Microsoft Yields 0.81%. The 2015 Buyer Is Collecting 8%. Here's How.

It's called yield on cost, and it explains why a tiny starting yield can still be a great income holding.

After last week’s Microsoft deep dive, a reader sent me a fair question.

“If the dividend only yields 0.81%, why would any income investor bother owning it?”

That is exactly the right question to ask. And the answer is a number most beginners never bother to calculate.

It is called yield on cost. Once it clicks, a tiny starting yield stops being a dealbreaker.

In today’s post, we will discuss:

What yield on cost actually measures

Why your current yield and your yield on cost drift apart over time

Microsoft as our guinea pig

How to use the number without fooling yourself

Okay, let’s dive in.

The two yields most people blur together

There are two different yields hiding behind the same word, and beginners mix them up all the time.

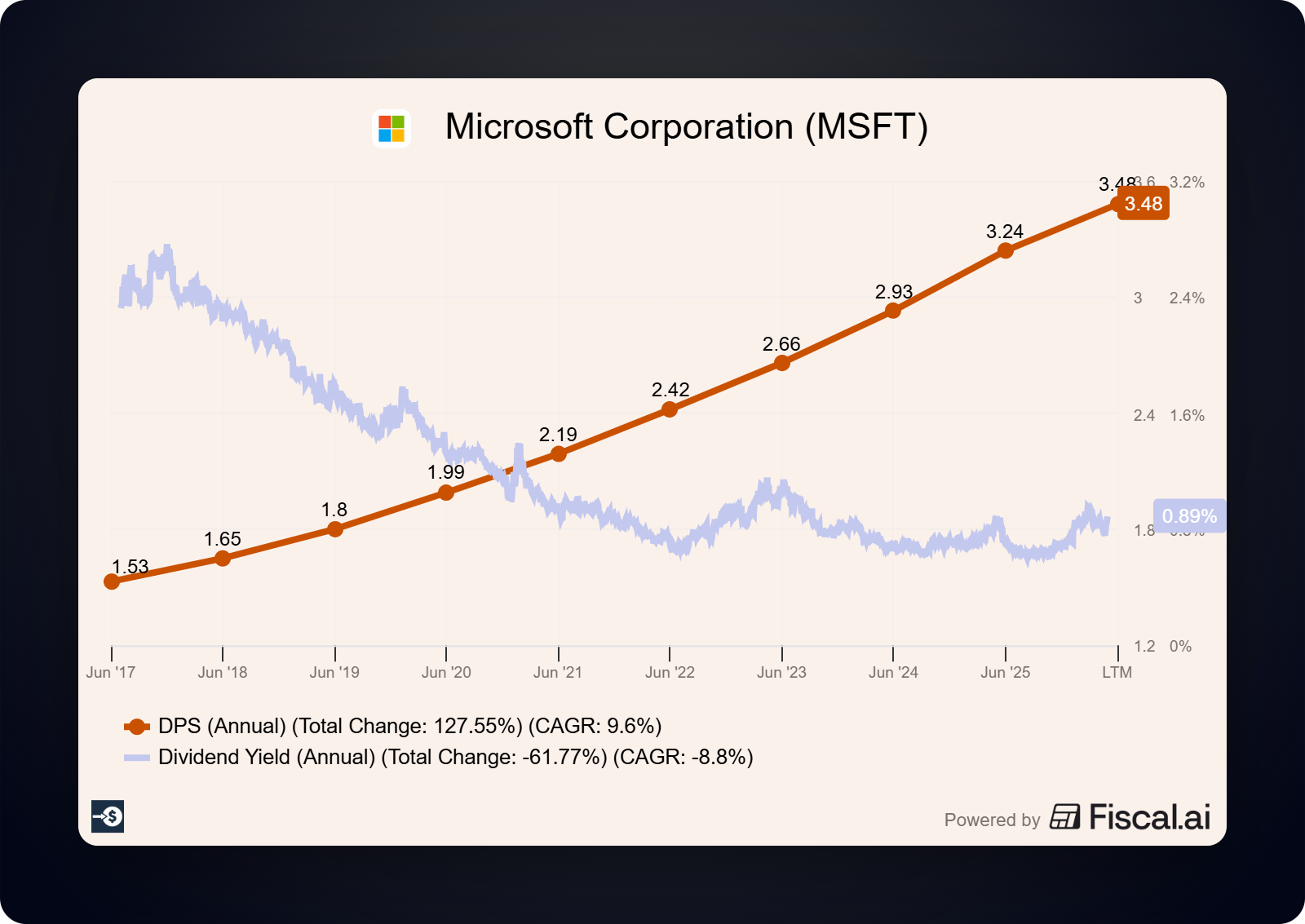

Current yield is the annual dividend divided by today’s share price. It is the number on every stock screener. For Microsoft at roughly $450 a share, paying $3.64 a year, that is 0.81%.

Yield on cost is the annual dividend divided by what you paid, your own cost basis. It is personal to you, and it does not show up on any screen.

Here is the key idea. The day you buy, those two numbers are identical. From that day forward, they go their separate ways.

Your cost basis is frozen at the price you paid. The dividend, in a healthy dividend-growth company, keeps climbing. So your yield on cost rises every single year you hold, even though the screener still shows the same small current yield to everyone looking today.

Next week I count the other half of Microsoft's payout, the buybacks that never show up as a yield. If you want it free in your inbox, subscribe here.

Microsoft as our guinea pig

Let’s look at Microsoft to see how far those two numbers can drift.

Microsoft pays $3.64 a year right now. The dividend has grown around 10% a year for two decades, and the company has raised it for more than twenty years straight.

A dividend growing 10% a year doubles in a little over seven years. That is the engine.

Now imagine you bought Microsoft back in 2015, around $45 a share. (Treat that price as a rough illustration, not your exact basis.) Watch what today’s dividend does against that old purchase price:

What you paid: ~$45

Current annual dividend: $3.64

Your yield on cost: $3.64 / $45 = about 8.1%

The screener’s current yield today: 0.81%

Same company. Same dividend. One number is 0.81% and the other is north of 8%.

The 2015 buyer is collecting close to 8% a year on the money they originally put in, while a buyer today starts at 0.81%. Someone who bought even earlier, back around $33 in 2013, has already crossed into double-digit yield on cost.

The yield looked trivial in year one. It did not stay trivial.

How to use it without fooling yourself

Yield on cost is a useful lens, and it is also easy to abuse. Here is how I think about keeping it honest.

Use current yield to decide what to buy today. When you are comparing two stocks you might purchase right now, you both start the clock at the current yield, so that is the fair comparison.

Use yield on cost to decide what to keep. A holding with a modest current yield but a fast-growing payout can quietly become one of the best income streams in your portfolio, which is the case for holding through a low headline yield.

The growth rate matters more than the starting yield. A 0.81% yield growing 10% a year passes a 3% yield growing 2% a year in about twelve years, and then pulls away for good.

Where investors get this wrong

Yield on cost rewards patience, and it also flatters you in ways that can cloud your judgment.

The biggest trap is treating it as a return. It is not. Yield on cost ignores the share price entirely, so it tells you nothing about whether the stock is cheap, fair, or expensive today.

A second trap is letting a high yield on cost talk you into holding a broken business. The number keeps looking great right up until the dividend gets cut, because it is anchored to a price from years ago. If the business quality slips, your cost basis will not save you.

The last trap is comparison. Your 8% yield on cost is not better than someone else’s 4% current yield, because they are two different measurements. Comparing them is like comparing your mortgage rate from 2015 to today’s listing price.

Yield on cost only works as a reason to hold when the dividend keeps growing and the underlying business stays healthy, which is why the safety work in last week’s deep dive comes first.

The takeaway

A small current yield attached to a fast-growing, well-covered dividend can turn into a large yield on cost given enough time, which is the whole reason a quality compounder like Microsoft belongs in a dividend-growth sleeve.

The dividend, though, is only half the cash Microsoft hands back to shareholders. The other half never shows up as a yield at all. Next week I will show you how to count Microsoft’s buybacks, why they quietly shrink your share count in your favor, and why they are the first thing to get cut when capital spending explodes.

If you want that buyback piece free in your inbox next week, the newsletter’s here.

That will wrap up today’s discussion.

If I can be of any further help, please don’t hesitate to reach out.

Until next time, stay safe out there,

Take care,

Dave

P.S. Here's the part worth remembering: the day you buy, the yield is the worst it will ever look. From there it only grows.