These 5 Dividend Stocks Are Dirt Cheap (July 2026)

Five stocks from this month's 'undervalued' lists. My tools say only three are cheap

Every month a fresh batch of “undervalued dividend stock” lists lands in your inbox. Most of them stop at the yield and a cheap-looking multiple.

That is where the mistake starts.

A low price tells you the market is nervous. It does not tell you whether the dividend is safe, whether the business is growing, or whether the moat still holds. Those answers decide whether a cheap stock is a gift or a trap.

Today we are going to run five dividend payers through the same valuation process I use, then pressure-test each one on safety, growth, moat, and risk. They span four sectors, and they range from genuinely cheap to merely fair. The tools will show you which is which.

None of these are buy recommendations. Think of them as candidates worth your homework and a live example of how to grade a cheap-looking stock before it earns a place in your portfolio.

In today’s post, we will discuss:

The three-tool valuation process (P/FCF, DCF scenarios, reverse DCF)

PepsiCo and Healthpeak, including how to value a REIT the right way

Three more names behind the paywall, where the tools get more interesting

A scorecard you can save and reuse

Okay, let’s dive in.

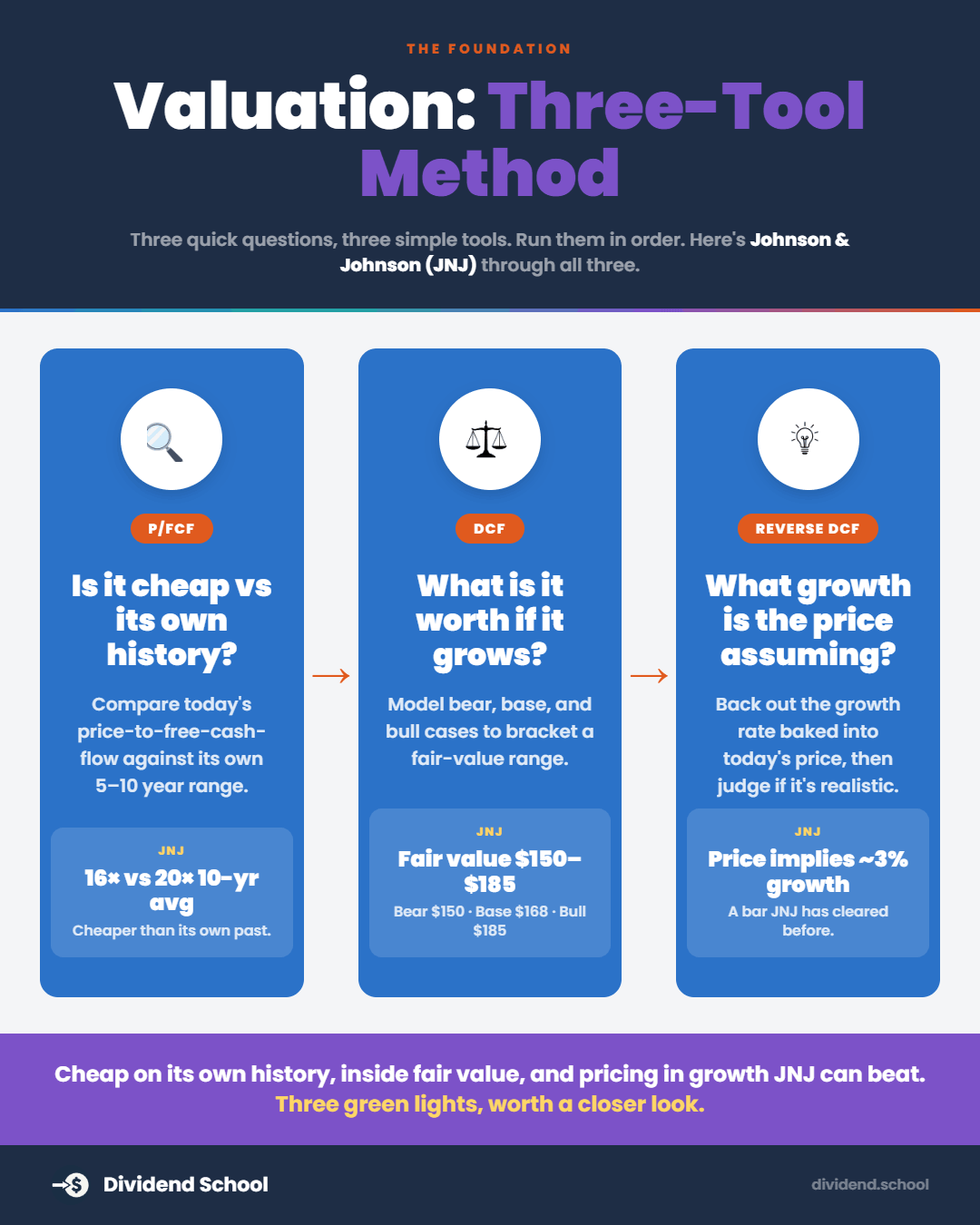

How to read a valuation before you trust it

I lean on three tools from Stock Simplifier, and each one answers a different question.

Price to free cash flow (trailing) asks, “Is the stock cheap versus its own history?” It plots today’s P/FCF multiple against the five-year average and colors the zones. Green is attractive, yellow is fair value, red is expensive. Simple, and it keeps you honest about what you are actually paying for a dollar of cash flow.

A discounted cash flow (DCF) asks, “What is the business worth if it grows at X?” I never trust a single DCF number. I look at a bear, base, and bull scenario, because the spread tells you how much of the value depends on optimism.

A reverse DCF flips the question: “What growth does today’s price already assume?” This one is my favorite. You solve for the growth rate baked into the current price, then ask whether the business can clear that bar.

Here is the part most lists skip.

Valuation is only half the job. A stock can screen cheap on all three tools and still be a bad idea if the dividend is stretched, the moat is cracking, or free cash flow is shrinking. So for each name below, we pair the valuation read with the dividend-safety math and the business risks. That is the whole point.

Let’s meet the candidates.

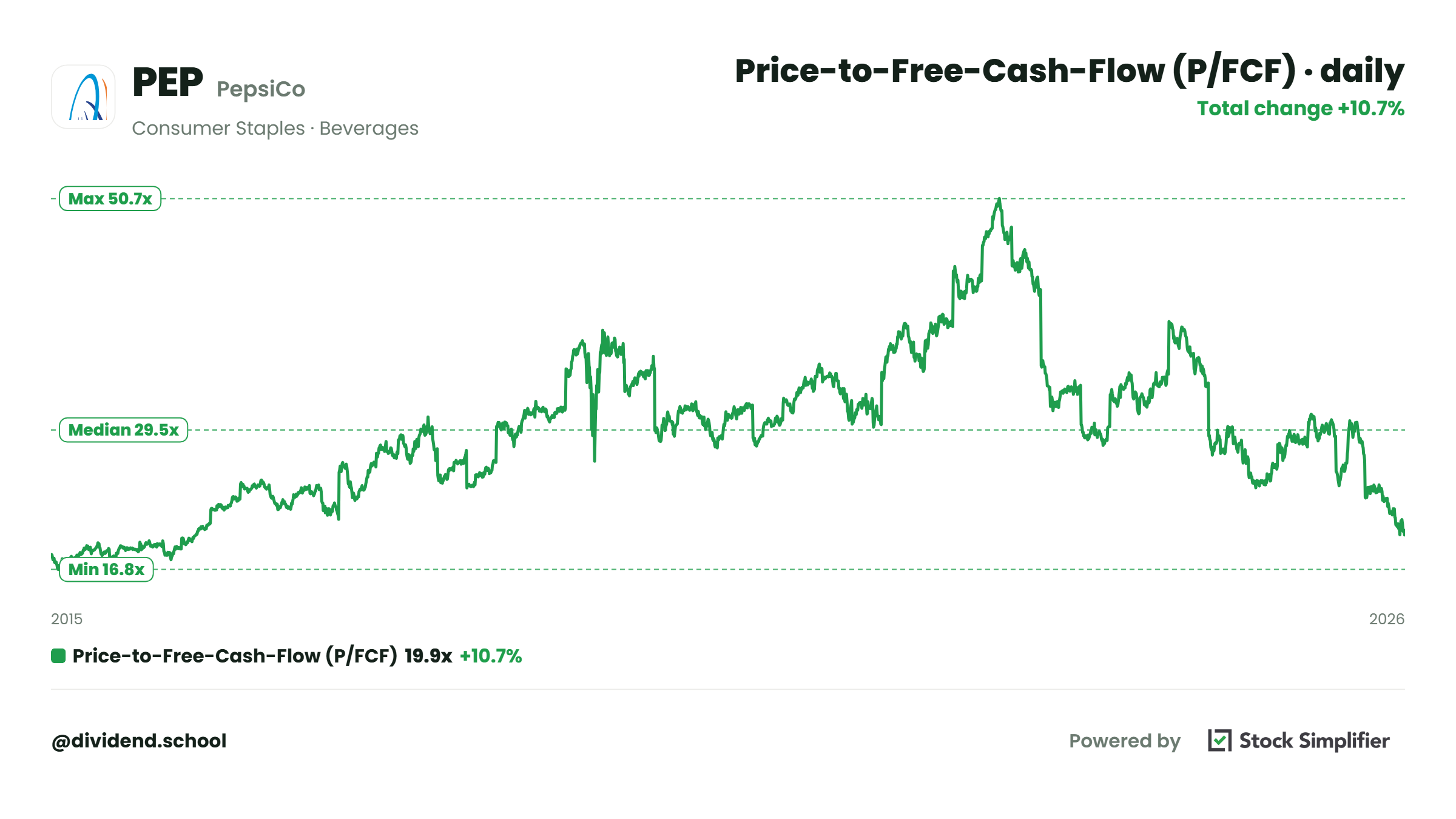

1. PepsiCo (PEP): the low bar hiding in plain sight

Pepsi needs no introduction. Lay’s, Doritos, Gatorade, Quaker, and the Pepsi brand itself, delivered through a direct-store network that stocks the shelf for you.

On valuation, the stock is cheap versus its own past.

P/FCF (trailing): 19.9x versus a 5-year average of 32.8x (attractive zone)

DCF base case (10% / 5% growth): $188.86, roughly 40% above the recent price near $135

DCF bear case (5% / 0%): $126.95, about 6% below

Reverse DCF: the price implies just 2.5% revenue growth a year for a decade

That 2.5% is the number to sit with. The market is pricing Pepsi to barely grow, and a 54-year dividend raiser trading like a no-growth business is worth a look.

Now the safety check, and here it gets more interesting.

Per PepsiCo’s FY2025 10-K (filed February 3, 2026), the company paid $7,638 million in dividends against roughly $8,200 million in free cash flow. That is a payout near 93% of free cash flow. On core earnings the payout is a more comfortable 68%, but the cash math leaves little cushion if free cash flow stalls.

The dividend itself is not in question. Pepsi has raised it for 54 straight years and lifted it 4% in February 2026 to $5.92 a share. What you are underwriting is the cash cushion behind that streak.

Growth is the soft spot. Revenue rose just 0.4% in 2024 and organic sales grew 1.7% in 2025, while a $1,993 million writedown tied largely to the Rockstar energy brand dragged GAAP earnings lower.

The risks worth weighing: GLP-1 weight-loss drugs denting snack and soda demand, tariffs pushing up commodity costs by 6 to 11 percentage points per segment, and acquisitions that keep producing impairments.

The verdict for your process: a wide-moat compounder priced for almost no growth, with a dividend that is safe on the streak but tight on cash. Worth the homework, especially if you believe Pepsi clears a 2.5% bar in its sleep.

2. Healthpeak (DOC): value a REIT the right way

Healthpeak is a healthcare REIT that owns outpatient medical buildings on hospital campuses and lab space in the top life-science markets.

Before the numbers, one correction that trips up most people.

You cannot value a REIT on standard free cash flow. Healthpeak’s reported GAAP free cash flow shows a tiny 2.3% margin, because real-estate depreciation is a massive non-cash charge that buries true cash generation. REITs solve this with two custom metrics.

Funds from operations (FFO) adds depreciation back. Treat it as the REIT’s version of earnings, so P/FFO is the REIT’s P/E.

Adjusted FFO (AFFO) strips out maintenance costs. Treat it as the REIT’s version of free cash flow, so P/AFFO is the REIT’s P/FCF.

Run the multiples off the per-share figures at a recent price near $21.77:

P/FFO: 11.8x (using FFO of about $1.85 a share)

P/AFFO: 13.3x (using AFFO near $1.64 a share)

Reverse DCF on FFO: with 8.5% near-term growth, the price only needs 1.1% growth a year after year three

Both multiples sit at the low end of where healthcare REITs trade, and the reverse DCF shows the market expecting almost no growth past the near term.

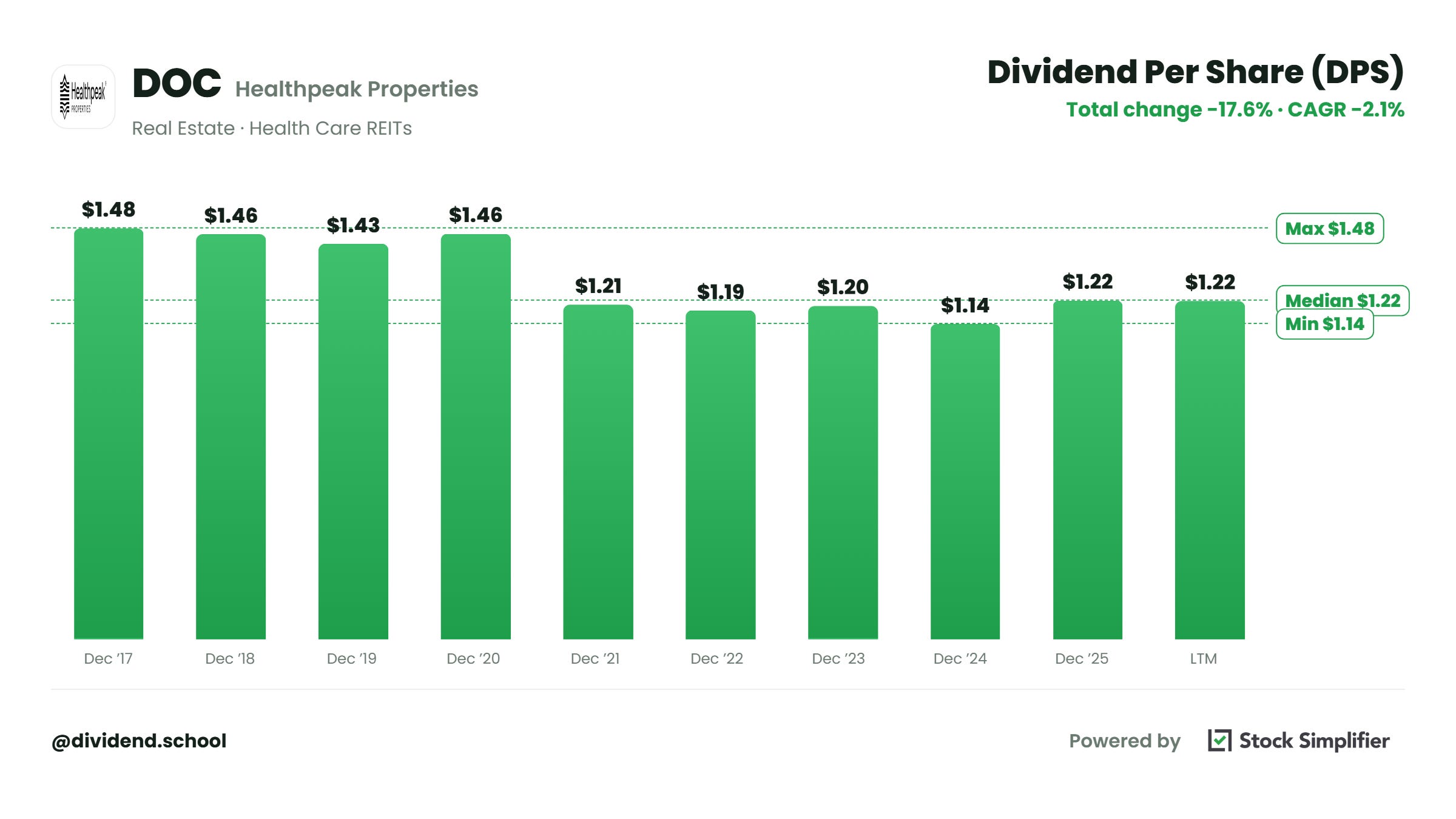

The dividend needs its own honest look. Healthpeak pays monthly, $0.10167 a share, or $1.22 a year, a yield near 5.6%. Against 2026 FFO-as-adjusted guidance of $1.71 to $1.75 (midpoint $1.73), the payout runs in the low 70s percent, and on AFFO near $1.64 it lands around 74%. Well covered.

One thing the yield-chasers miss: this is not an unbroken grower. Healthpeak cut its dividend in 2020 (from $1.48 to $1.20 annualized) while it exited senior housing and repositioned. It moved to a monthly payout in 2025 and has held it steady since.

The moat is in the buildings. Outpatient medical space physically attached to a hospital campus keeps physician tenants in place, and retention ran near 79% in 2025. Life-science clusters in South San Francisco, Boston, and San Diego are hard to replicate.

The risks are real and current. Lab oversupply pushed same-store life-science income negative in early 2026, the stock is sensitive to interest rates, and the March 2026 Janus Living senior-housing spinoff (Healthpeak kept about 82%) changed the earnings mix.

The verdict for your process: a well-covered high-yield REIT trading cheap on the metrics that matter, with a lab-vacancy overhang you need to have a view on. The dividend cut in its history is a reminder to underwrite the coverage behind the yield.

Below the paywall, three more names and the board that ties it together:

The cheapest, best-covered stock of the five. A Dividend Aristocrat with a 49-year raise streak that the market has priced for 0.4% annual growth. It swept all four questions on the scorecard.

A 48-year raiser yielding over 5% where the tools disagree with the “deep value” label. The disagreement is the lesson, and it comes with 21% downside in the bear case.

A quality compounder in disguise. A 30% free cash flow payout, 13% revenue growth, and a 15% dividend raise in April. The most cushion on the list, if the growth holds.

The one-page scorecard grading all five on valuation, growth bar, and coverage. Save it and run your own candidates through it.

Members get this workup every month, plus the full Dividend Universe with Buy Below prices and safety scores, and a premium email every week on a predictable schedule.

$369 a year, 30-day money-back guarantee, cancel anytime.