The Dividend Reinvestment Plan (DRIP): Your Portfolio’s Compounding Engine

What if every dividend payment you received automatically bought more shares, which then paid more dividends, which bought even more shares? That is the core promise of a Dividend Reinvestment Plan (DRIP).

Albert Einstein reportedly called compound interest the eighth wonder of the world. Whether he actually said it is debatable. What is not debatable is the math behind compounding, and DRIPs are one of the simplest tools dividend investors have to put that math to work.

In today’s post, we will cover how DRIPs work mechanically, walk through the real math of reinvesting dividends over time, examine the benefits and drawbacks, and help you decide whether a DRIP belongs in your investing process.

Let’s dive in.

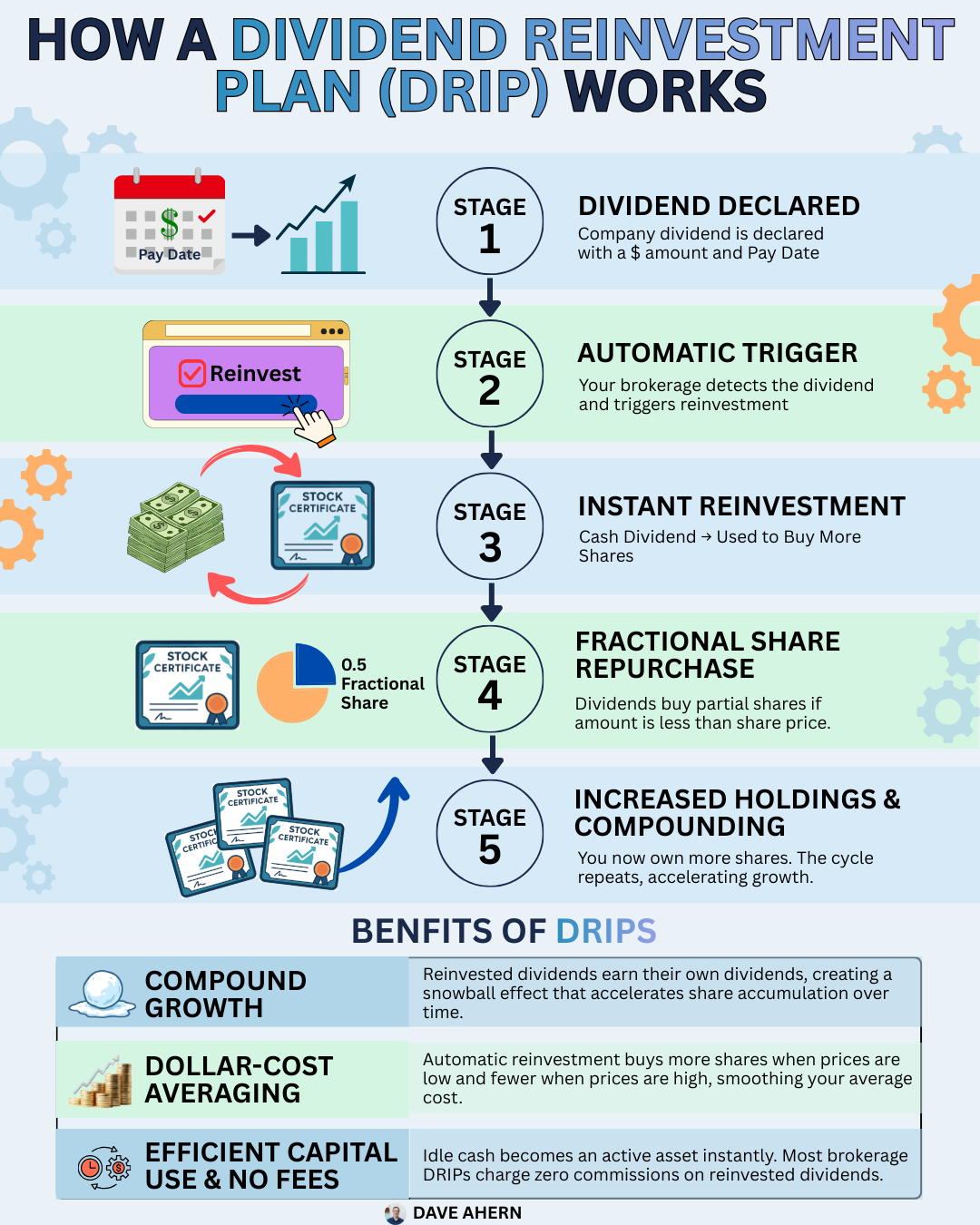

What Is a DRIP?

A Dividend Reinvestment Plan (DRIP) is a program that automatically reinvests your cash dividends into additional shares (or fractional shares) of the company that paid them. Instead of receiving a cash deposit in your brokerage account, the dividend payment purchases more stock on your behalf.

Think of it like a snowball rolling downhill. Each dividend payment adds a thin layer of snow. That slightly bigger snowball catches a little more snow on the next rotation. Over the years and decades, the snowball grows far larger than the original ball you started with.

DRIPs come in two main flavors.

Brokerage DRIPs. Most major brokerages (Fidelity, Schwab, Vanguard) offer DRIP functionality at no cost. You toggle it on in your account settings, and your dividends automatically reinvest. This is the most common type and the one most investors will use.

Company-Sponsored DRIPs. Some companies run their own DRIP programs directly. These sometimes offer shares at a small discount (typically 1% to 5%) to the market price and may waive commission fees. Companies like Coca-Cola, Johnson & Johnson, and Procter & Gamble have historically offered direct plans, though availability and terms change over time.

The mechanics are straightforward. You own 100 shares of a company. The company pays a quarterly dividend. Instead of that cash landing in your account, the DRIP uses it to buy more shares at the current market price. Next quarter, you own slightly more shares, so your dividend payment is slightly larger. Repeat for decades.

The Math Behind DRIPs: Why Compounding Matters

To see why DRIPs are powerful, we need to understand how reinvested dividends compound. Let’s walk through a simplified example to illustrate the concept.

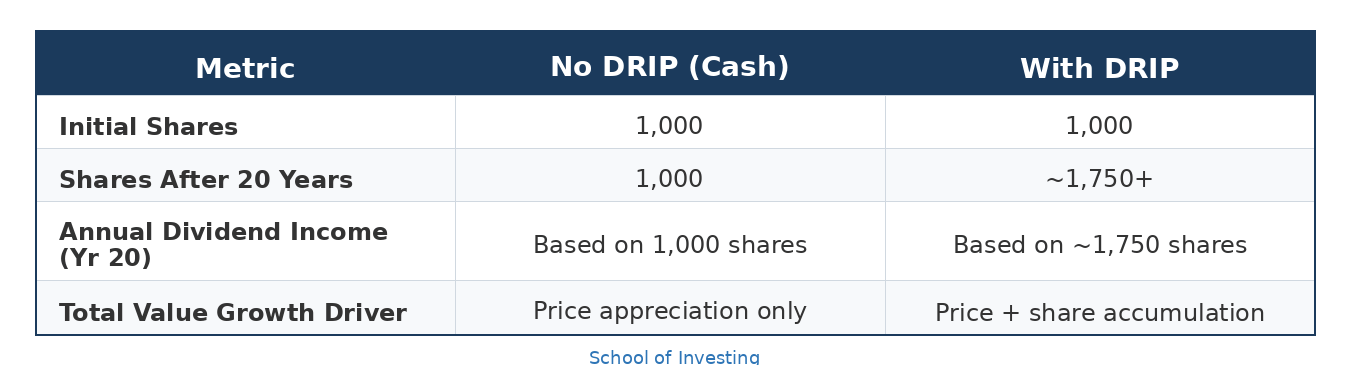

Imagine you buy 1,000 shares of a company at $50 per share, totaling $50,000. The company pays a 3% annual dividend yield and increases it by 7% each year. The stock price appreciates at 7% annually as well.

Scenario A: Take the Cash

You collect dividends as cash. After 20 years, you still own 1,000 shares. Your annual dividend income has grown thanks to the company’s dividend increases, but your share count never changed.

Scenario B: DRIP Reinvestment

You reinvest every dividend. Each quarter, those payments buy additional shares. Those new shares will generate dividends in the following quarter. After 20 years, you own significantly more shares.

Here is the approximate comparison over 20 years.

The critical difference is the share count. The DRIP investor owns roughly 75% more shares after 20 years. Those extra shares all generate dividends, creating a self-reinforcing cycle. The exact numbers will vary depending on the stock price at each reinvestment date, dividend growth rates, and other variables, but the principle holds: reinvesting dividends accelerates wealth building.

This is the compounding engine at work. Your dividends earn dividends, which earn more dividends.

Real-World Context: How Dividend Growth Powers DRIPs

The power of a DRIP depends heavily on the quality of the underlying business. A DRIP on a company with a shrinking dividend does you no favors. But a DRIP on a company that consistently grows its dividend can produce remarkable results.

Consider the characteristics that make a company ideal for DRIP investing. The business needs to pay a reliable dividend, grow it over time, and maintain financial health to sustain those payments.

This is where our analytical framework comes in. The metrics we have discussed throughout the School of Investing matter here: strong returns on invested capital (ROIC), manageable payout ratios, consistent free cash flow generation, and durable competitive advantages. These are the traits that allow companies to increase dividends year after year.

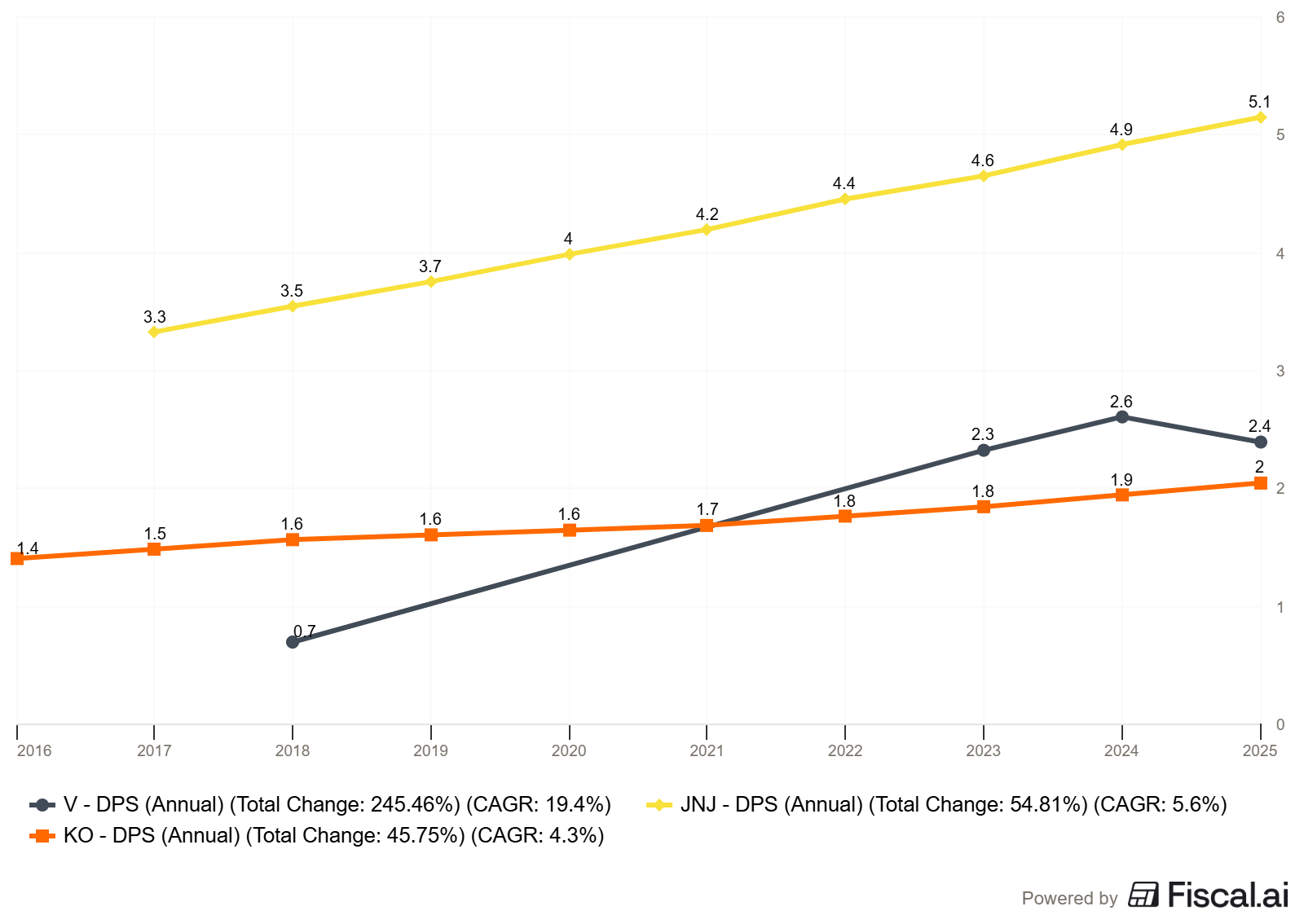

For example, companies in the payment processing space, like Visa and Mastercard, have grown their dividends at high rates because of the capital-light business models we discussed in our payment processing deep dive. Their ability to generate substantial free cash flow relative to the capital required to run the business gives them the capacity to return cash to shareholders consistently.

On the other hand, companies like the airlines Buffett famously criticized (capital-hungry businesses generating low returns) make poor DRIP candidates. The dividend, if one exists, is unreliable because the business itself is unreliable.

The lesson: a DRIP is only as good as the business behind the dividend.

Benefits of DRIPs

Automatic Discipline

The biggest advantage of a DRIP is behavioral. It removes the decision point. You do not have to decide whether to reinvest, when to reinvest, or how much to reinvest. The program handles it automatically. For most investors, this “set it and forget it” approach eliminates the temptation to spend dividend income or to time the market with reinvestment decisions.

Dollar-Cost Averaging

Because DRIPs reinvest at regular intervals regardless of the stock price, you benefit from dollar-cost averaging. When the stock price drops, your dividends buy more shares. When the price rises, they buy fewer. Over time, this smooths out your average cost per share. You end up buying more shares when they are cheap and fewer when they are expensive, which is exactly the behavior we want as value investors.

Fractional Shares

Most DRIP programs allow you to purchase fractional shares. If your quarterly dividend is $75 and the stock trades at $200, the DRIP buys 0.375 shares. Without this feature, that $75 would sit as uninvested cash. Fractional share purchasing ensures every dollar of your dividend goes to work immediately.

Commission-Free Reinvestment

Brokerage DRIPs and most company-sponsored plans reinvest without charging commissions. While commissions have largely disappeared for standard stock trades, this was a significant advantage historically and remains relevant for company-sponsored plans.

Compounding Acceleration

As we demonstrated in the math section, reinvested dividends buy additional shares that generate their own dividends. This creates a compounding loop that accelerates over time. The effect is modest in the early years but becomes substantial over the long term. Patient investors benefit most.

Drawbacks and Considerations

DRIPs are not a magic bullet. There are legitimate reasons an investor might choose not to use one, and understanding the trade-offs matters.

Tax Complications

This is the biggest practical downside. Reinvested dividends are still taxable income. Even though you never see the cash, the IRS treats the dividend as income in the year it was paid. Each reinvestment also creates a new tax lot with its own cost basis and purchase date. Over 20 years of quarterly reinvestments, you could have 80+ separate tax lots for a single stock. Tracking cost basis can be tedious, though most brokerages now handle it automatically. If you hold DRIPs in a tax-advantaged account (IRA or 401k), this issue disappears entirely.

No Control Over Purchase Price

A DRIP reinvests on the dividend payment date at whatever the market price happens to be. You cannot wait for a dip or exercise any judgment about valuation. For a value-conscious investor, this can feel uncomfortable. However, over long holding periods, this disadvantage tends to wash out through the dollar-cost averaging effect.

Concentration Risk

DRIPs automatically reinvest back into the same stock that paid the dividend. If you own 10 stocks and one of them has a much higher yield, the DRIP will funnel more capital into that one position over time. This can slowly skew your portfolio allocation without you realizing it. Periodic portfolio reviews help catch this.

Opportunity Cost

Sometimes the best use of dividend income is not reinvesting it in the same stock. Perhaps another company in your portfolio (or watchlist) offers better value at that moment. Taking dividends as cash gives you the flexibility to allocate that capital wherever the opportunity is greatest. Buffett himself often takes dividends as cash from his holdings and redeploys them into whatever opportunity he finds most attractive.

Forced Buying in Overvalued Markets

A DRIP buys shares regardless of valuation. If a stock runs up to a price-to-earnings ratio of 40 and you believe fair value is closer to 20, the DRIP will still reinvest your dividend at that elevated price. For investors who care deeply about the price they pay (and we should, as Buffett reminds us), this is a real consideration.

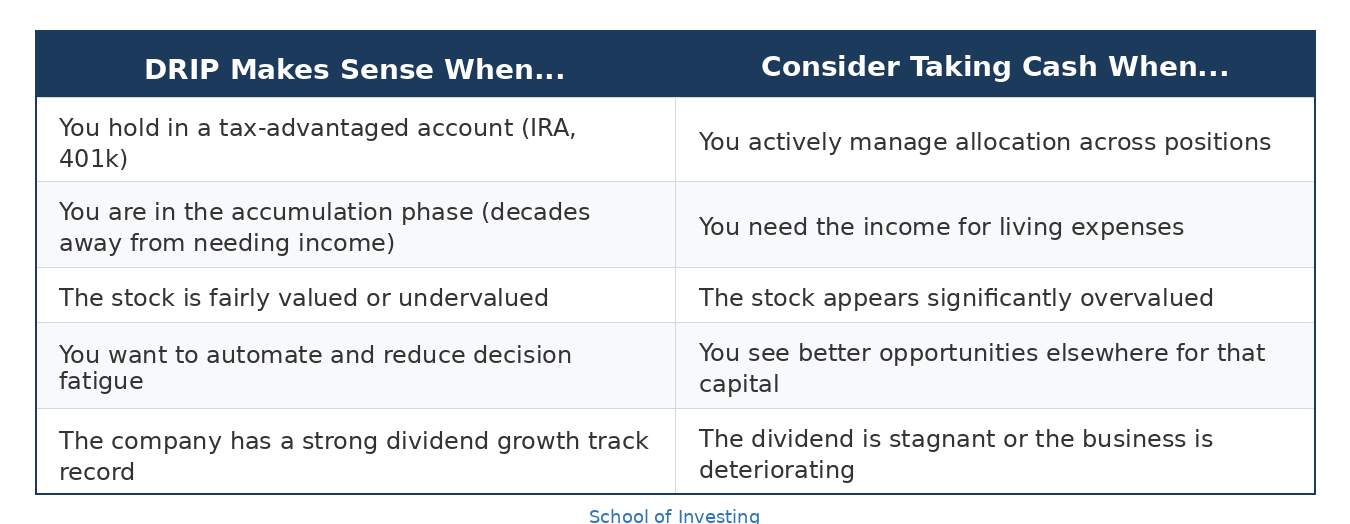

DRIP Decision Framework

To help you decide, here is a simple framework.

How to Set Up a DRIP

Setting up a DRIP is straightforward with most brokerages.

Step 1: Log in to your brokerage account and navigate to the dividend reinvestment settings. Most brokerages place this under account settings or the individual stock’s detail page.

Step 2: Choose whether to enable DRIP for your entire portfolio or for individual stocks. I recommend setting it at the individual stock level. This gives you the flexibility to reinvest dividends from your highest-conviction holdings while taking cash from others.

Step 3: Confirm fractional share support. Most major brokerages support fractional shares for DRIP, but verify this for your specific platform.

Step 4: Review quarterly. Even with DRIP enabled, review your positions each quarter. Check that your portfolio allocation has not drifted significantly and that the businesses behind your dividends remain healthy.

For company-sponsored DRIPs, you will typically enroll directly through the company’s transfer agent (often Computershare or EQ Shareowner Services). These may require minimal investments and have their own enrollment forms.

DRIPs and the Buffett Framework

Warren Buffett’s approach to capital allocation offers a useful lens for thinking about DRIPs. As we have explored in previous articles, Buffett loves businesses that generate high returns on invested capital with minimal capital requirements. See’s Candies is his dream business precisely because it generates substantial returns relative to the capital invested.

When you enable a DRIP, you are essentially making a capital allocation decision: you are choosing to reinvest in the same business. Buffett himself has said, “There’s no rule that you have to invest money where you’ve earned it.” Sometimes the best use of earnings (or dividends) is to deploy them elsewhere.

This means DRIPs work best when you have high conviction in the business and believe the stock is reasonably valued. If you would buy more shares at the current price with new money, then reinvesting your dividends through a DRIP makes sense. If you would not, consider taking the cash and deploying it where you see better value.

The “savings account” analogy Buffett uses for businesses applies perfectly here. A DRIP on a great business (one that pays an extraordinarily high interest rate that rises over time) is a powerful compounding tool. A DRIP on a mediocre business (one that pays an inadequate rate and requires constant capital) just compounds your problems.

The Bottom Line

DRIPs are among the simplest and most effective tools for dividend investors seeking to build long-term wealth. They automate the reinvestment process, harness the power of compounding, and remove the behavioral temptation to spend dividend income.

But they are not a replacement for sound analysis. The DRIP amplifies whatever the underlying business delivers. A DRIP on a high-quality, dividend-growing company accelerates your wealth. A DRIP on a struggling company with a deteriorating dividend accelerates your losses.

Here is the actionable takeaway: Use DRIPs selectively on your highest-conviction, highest-quality holdings, particularly in tax-advantaged accounts. Take dividends as cash from positions where you have less conviction or where the stock appears overvalued. And always remember that the quality of the business matters more than the mechanics of reinvestment.

That is going to wrap up our discussion for today.

As always, thank you for taking the time to read this post, and I hope you find something of value on your investing journey.

If I can further assist, please don’t hesitate to reach out.

Until next time, take care and be safe out there,

Dave

Muito bom.

Do this in your 20s-30s only.