 years in a row, with a five-year compound growth rate of roughly 15% to 16%. The 2024 increase was 13%. The 2025 increase was 14%. The math doesn’t shift much.

Now look at the payout ratio. Visa pays out roughly 23% of earnings as dividends. That is unusually low. Most companies growing dividends in the mid-teens are stretching, paying out 70% or 80% of earnings and praying earnings growth keeps up.

Visa is doing the opposite. It is signaling that it can grow the dividend at this clip indefinitely, because the dividend consumes such a small share of the cash it generates. Total capital returned to shareholders during fiscal 2025 was $22.8 billion across dividends and buybacks combined. The dividend itself is the smaller piece.

Here is what Visa’s signal means in practice. Management is telling you: we expect to keep compounding earnings in the low-to-mid teens, and we plan to translate that directly into your dividend check year after year. They are not promising a step change. They are promising a stable, predictable, multi-year machine.

That kind of signal fits the business. Visa’s revenue comes from transaction volume on a network that gets stronger with every additional cardholder and merchant. There are no AI cycles to time, no commodity prices to worry about. Just a slow, compounding toll on global commerce.

The takeaway from Visa: when a high-quality business with a low payout ratio raises its dividend at the same rate year after year, the company is signaling durability, not breakout.

Amphenol: The Step-Change Signal

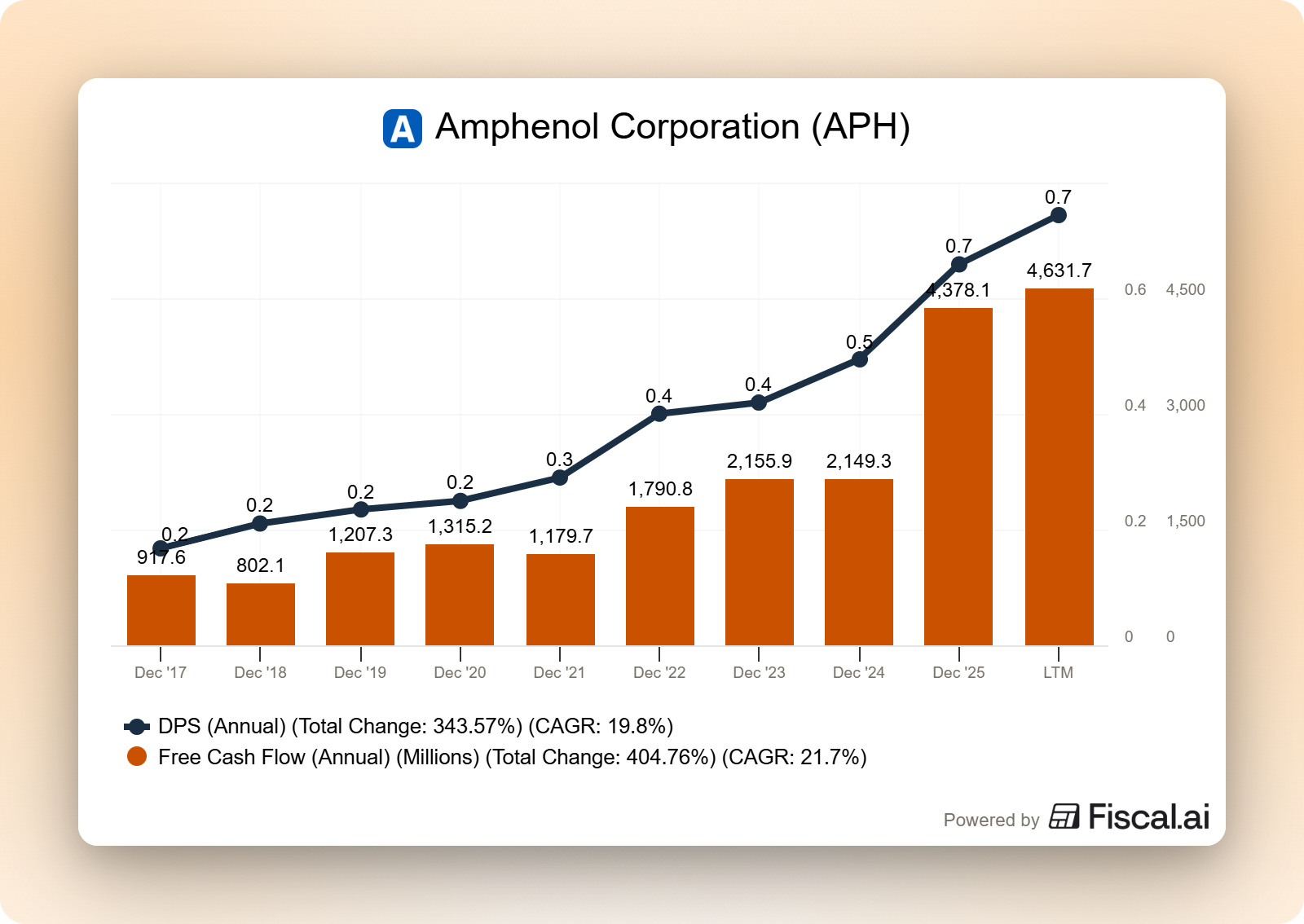

Amphenol’s signal is conviction.

On October 22, 2025, alongside record third-quarter earnings, Amphenol announced a 52% increase in its quarterly dividend, from $0.165 per share to $0.25 per share (Amphenol Q3 2025 earnings release, filed as 8-K with the SEC, October 22, 2025).

A 52% bump is not normal. Most companies move dividends in 5% to 15% increments. Even high-growth dividend payers rarely raise the run rate this much in a single move.

So what triggered it? Q3 2025 sales hit $6.2 billion, up 53% in U.S. dollars and 41% organically. GAAP diluted EPS was $0.97, up 102%. Operating margin reached a record 27.5%. Free cash flow was $1.2 billion in the quarter.

That kind of growth is anchored in something specific. Amphenol manufactures connectors, sensors, and interconnect systems. Its IT datacom segment, which sells the components that build AI data centers, has been the primary driver of organic growth across 2025. The dividend increase is the company’s way of saying: this isn’t a one-quarter sugar high. We believe the AI infrastructure cycle is going to produce sustained free cash flow at a much higher level than what we were generating two years ago.

Compare what Amphenol could have said in a press release (”we are optimistic about AI demand”) with what the dividend says (”we are willing to bake a 52% higher dividend run rate into every future quarter”). The second is far more expensive to walk back.

A step-change increase like this also carries risk for the investor reading it. If management is wrong about the durability of the cycle, the next move is a cut, and a cut from a base that high is painful. The signal is bullish, but it is also a bet.

This is where you read the rest of the financial statements. Amphenol entered 2026 with 13 consecutive years of dividend increases, an active acquisition program, and an order book reflecting accelerating demand from data-center customers. The signal is consistent with the underlying business, which is what you want to see.

The takeaway from Amphenol: a step-change dividend increase is management putting capital behind their words. Match the size of the increase to the durability of the cash flow story. If the two don’t line up, ask why.

Dividend School exists to make you the kind of investor who reads filings the way you just read this article. If that's the direction you want to go, paid subscribers get a new deep-dive like this every week, plus the full archive of past frameworks, the dividend safety spreadsheet, and the tools I use myself. Subscribe to keep going.

MSCI: The Formula-Based Signal

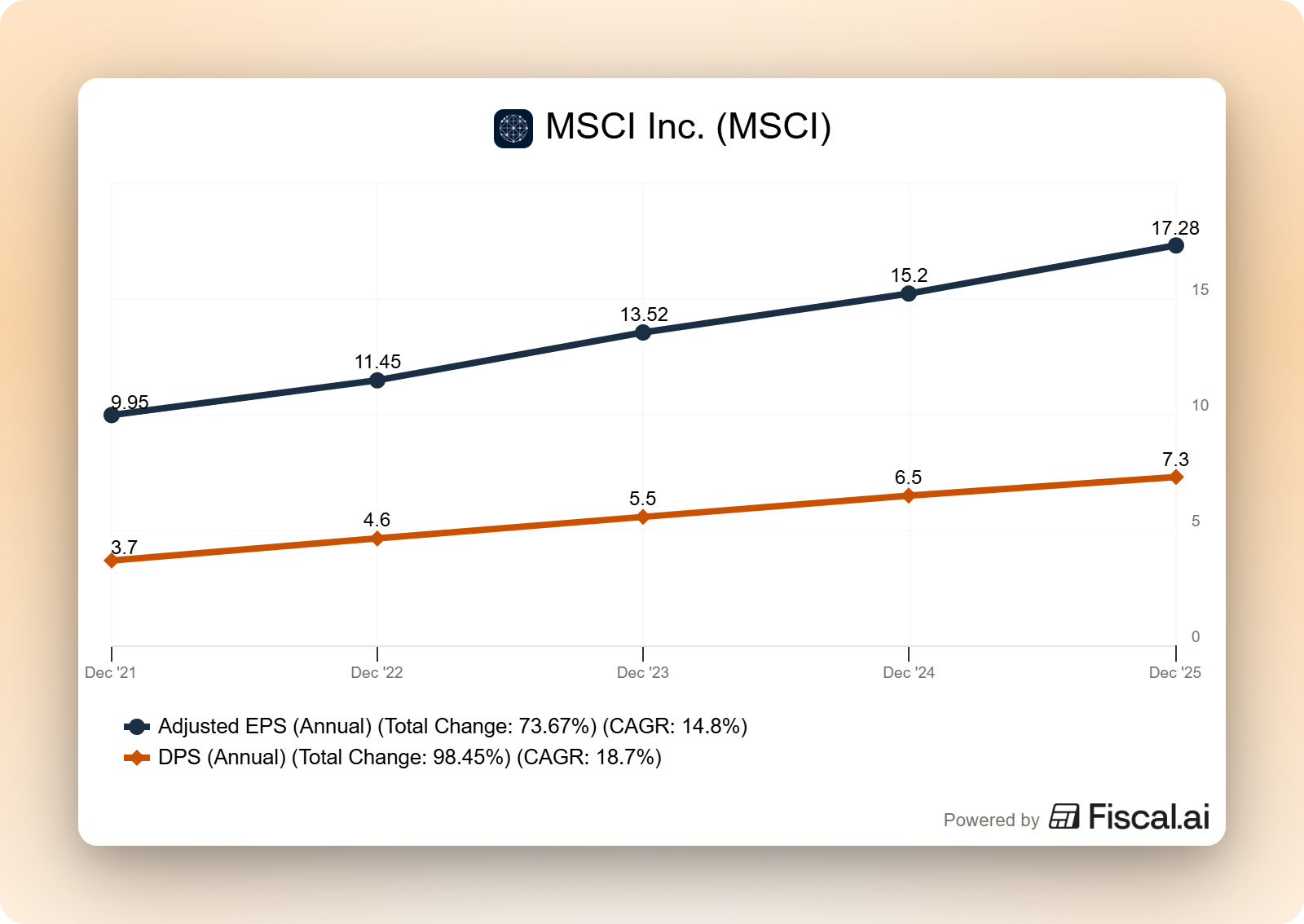

MSCI’s signal is transparency.

On January 30, 2025, MSCI raised its quarterly dividend from $1.60 to $1.80 per share, a 12.5% increase. The annual rate moved from $6.40 to $7.30 (MSCI 8-K filed with the SEC, January 30, 2025).

The interesting part is not the number. It’s the policy. MSCI has publicly stated a target payout ratio of 40% to 50% of adjusted earnings per share. That single sentence does more work than any guidance the company gives on a quarterly call.

This is a different kind of signal from Visa’s quiet compounding or Amphenol’s step change. MSCI is telling investors: We have a rule. When adjusted EPS grows, the dividend grows alongside it. When EPS does not grow, the dividend stays flat.

The advantage of a formula-based dividend is that it removes management discretion from the equation. You don’t need to guess what the board will do at the next meeting. You only need to forecast adjusted EPS and apply the payout percentage.

The disadvantage is that it ties the dividend tightly to earnings. If MSCI has a difficult year, the dividend will reflect that. Investors who want a smooth, recession-proof income stream may prefer a company that maintains its dividend through a downturn.

For MSCI’s business, the formula fits. The company runs an index, analytics, and ESG data business that generates retention rates near 95% on its recurring subscriptions and consistent free cash flow. Q3 2025 free cash flow was $423.3 million, up 7.4% (MSCI Q3 2025 earnings release). Earnings are sticky enough that a formula-based payout is a credible commitment.

There is a deeper layer here. MSCI also announced a new $3.0 billion share repurchase authorization on October 25, 2025. The combination is telling. The dividend follows the formula. The excess capital above the formula goes to buybacks. Investors get a predictable income stream plus discretionary capital returns when cash flow exceeds expectations.

The takeaway from MSCI: a company with an explicit payout ratio policy gives you a forecastable dividend. Track adjusted EPS, and you can model the dividend yourself.

Three Signals at a Glance

Sources: Visa, Amphenol, and MSCI 8-K filings on sec.gov, dated as listed in column 2.

A Practical Framework for Reading Dividend Increases

When a company you own announces a dividend increase, work through these five questions.

1. What is the size of the increase relative to history?

Compare this year’s increase to the trailing three-to-five-year average. An increase in line with history confirms the existing trajectory. An increase well above or below history is sending a different signal, and it deserves an explanation.

2. What is the payout ratio after the increase?

A dividend raised aggressively into a payout ratio above 80% leaves no margin of safety. A dividend raised into a payout ratio of 25% to 50% has room to keep compounding. The lower the payout, the more durable the increase.

3. Did the underlying earnings and free cash flow grow at a similar pace?

The healthiest dividend increases follow earnings growth, not the other way around. If a company raises the dividend faster than free cash flow grew, it is borrowing against future cash. Verify the gap closes.

4. Has management stated a dividend policy?

Companies like MSCI publish a target payout range. Companies like Visa describe a goal of consistent annual increases tied to earnings growth. Read what they said and check whether the actual increase fits the policy.

5. What does the balance sheet say?

A dividend raised while debt is rising and cash is falling is a different signal from one raised while the balance sheet is improving. Always cross-check the dividend announcement against the cash flow statement and the debt schedule.

Run any dividend increase through these five filters and the signal becomes much clearer.

Common Mistakes Investors Make

Three pitfalls show up regularly.

First, focusing only on yield. A 5% yield on a stagnant or declining dividend is worse than a 1% yield on a dividend growing at 14% per year. Visa yields less than 1%, but its dividend has compounded at 15%+ for over a decade. The yield understates what investors actually receive over time.

Second, treating every increase the same. A 3% bump from a mature utility means something very different from a 52% bump from a growth company. The percentage size matters, but so does the company’s history and stated policy.

Third, ignoring the buyback line. Many companies return more capital through buybacks than dividends. Visa returned $22.8 billion in fiscal 2025 across both, with the bulk coming from buybacks. A company that cuts its buyback to fund a dividend increase may not be signaling what you think.

Avoid these three mistakes and you read the signal more accurately than most professional analysts.

Investor Takeaway

Dividend increases are one of the few corporate actions that cost management something to get wrong. That is precisely why they carry information that words on a conference call cannot.

When you see a dividend announcement, don’t just glance at the new yield. Ask what management is committing to, why they are committing now, and whether the underlying cash flow story supports the commitment.

Visa, Amphenol, and MSCI each raised their dividend in the last year, and each told you something different. Visa committed to continued mid-teens compounding. Amphenol committed to a higher run rate built on a specific demand cycle. MSCI committed to a transparent payout-ratio policy tied directly to earnings.

Reading those signals is part of becoming an investor who can analyze a company on your own, rather than waiting for someone else to tell you whether the news was good or bad. The data is in the 8-K. The pattern is in the history. The signal is in the size of the move.

And with that, we will wrap up our discussion for today.

As always, thank you for taking the time to read today’s post, and I hope you find something of value on your investing journey. If I can further assist, please don’t hesitate to reach out.

Until next time, take care and be safe out there,

Dave

P.S. Dividend School exists for one reason: to help you analyze companies on your own, instead of waiting for someone to tell you whether the news was good or bad. If that's the kind of investor you want to be, paid subscribers get a new article like this every week, with full access to the archive, the dividend safety spreadsheet, and the frameworks I use myself. Subscribe and join us.