S&P Global vs. Moody's: A Reverse DCF Teardown

High-quality companies often trade at prices that seem expensive, leaving investors on the sidelines waiting for a pullback that never comes.

But how do you know if a "high" price is actually fair value for a superior business?

This article will teach you how to use a reverse discounted cash flow (DCF) model to translate a stock price into a clear, tangible growth expectation, so you can decide for yourself if the market is being too optimistic or if the price is justified.

TL;DR

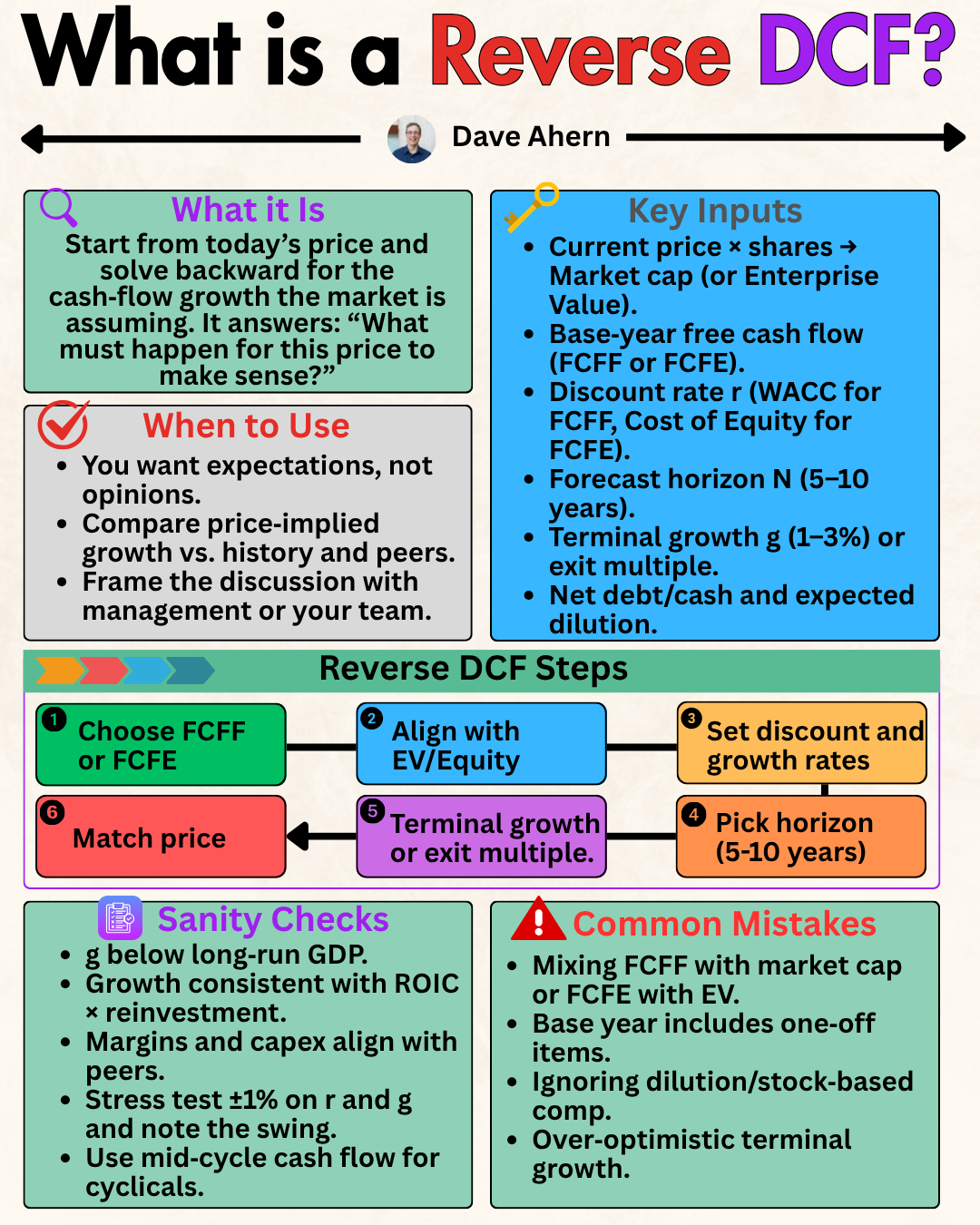

Valuation Flipped: A reverse DCF starts with the current stock price and solves for the future cash flow growth rate the market is implying. This is more objective than a traditional DCF, which starts with a growth assumption to arrive at a price.

From "What's it Worth?" to "What's Priced In?": The goal isn't to pinpoint an exact intrinsic value. It's to understand the expectations embedded in the price and then use your own research to determine if those expectations are plausible.

Key Inputs Matter: The model is most sensitive to three inputs: the starting free cash flow (FCF), the discount rate (WACC), and the terminal growth rate. Getting these roughly right is crucial.

The Quality Connection: Companies with high returns on invested capital (ROIC) and durable competitive advantages (moats) can justifiably sustain higher growth rates for longer, which the market often prices in.

SPGI vs. MCO: Both S&P Global and Moody's are classic quality compounders. A reverse DCF shows the market expects both to grow free cash flow at a low-double-digit pace for the next decade. The key question is whether their moats and reinvestment opportunities support that outlook.

Why It Matters

The biggest challenge in quality investing isn't identifying great businesses—it's valuing them without overpaying. A traditional DCF model is a powerful tool, but it has a critical flaw: its output (a single price target) is exquisitely sensitive to your long-term growth assumptions. If you assume 12% growth instead of 10%, the intrinsic value might swing by 20-30% or more. This precision is often false.

Investors go wrong by anchoring to their own biases, plugging in optimistic assumptions to make a valuation work. This creates the illusion of a margin of safety where none exists.

A reverse DCF short-circuits this bias. By starting with the price—the market's collective opinion—it forces you to ask a more practical question: "To justify today's price of $440, what does S&P Global need to deliver in cash flow growth over the next ten years?"

This reframes the problem from forecasting to reality-testing. You are no longer a forecaster; you are a critic, evaluating the plausibility of the market's embedded forecast.

Core Concepts: Deconstructing the Reverse DCF

A reverse DCF uses the same building blocks as a standard DCF, just in a different order. The core idea is that a company's value is the sum of all its future cash flows, discounted back to today.

ROIC vs. WACC and Value Creation

The engine of value is simple: a company must earn a Return on Invested Capital (ROIC) that is higher than its Weighted Average Cost of Capital (WACC). The wider the spread, the more value is created with every dollar reinvested back into the business. For quality companies like SPGI and MCO, which have asset-light models and strong pricing power, ROIC can be exceptionally high, often exceeding 30-40%. This is the hallmark of a powerful moat.

The Key Inputs

Current Free Cash Flow (FCF): This is your starting point. It's best to use a normalized figure, perhaps a 3-year average or the last twelve months' FCF, adjusted for any one-off items. FCF is a more honest measure of economic profit than GAAP Net Income because it accounts for cash required for capital expenditures.

Discount Rate (WACC): This rate reflects the riskiness of the company's cash flows. It's the blended cost of a company's equity and debt. For stable, blue-chip companies, a WACC of 8-9% is a common starting point.

Terminal Growth Rate: This is the rate you assume the company's FCF will grow at forever, after an initial high-growth period (e.g., 10 years). This should be a conservative number, typically in line with long-term GDP growth, say 2.5-3.0%. A rate higher than this implies the company will eventually become the entire economy, which is impossible.

With these three inputs and the current stock price, the model solves for the one missing variable: the implied FCF growth rate during the high-growth period.

Worked Example: S&P Global (SPGI) vs. Moody's (MCO)

S&P Global and Moody's are fantastic subjects for this analysis. They form a duopoly in the credit ratings industry, a business with immense regulatory moats, incredible pricing power, and very low capital intensity. These are the kinds of businesses that can generate massive amounts of free cash flow.

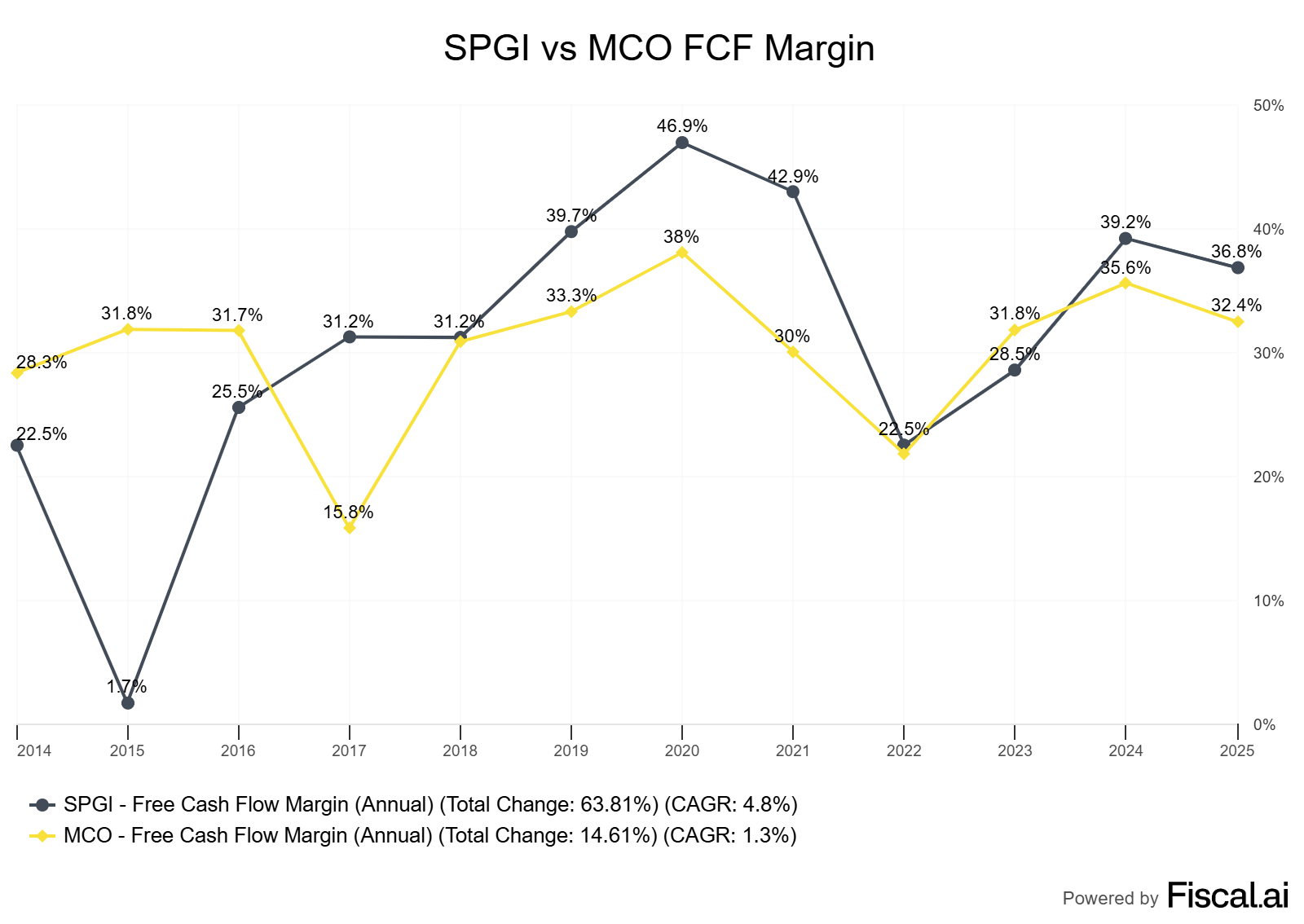

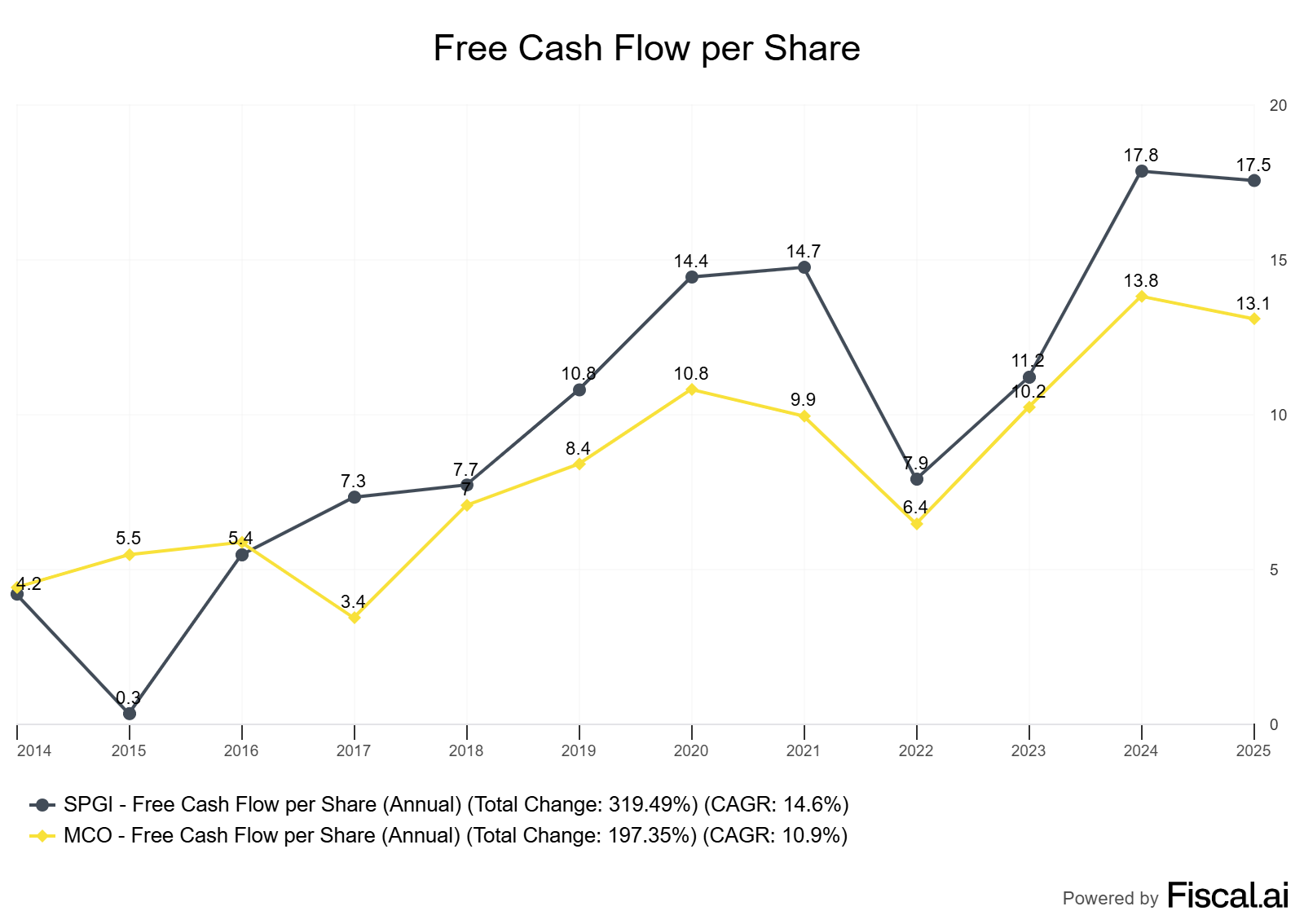

First, let's look at their historical performance. Both have been compounding machines.

Setting Up the Reverse DCF

Let's run the numbers. We'll use a simple two-stage model: a 10-year high-growth period followed by a terminal growth phase.

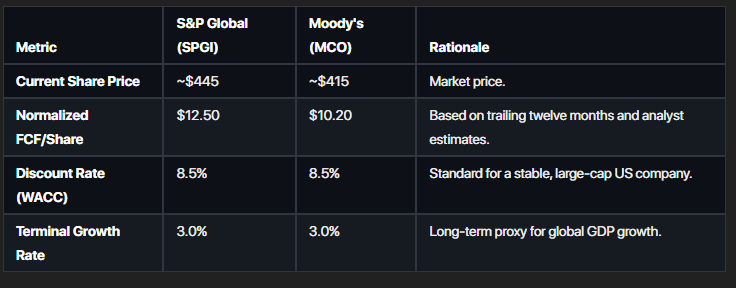

Assumptions (as of August 28, 2025):

Solving for Implied Growth

Plugging these numbers into a reverse DCF calculator, we solve for the annual FCF per share growth rate over the next 10 years that justifies today's price.

Results:

S&P Global (SPGI): The market price of ~$445 implies a 10-year FCF per share CAGR of ~11.5%.

Moody's (MCO): The market price of ~$415 implies a 10-year FCF per share CAGR of ~12.0%.

Is This Plausible?

The market is indicating that it expects both companies to increase their free cash flow per share by approximately 11-12% annually over the next decade. Now, we can use our fundamental research to critique this expectation.

Historical Context: Over the last decade, both companies have grown FCF per share at a similar, if not slightly higher, rate. So, the market is essentially pricing in a continuation of past success.

Analyst Estimates: The Wall Street consensus estimates for the next 3-5 years for both companies hover in the low double-digit range, aligning closely with our findings.

Business Drivers: Can they do it? Their ratings businesses are mature but benefit from GDP growth and new debt issuance. Their non-ratings segments (analytics, data, research) are growing faster and provide diversification. They have immense pricing power and are constantly buying back shares, which boosts the "per share" growth.

The conclusion is that the market's expectations, while not conservative, are not outlandish. They are pricing these companies as the high-quality compounders they have proven to be. An investment decision would hinge on your conviction that their moats will remain intact and they can continue to find reinvestment opportunities to sustain this level of growth for another ten years.

How to Build Your Own Reverse DCF

You don't need a complex spreadsheet. Here’s a simple process:

Gather Your Data:

Stock Price: From any financial data provider.

Shares Outstanding: From the company's latest 10-K or 10-Q filing.

Free Cash Flow: Calculate this from the cash flow statement:

Cash Flow from Operations - Capital Expenditures. Use the trailing twelve months (TTM) figure. You can find this on sites like Yahoo Finance or directly from filings.FCF per Share:

Free Cash Flow / Shares Outstanding.

Establish Your Assumptions:

WACC: For simplicity, start with a range. 8% for a very stable, low-risk business. 9-10% for a solid business with more cyclicality.

Terminal Growth Rate: Use a figure between 2.5% and 3.0%.

Use an Online Calculator: Search for a "Reverse DCF Calculator." There are many free web-based tools.

Input and Solve: Enter the stock price, your FCF per share, WACC, and terminal growth rate. The tool will solve for the implied growth rate.

Analyze the Result: This is the most important step. Compare the implied growth rate to the company's historical growth, management's guidance, and your own qualitative assessment of its moat and reinvestment runway. Is the expectation reasonable, heroic, or overly pessimistic?

Common Pitfalls and False Positives

Using Net Income Instead of FCF: Net income includes non-cash charges and can be distorted by accounting choices. FCF is a purer measure of cash profit.

Ignoring Stock-Based Compensation (SBC): SBC is a real expense. Some companies report "Adjusted FCF" that adds it back. Be sure to treat it as a cash expense or account for the resulting dilution in your share count forecast.

One-Time Items: A single year's FCF can be skewed by large working capital swings or one-off cash outlays. Using a multi-year average can provide a more normalized starting point.

Setting the Terminal Growth Rate Too High: This is the most common way to inflate any DCF model. Keep it anchored to long-run GDP growth.

Checklist for Your Valuation Process

Have I used a normalized, clean starting Free Cash Flow per share?

Have I accounted for stock-based compensation?

Is my discount rate (WACC) reasonable for the company's risk profile?

Is my terminal growth rate at or below the long-term rate of global economic growth?

Have I compared the implied growth rate to the company's historical results?

Have I compared the implied growth rate to the size of its addressable market?

Does the company's moat and competitive advantage support this implied growth rate for ten years?

Mini-FAQ

How do I estimate WACC without a finance degree?

For stable, large-cap companies, using a range of 8-9% is a reasonable starting point. You can also find consensus estimates on some financial data platforms. The key is to test a range to see how sensitive your output is to this assumption.What's a "good" implied growth rate?

There is no "good" or "bad" number. It's all about context. An implied growth rate of 5% for a utility company might be wildly optimistic, while a 15% rate for a founder-led SaaS company might be conservative. The goal is to judge its plausibility for the specific business.Can I use this for unprofitable tech companies?

No. A DCF model requires positive and predictable free cash flow. It is not the right tool for early-stage or unprofitable businesses.How far out should I project the high-growth period?

Ten years is a standard convention. Using a period much longer than that (e.g., 20 years) implies an unrealistic level of certainty about the distant future.What if the implied growth is negative?

This suggests the market expects the company's cash flows to shrink over time. This could be an opportunity if you believe the market is overly pessimistic, or it could be a warning sign that the business is in structural decline.

Glossary

DCF (Discounted Cash Flow): A valuation method used to estimate the value of an investment based on its expected future cash flows.

FCF (Free Cash Flow): The cash a company generates after accounting for cash outflows to support operations and maintain its capital assets.

WACC (Weighted Average Cost of Capital): The average rate of return a company is expected to pay to all its security holders (debt and equity).

ROIC (Return on Invested Capital): A ratio used to assess a company's efficiency at allocating the capital under its control to profitable investments.

Terminal Value: The estimated value of a business beyond the explicit forecast period.

CAGR (Compound Annual Growth Rate): The mean annual growth rate of an investment over a specified period of time longer than one year.

Moat: A durable competitive advantage that allows a company to protect its market share and profitability from competitors.

Further Reading

Expectations Investing: Reading Stock Prices for Better Returns by Michael Mauboussin and Alfred Rappaport. (Book)

Musings on Markets Blog by Aswath Damodaran. (Website, ongoing)

Valuation: Measuring and Managing the Value of Companies by McKinsey & Company. (Book)

References

S&P Global Inc. (2024). Form 10-K, Fiscal Year-Ended December 31, 2023. Retrieved August 28, 2025.

Moody's Corporation (2024). Form 10-K, Fiscal Year-Ended December 31, 2023. Retrieved August 28, 2025.

Financial data sourced from public providers as of August 28, 2025.

Educational content, not investment advice.