Union Pacific (UNP) Has Paid Dividends for 127 Straight Years.

The dividend is safe, covered twice over. The price is the problem, and the merger makes it bigger.

A free Dividend School deep dive. This is the same 12-section framework every Dividend School Pro deep dive runs on. In the paid version, the valuation work, the buy-below price, and the verdict sit behind the paywall. Today the whole thing is open.

The short answer: Union Pacific’s (UNP) dividend is safe, covered at 46% of earnings and 59% of free cash flow, but at $267 against our $224 buy-below the stock is a hold, and we would wait before adding.

Union Pacific is one of the 20 companies in our Dividend Universe, and it will stay there. It also won’t be anywhere near our Best Buys Now list on July 5th. Both of those things are true at once, and the gap between them is the most useful lesson in this piece.

1. The 127-year dividend and the biggest deal in railroad history

Union Pacific has paid a dividend for 127 consecutive years.

Sit with that number. The company mailed checks to shareholders through two world wars, the Great Depression, the stagflation of the 1970s, and the financial crisis. Almost nothing in American business has that kind of staying power.

And right now, this 160-year-old railroad is attempting the most audacious move of its modern life: buying Norfolk Southern to create America’s first true transcontinental railroad. The regulator just hit pause on the review.

So here’s the question this deep dive answers: when a wonderful, universe-quality business takes on the biggest deal in its industry’s history at a price above what we’d pay, what does a disciplined dividend investor actually do?

2. The bet

Union Pacific (UNP) owns an irreplaceable rail network across the western United States, and the bet is duopoly economics: only two railroads serve the West, pricing rises faster than inflation, and an improving operating ratio turns 3% revenue growth into high single digit earnings growth, year after year.

The dividend rides on top of that machine, covered roughly twice over by earnings.

The Norfolk Southern merger is the wild card, with the potential to extend the network coast to coast or to consume management’s attention and the balance sheet for years.

3. What the company does

Union Pacific moves heavy things long distances, cheaper than anyone else can.

The railroad operates in 23 western states per the Q1 2026 earnings release, connecting ports on the West Coast and Gulf to the middle of the country, with gateways to Mexico. Grain from Nebraska, chemicals from the Gulf, cars from Mexico, containers from the Port of Los Angeles. If it’s bulky and it’s west of the Mississippi, there’s a fair chance it rides UP rail.

Think of the network as a toll road that took 160 years to build and could never be built again. The land assembly alone makes a new transcontinental railroad impossible. That’s the asset you own a slice of.

One stat explains why shippers choose rail: a train moves a ton of freight three to four times farther per gallon than a truck. For heavy, non-urgent freight, rail wins on cost, and shippers have two choices in the West: Union Pacific or BNSF.

4. How they make money

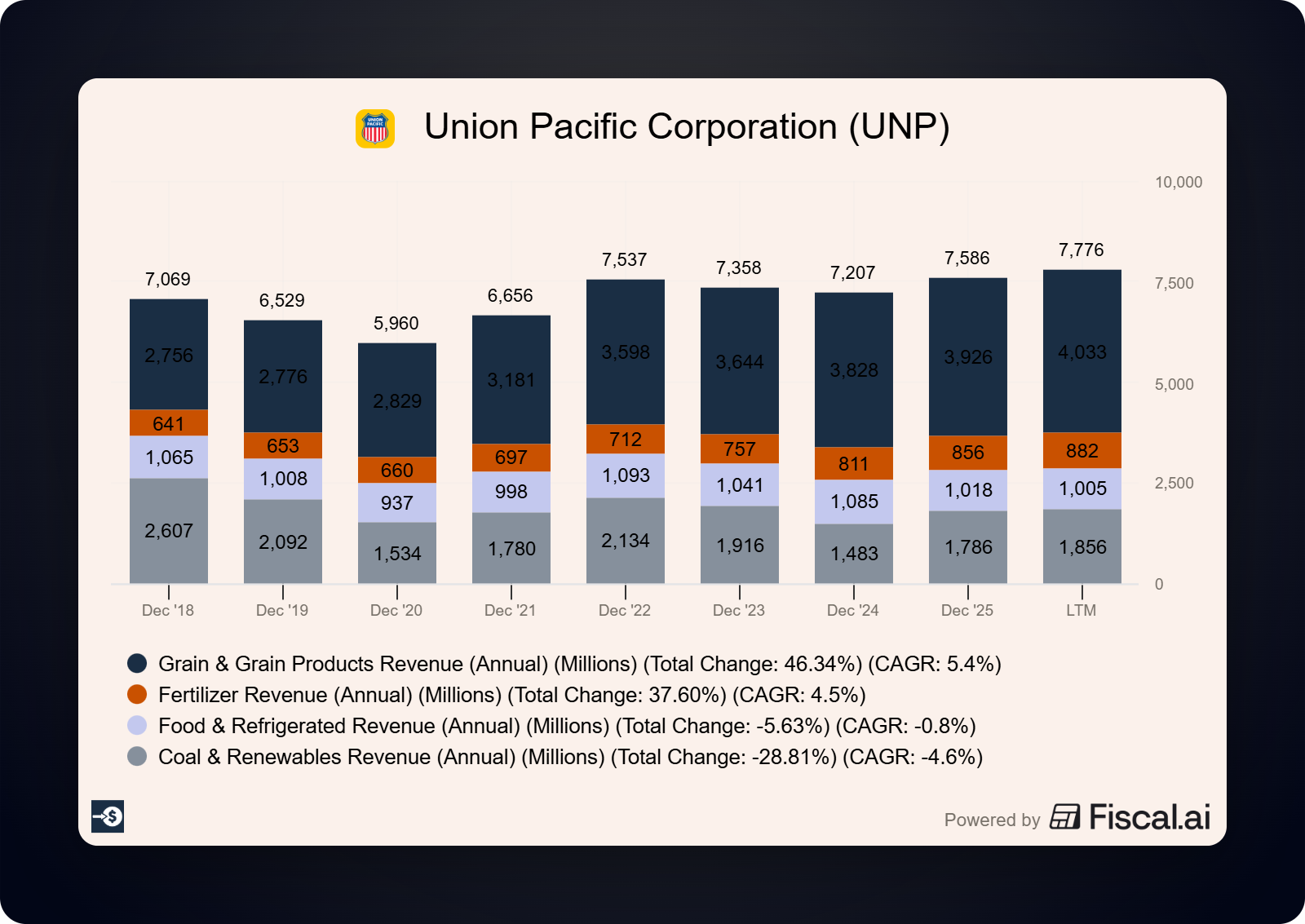

UNP charges per carload, and it reports freight revenue in three buckets. From the Q1 2026 earnings release:

Bulk (grain, fertilizer, coal, food): $2.0 billion, up 10%

Industrial (chemicals, metals, forest products, energy): $2.2 billion, up 5%

Premium (intermodal containers and automotive): $1.7 billion, down 5%

Total Q1 freight revenue came to $5.9 billion, up 4%, on 1% fewer carloads. Read that again: fewer cars, more revenue. Average revenue per car rose 4% to $2,829. That’s pricing power, the kind that shows up quarter after quarter when your customers have one alternative.

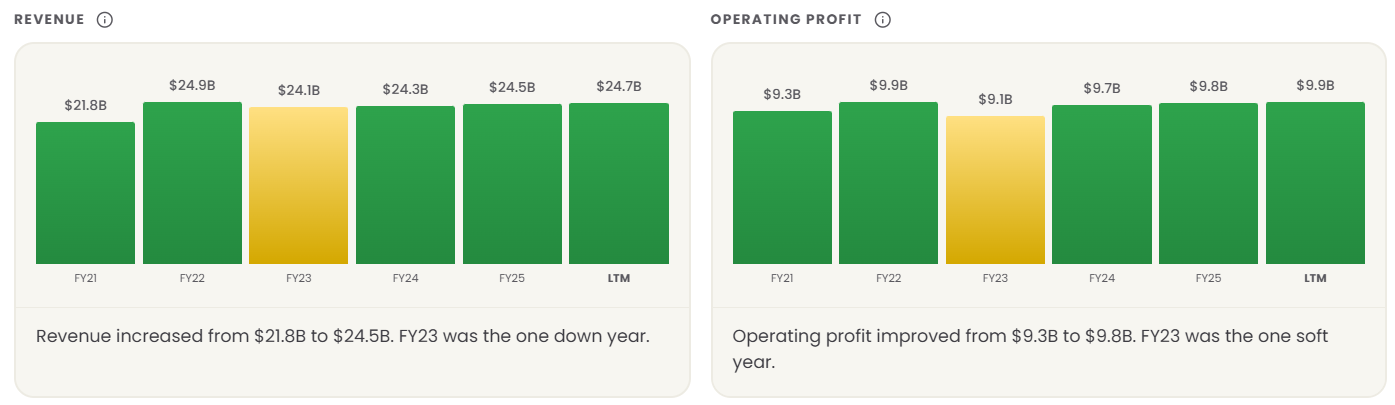

The full-year 2025 scoreboard, from the January 27, 2026 earnings release:

Operating revenue: $24.5 billion, up 1%

Net income: $7.1 billion, up 6%

Diluted EPS: $11.98, up 8% (versus $11.09 in 2024)

Cash from operations: $9.3 billion

And Q1 2026 set records: best-ever first quarter operating revenue ($6.2 billion), operating income, net income ($1.7 billion), and EPS of $2.87, with adjusted EPS of $2.93 up 9%.

A railroad posting record everything while carloads shrink is a business earning its profits from efficiency and price, and that’s the design.

This is the point where the paywall drops in a regular Dividend School Pro deep dive. Everything below, the dividend math, the merger risk, the valuation, and the verdict, is what subscribers get every month.

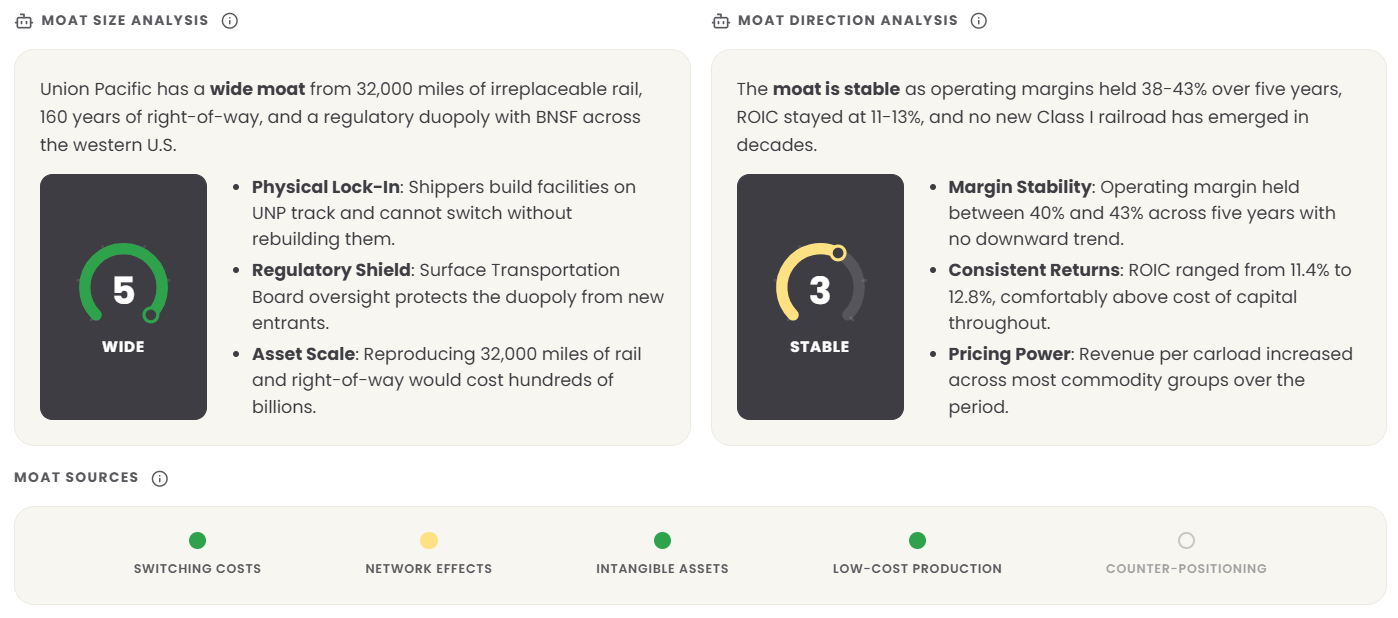

5. Moat and competition

This is one of the widest moats in our universe, and it comes from a simple fact: nobody can build another one.

Western rail is a duopoly. Union Pacific and BNSF (owned by Berkshire Hathaway) split the territory, and for many routes and commodities a shipper has exactly one practical rail option. Trucks compete at the margin for shorter, lighter hauls, but for coal, grain, and chemicals moving 1,500 miles, rail has no substitute.

The barriers stack on top of each other. The rights of way were assembled in the 1800s, partly by federal land grant. Regulation (the Surface Transportation Board) restricts entry and exit. And the cost advantage compounds with scale: longer trains, fewer employees per ton-mile, better fuel efficiency.

The numbers back the story. Q1 2026 workforce productivity hit 1,163 car miles per employee, up 7%, with average headcount down 5%, per the earnings release. Train length, terminal dwell, and locomotive productivity all set records. Management states the railroad earns an industry-leading operating ratio and return on invested capital, and the 60% number supports the claim.

The honest caveat: the same regulator that protects the duopoly also caps what UNP can extract from it. That tension is permanent, and it’s about to matter more than usual.

6. Financials

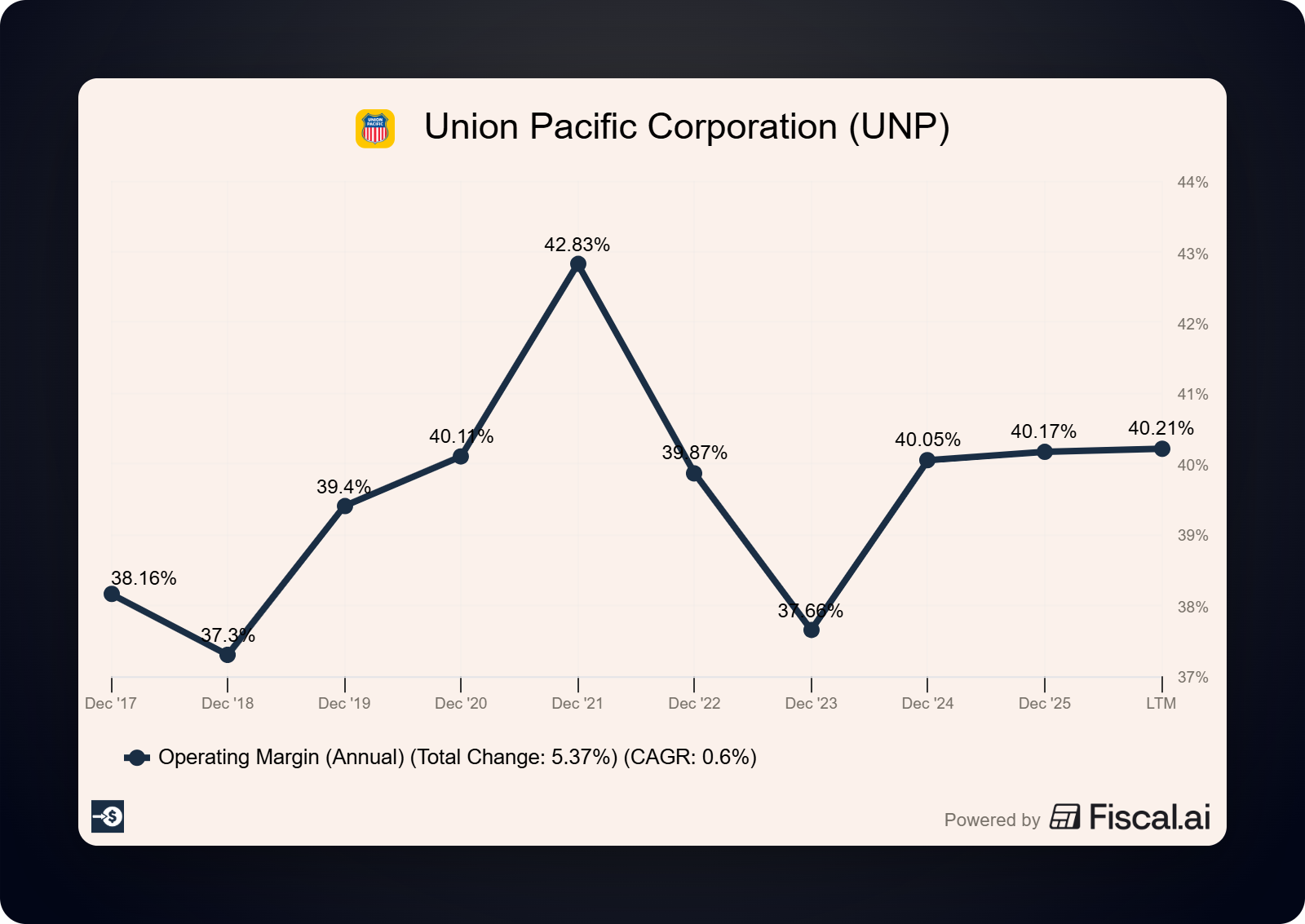

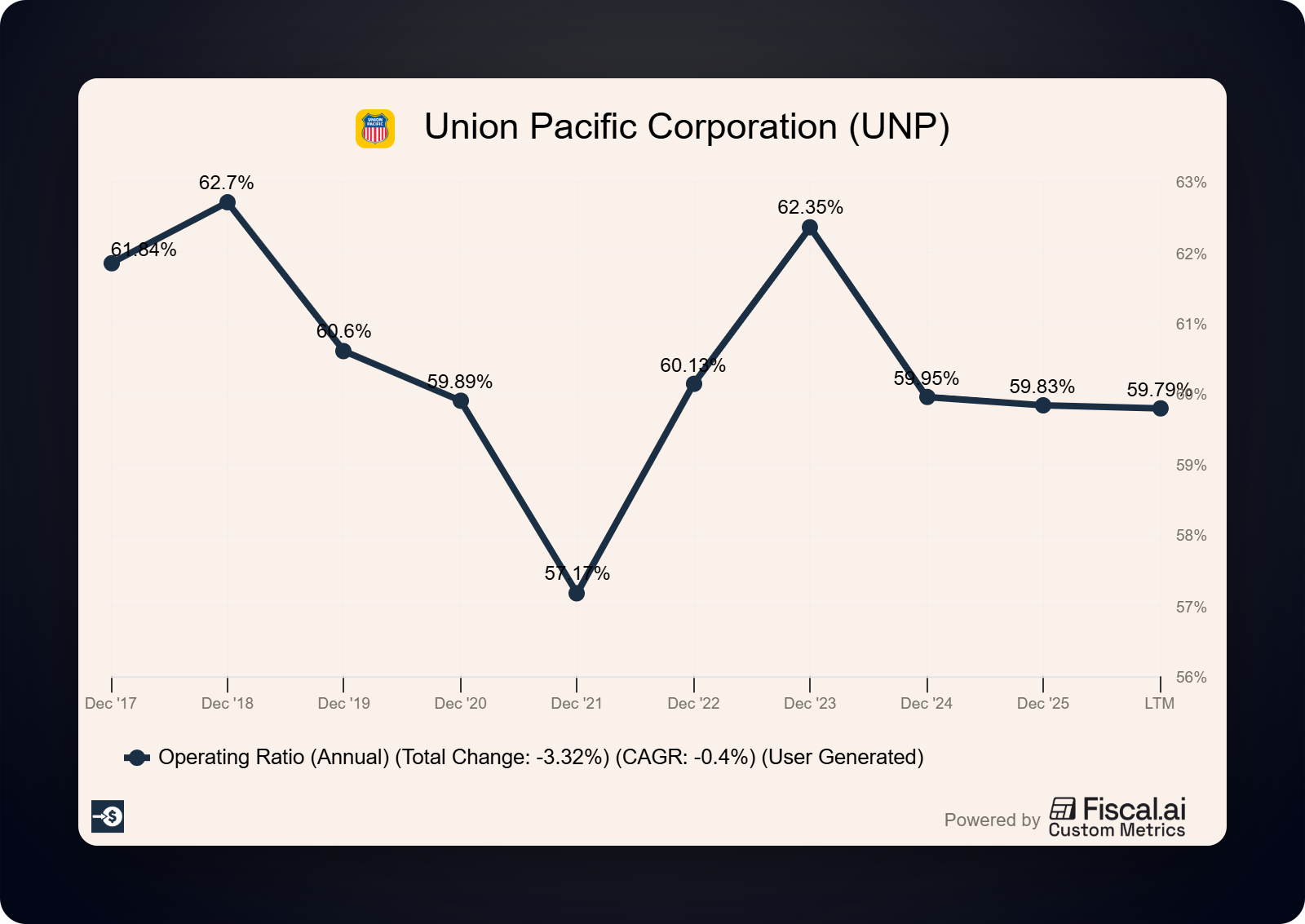

A railroad’s quality shows up in three places: the operating ratio, the cash conversion, and the balance sheet.

The operating ratio is operating expenses as a percent of revenue, and lower is better. Q1 2026 came in at 60.5% reported and 59.9% adjusted, an 80 basis point improvement per the earnings release. Getting under 60% puts UP at the front of the North American industry.

Cash conversion is the part beginners miss with railroads, so let’s do the math in the open. For full-year 2025:

Cash from operations: $9.3 billion

Capital investments: $3.8 billion

Free cash flow (our definition: operating cash flow minus capital spending): roughly $5.5 billion

Railroads eat capital. Track, locomotives, and bridges consume 15% of revenue every single year, and that spending never stops. Even after that burden, UP converts about 22 cents of every revenue dollar into free cash. That’s what 160 years of sunk infrastructure earns you.

The balance sheet, from the Q1 2026 release:

Total debt: $30.7 billion, down from $31.8 billion at year-end

Adjusted debt to adjusted EBITDA: 2.5x, improved from 2.7x

Q1 debt repaid: $1.2 billion

Notice the direction. Debt is going down, fast, and we’ll get to why in section 9.

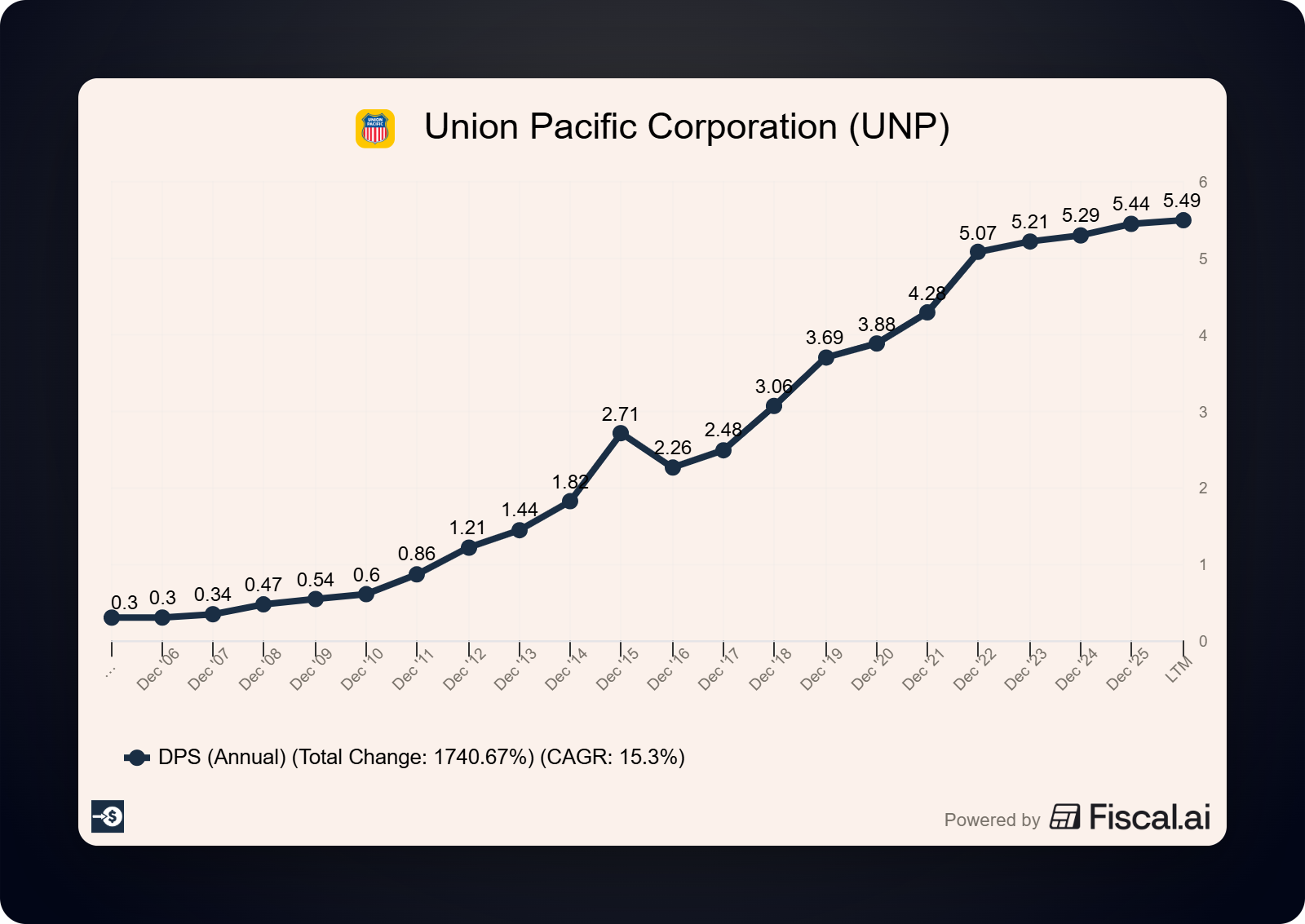

7. Dividend deep dive

The streak: Union Pacific has paid dividends for 127 consecutive years and has raised the payout for roughly two decades straight.

The current numbers:

Quarterly dividend: $1.38 per share ($5.52 annualized), declared for both Q1 and Q2 2026

Most recent raise: 3%, from $1.34

Yield at a $267 price: about 2.1%

Dividends paid per share in 2025: $5.44, up 3% from 2024

Now coverage, both ways.

On earnings: $5.52 annualized against $11.98 of 2025 EPS is a 46% payout ratio. On free cash flow: roughly $3.25 billion of dividends paid in 2025 against $5.5 billion of free cash flow is a 59% payout. Both sit in the safe zone with room for raises even in a recession year.

This is what coverage is supposed to look like. Hold it next to the Texas Instruments piece we published alongside this one and the contrast teaches the whole lesson: TXN pays out 116% of free cash flow, UNP pays out 59%.

One yellow flag, and it’s an honest one: the raise pace has slowed to 3%, beneath the company’s longer-run pace (dividend growth averaged high single digits over the past decade). Management is conserving cash for the merger. The 2026 outlook in the Q1 release still commits, in writing, to “consistent annual dividend increases.”

Our dividend safety read: Safe, and arguably Very Safe on the numbers alone. The only reason we grade it A- and watch the file is the merger, because a deal this size reshuffles every capital allocation priority around it.

8. Growth prospects

A railroad can’t grow its track, so growth comes from four smaller levers pulling together.

Pricing above inflation is lever one, and the Q1 release confirms it: core pricing gains drove revenue growth, and management’s stated outlook is “pricing dollars in excess of inflation dollars.” Lever two is efficiency, the march from a 60% operating ratio toward the mid-50s, where every basis point drops straight to operating income. Lever three is volume mix, with grain, coal exports, and Mexico trade running strong (bulk revenue up 10% in Q1) while intermodal stays soft. Lever four is the buyback, currently paused, which historically retired 1 to 2% of shares each year.

Management’s stated targets, affirmed in the Q1 2026 release: mid-single-digit EPS growth in 2026, on track to a three-year EPS CAGR of high single to low double digits through 2027.

Then there’s the merger. A combined UP and Norfolk Southern would be the first single-line transcontinental railroad in American history, eliminating the Chicago interchange where freight sits for days. The efficiency prize is real. So is the price tag, the integration risk, and the regulatory gauntlet. We treat the merger as a free option: zero value in our numbers, with the risks counted separately in section 10.

For the dividend, the arithmetic is friendly either way: a 46% earnings payout growing with mid-single-digit EPS supports 5%+ dividend growth once the merger resolves.

9. Management and capital allocation

CEO Jim Vena is an operator’s operator, a Hunter Harrison disciple who took the job in 2023 and has delivered record operating metrics nearly every quarter since. The Q1 safety and productivity numbers (terminal dwell down 11%, freight car velocity up 9%) are his fingerprints.

The capital allocation picture changed completely with the merger, and the Q1 2026 cash flow statement shows it plainly:

Share repurchases, Q1 2026: zero (versus $1.7 billion a year earlier)

Debt repaid, Q1 2026: $1.2 billion

Dividends paid, Q1 2026: $821 million, up from $804 million

Buybacks stopped. Debt paydown accelerated. The dividend kept growing. That’s the standard playbook for financing a mega-deal while defending a credit rating. The priority order (dividend protected, buyback sacrificed) is what income investors want to see.

The watch item: UP will issue a large slug of new shares to pay for Norfolk Southern. Every share issued dilutes your claim on the dividend stream, and the deal math has to earn that back through cost savings and new traffic. That’s a multi-year show-me story.

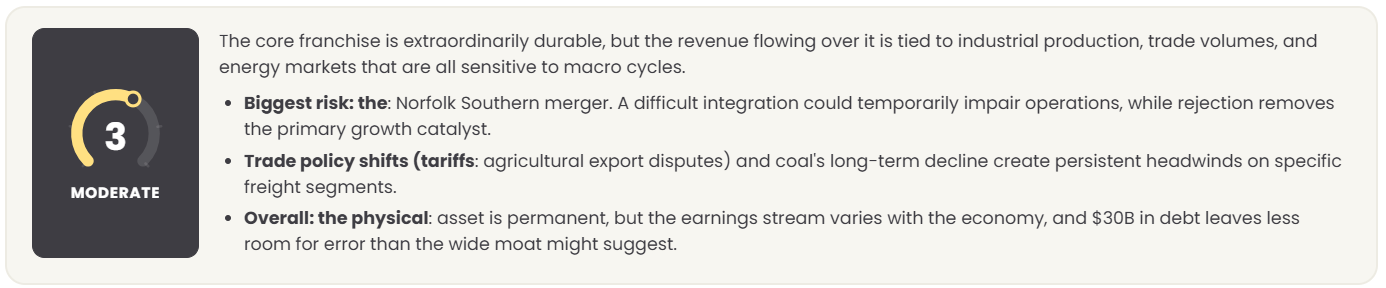

10. Risks

Ranked by what matters most.

The merger is risk one, two, and three. The Surface Transportation Board found the original application incomplete in January 2026, accepted a revised application on May 28, 2026, but is holding proceedings in abeyance with supplemental information due July 27, 2026. Translation: the regulator has questions about competition, shipper access, and service that UP hasn’t answered to its satisfaction. The range of outcomes runs from approval with painful conditions, to years of limbo, to outright rejection after enormous sunk costs. UP also inherits exposure to Norfolk Southern’s Eastern Ohio derailment liabilities if the deal closes, per the risk factors in UP’s own Q1 2026 release.

Risk four is the freight economy. Management’s own outlook calls the economic forecast muted. Intermodal carloads fell 9% in Q1, and automotive fell 6%. A consumer recession hits the Premium segment directly.

Risk five is coal’s long goodbye. Coal and renewables revenue jumped 17% in Q1 on export strength, but the decade-long trajectory of domestic coal is down, and it remains a meaningful bulk commodity.

Risk six covers the permanent ones: derailments, labor relations, and a regulator that can turn hostile, especially with a merger pending.

The bear case in one line: you pay 22 times earnings for a slow-growth railroad that spends the next three years distracted, diluted, and arguing with its regulator.

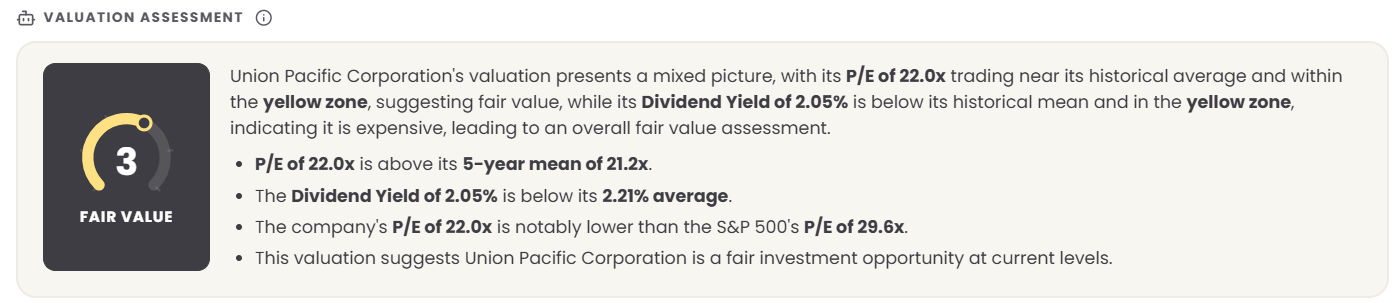

11. Valuation: a reverse DCF

A regular discounted cash flow (DCF) guesses at growth and produces a price. A reverse DCF starts from the price and solves for the growth the market is already paying for. Then you judge whether that growth is believable. (We walk through the same method in the Texas Instruments piece published earlier.)

Our inputs: an 8.2% discount rate (UNP’s weighted average cost of capital), a 4.5% terminal growth rate (anchored to the current 10-year Treasury yield), and a 10-year growth stage.

The 10-year treasury acts as our terminal rate for a simple reason, we can’t reliably “guess” at a rate longer than 10 years. And it can act as a proxy for our minimum return to best.

At $267 per share on 593.6 million diluted shares, the market values Union Pacific at near $158 billion.

Run the math on 2025’s $5.5 billion of free cash flow, and here’s what the price assumes:

4.7% annual FCF growth for the next decade

That’s a sane number, and that’s the problem. It’s higher than the company’s past performance, and we haven’t factored in the potential merger.

Here’s the historical FCF ranges:

3-year: 1.88%

5-year: 0.22%

10-year: 4.03%

Management targets mid-single-digit EPS growth for 2026 and high single digits through 2027, so today’s price assumes the plan works, hands you the merger for free, and leaves nothing over for disappointment.

Now the same math at our buy-below:

At $224: 2.6% implied growth, below inflation

Pay $224, and you own a railroad priced to grow slower than the economy, with every basis point of pricing power, efficiency gain, and merger upside as your margin of safety.

One honest caveat: the 4.5% terminal rate is generous, which flattens the hurdle. These implied growth rates are floors. Another caveat: any company growing slower than GDP or 10-year Treasury rates doesn’t earn our money.

There’s slow, and there’s too slow.

For context, $267 is also 22 times trailing EPS of $12.15 (2025’s $11.98, minus Q1 2025’s $2.70, plus Q1 2026’s $2.87), the top of UNP’s usual 18 to 22 times range. The reverse DCF and the multiple agree: priced for everything going right.

Nothing about that math says sell. All of it says don’t add here.

12. Why It’s Part of the Universe

Union Pacific stays in the Dividend Universe without debate: the moat is generational, the dividend is covered twice over by earnings, and management just demonstrated, in real dollars, that the payout outranks the buyback.

But, it will not be on the July 5th Best Buys Now list, because membership in the universe answers one question and price answers another. At $267 against a $224 buy-below, you’re paying full fare for a railroad that is about to spend years and billions on the most complicated merger in its history.

If you own it: keep collecting the 2.1%, reinvest elsewhere, and let the streak do its work. If you don’t: put it on the list and wait. Railroads sell off twice a decade like clockwork, on recession fear or regulatory headlines, and the next scare is your entry.

What would change our mind, in either direction: a price below $224 makes this a buy regardless of the merger noise. STB approval with clean conditions would justify raising the buy-below. A dividend freeze to fund the deal or a credit downgrade below strong investment grade would trigger a full-universe review.

Wonderful company, wrong price. That sentence is most of what Dividend School Pro exists to tell you, month after month.