S& Global (SPGI): Durable Earnings or Not?

S&P Global’s earnings durability is underpinned by a highly recurring, asset-light information-services model with diversified monetization across credit ratings, indices, data/analytics, and commodity insights.

Structural moats include network effects (indices AUM-linked fees), brand and regulatory accreditation (NRSRO ratings), switching costs (embedded workflows, historical time series), and scale/data advantages. The largest swing factors are (1) ratings issuance cyclicality, (2) potential regulatory actions affecting take rates or methodology, and (3) competitive dynamics in data/analytics and index licensing.

Durability Score: 88/100.

It could rise with continued mix-shift to subscription/recurring revenues, broadened index AUM penetration, and stable regulatory posture; it could fall with prolonged issuance droughts or material regulatory/take-rate changes that compress margins.

1) Business model and end-market mapping

Revenue drivers:

Price: subscription list pricing, contractual escalators; licensing rates on AUM-linked indices; transaction fees on ratings.

Volume: bond/loan issuance volumes, index AUM and ETF creations, data seats/users, consumption-based data feeds, commodity assessments/trading services.

Mix: shift toward data feeds/enterprise solutions; higher-yield index licensing; non-transaction ratings and surveillance.

Value chain and risk bearing:

Credit risk is borne by issuers/investors; SPGI bears primarily reputational and regulatory risk (especially in Ratings).

No inventory/commodity risk; Commodity Insights monetizes price assessments and analytics.

Regulatory exposure meaningful in Ratings (NRSRO, ESMA, FCA, etc.).

Secular vs cyclical exposure:

Secular: growth in passive investing (indices), data proliferation/automation, private markets data, climate/ESG analytics, energy transition insights.

Cyclical: credit issuance cycles; macro risk appetite; market volumes affecting index-linked AUM.

Cash flow model:

Asset-light; low maintenance capex and high inherent operating leverage.

High gross margins; structural scalability as datasets, methodologies, and platforms are reused across clients.

Source: segment and business model descriptions in 10-Ks (2024 10-K).

2) Moats and competitive dynamics

Moat sources:

Network effects: S&P DJI indices embedded in trillions of AUM; benchmark standard status supports durable licensing.

Switching costs: deep integration of datasets (Capital IQ Pro, Ratings, Platts) into client models, workflows, back-tests.

Brand and regulatory accreditation: S&P Global Ratings is a leading NRSRO with entrenched market acceptance.

Scale/data/IP: proprietary time series, methodologies, price assessments; breadth across asset classes and sectors.

Distribution: global enterprise relationships; multi-segment cross-sell.

Competitive set and disruption vectors:

Ratings: Moody’s, Fitch; potential platform disintermediation limited by regulation and investor requirements.

Indices: MSCI, FTSE Russell; threats include custom/direct indexing, fee pressure; but category remains oligopolistic.

Market Intelligence/Data: Bloomberg, FactSet, LSEG/Refinitiv, Morningstar; open-source/AI agents could pressure “commodity data,” but proprietary content + workflow tools mitigate.

Commodity Insights: Argus, ICIS; methodology trust and adoption create barriers.

Concentration/embeddedness:

10-Ks typically disclose no single customer >10% of revenue; long-term contracts with auto-renew mechanics for many subscriptions; multiyear index/ETF arrangements.

Source: risk factors, business, and competition sections in 10-Ks (2024 10-K).

3) Financial signals of durability

Durable earnings narrative (based on the above)

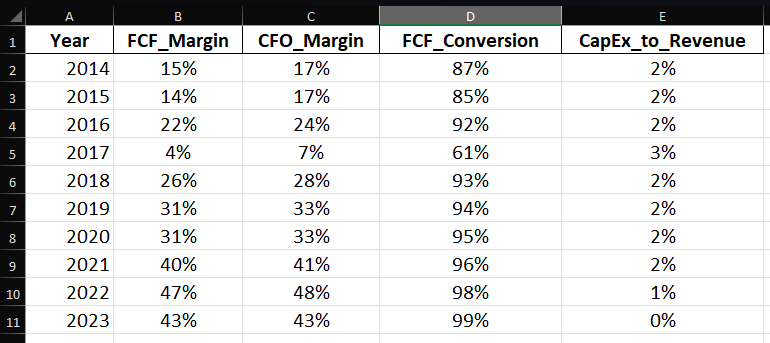

Recurring, high-margin model: Average CFO margin ~29% and FCF margin ~27% over a decade indicate strong cash generation relative to sales, consistent with subscription/data/rating franchises. Low CapEx intensity (~1.8% of revenue) supports robust cash conversion into FCF without heavy reinvestment needs.

Capex-light durability: With limited PP&E investment required, growth has been funded primarily through operating cash. This structure typically scales well and cushions cash flows in down-cycles.

FCF resilience and improvement: Despite a pronounced dip in 2017 (FCF margin ~4%), the company rebounded quickly, with FCF margins in the 25–47% range from 2018 onward. The step-up through 2021–2023, alongside revenue CAGR of ~7.7%, underscores durable cash profitability.

Strong FCF conversion: Average FCF/CFO conversion of ~90% (using only CapEx) highlights minimal leakage from operating cash flows to sustain the asset base, amplifying cash available for debt service, buybacks, dividends, or selective M&A.

Scale benefits and mix shift: From 2014 to 2023, revenue roughly doubled (4.27B → 8.30B), while FCF increased more than 5× (0.63B → 3.56B), implying expanding operating leverage and mix toward higher-value analytics/benchmarks. The 2022 integration period aligns with the visible step-up in both revenue and cash generation afterward.

Volatility note: 2017 is the outlier year in this series. Excluding that year, both margins and FCF growth display a steadier trajectory, reinforcing the “durable earnings” characterization over the broader period.

Key formulas:

Sustainable growth: g=Reinvestment Rate×ROIC

Accruals ratio (simplified): Accruals=Average Total Assets(ΔCurrent Assets−ΔCash)−(ΔCurrent Liabilities−ΔDebt)−Depreciation

4) Stress tests and “kill switches”

Prior shock performance:

2020 issuance volatility; 2022–2023 Ratings downturn; resilience from non-transaction and index/data segments.

Source: MD&A discussions (2022–2024 10-Ks).

Scenario tests (illustrative structure):

Scenario A: Credit issuance shock −30% for 4 quarters → Ratings revenue/margin down; partial offset from subscriptions and indices AUM if markets recover.

Scenario B: Regulatory take-rate cut in indices or pricing oversight in Ratings (e.g., −20–50 bps on specific fee lines) → multiple compression risk; mitigants include product mix and volume growth.

Scenario C: Share loss to competing data/desktop in EMEA financials (e.g., −5% data seats) → modest revenue impact; counter by bundling and workflow stickiness.

Single points of failure and mitigants:

Ratings methodology credibility/regulatory status → governance, compliance, transparency.

Index AUM concentration risk → product breadth, custom indices, derivatives/ETP ecosystem depth.

5) Reinvestment runway

New products/adjacencies:

Private markets datasets/analytics, climate/ESG (Sustainable1), AI-enabled research and data engineering, index innovation (thematics, factors), commodity transition analytics.

Geographic white space:

EM debt/ETFs penetration; APAC data and index adoption; local-language workflow tools.

Returns on new investments:

Historically strong IRR for IP-rich expansions; watch post-merger synergy capture and integration ROI (IHS Markit merger closed 2022).

Source: strategy disclosures and FY releases (2022 results note Investor Day model).

Capital allocation:

Dividends and buybacks (ASRs in 2022–2024), selective M&A and divestitures to optimize portfolio (e.g., regulatory-related asset sales).

Source: capital returns and repurchase program details in 10-Ks (2024 10-K).

6) Linking durability to valuation

Higher ROIC + reinvestment → higher and longer growth g.

Predictable cash flows and recurring mix → lower required return k.

Stable-growth intuition: EP=(k−g)(1−b),b=retention rate

What can expand/contract the multiple:

Expanders: issuance up-cycle, recurring mix gains, AI/data monetization, benign regulation, lower real rates.

Contractors: regulation/take-rate pressure, prolonged issuance drought, fee deflation in indices/data, higher rates.

Optional narrative (DCF/EVA):

Durability supports long advantage period; terminal fade modest if moats persist. Use 10-K cash flows and Yahoo Finance WACC inputs to frame scenarios (do not fabricate).

7) Return decomposition (5–10 years)

TSR framework: TSR≈FCF/share growth+Dividend Yield+ΔMultiple

Base case (qualitative assumptions):

FCF/share growth: MSD-to-HSD from mix-shift to recurring + issuance normalization; modest margin expansion; ongoing buybacks reduce share count.

Dividend yield: low current yield with steady annual raises; payout remains conservative versus FCF.

Multiple: stable to modest compression if rates rise; expansion if durability narrative strengthens.

Bear case:

Ratings trough extended; regulatory friction; limited index fee growth → lower FCF growth and some multiple compression.

Bull case:

Strong multi-year issuance rebound; index AUM compounding; AI-enabled operating leverage → higher FCF/share growth; multiple holds or expands.

Sensitivity (qualitative):

±1–2 P/E turns meaningfully impacts TSR given elevated starting multiple; ±200 bps in g has outsized effect via both earnings path and justified multiple.

8) Practical checklist (score each 1–10; weight)

Network effects and switching costs (15): 9

Pricing power (15): 9

Cyclicality and shock resilience (10): 7

Customer/supplier concentration (10): 9

Cash conversion and capital intensity (10): 9

ROIC level and fade risk (15): 9

Regulation risk (10): 6

Disruption risk (10): 7

Reinvestment runway (10): 8

Accounting quality (5): 8

Durability Score (0–100) = 88

Biggest drivers: network effects and brand/regulatory status in Ratings and Indices; asset-light cash conversion.

What could move it ±10: Regulatory/take-rate actions (down), or accelerated recurring mix/AI-enabled productivity gains (up).

9) What to monitor quarterly

Core issuance/transaction trends vs market volumes; monthly Billed Issuance (as disclosed).

Index AUM, ETF flows, licensing yields; new index launches.

Subscription growth in Market Intelligence and Commodity Insights; attach and seat metrics.

Margin trajectory (adjusted vs GAAP); cost discipline and synergy capture.

FCF conversion; buybacks; share count; leverage.

Regulatory developments (SEC/ESMA/FCA) and any notable cases.

Key partnerships, renewals, and ecosystem integrations (ETF sponsors, exchanges).

Guidance changes and variance analysis.

Sources: quarterly earnings materials (see Quarterly Earnings hub) and 10-Qs.

10) Risks and catalysts

Risks:

Issuance cyclicality (medium likelihood/medium–high impact).

Regulatory/take-rate changes (low–medium likelihood/high impact).

Fee pressure in indices/data or share loss to competitors (medium/medium).

Methodology/operational lapses (low/high due to reputational leverage).

Catalysts:

Issuance rebound cycles; new index adoptions; major data contract wins.

AI features that increase product differentiation and pricing.

Portfolio optimization (value-accretive M&A/divestitures).

Regulatory clarity or positive rulings.

11) Sources

Primary sources:

FY2024 results release: Press Release

Annual report: Annual Report 2024 | S&P Global

Disclosures: Educational content. Not investment advice.

The only one should invest is by learning price volume action and the ability to take losses.