Microsoft Will Spend $190 Billion in 2026. Is Its 22-Year Dividend Streak Still Safe?

A 94 safety score reads the past. The $190 billion in capex reads the future. Here's what it does to free cash flow.

Dividend School monthly deep dive.

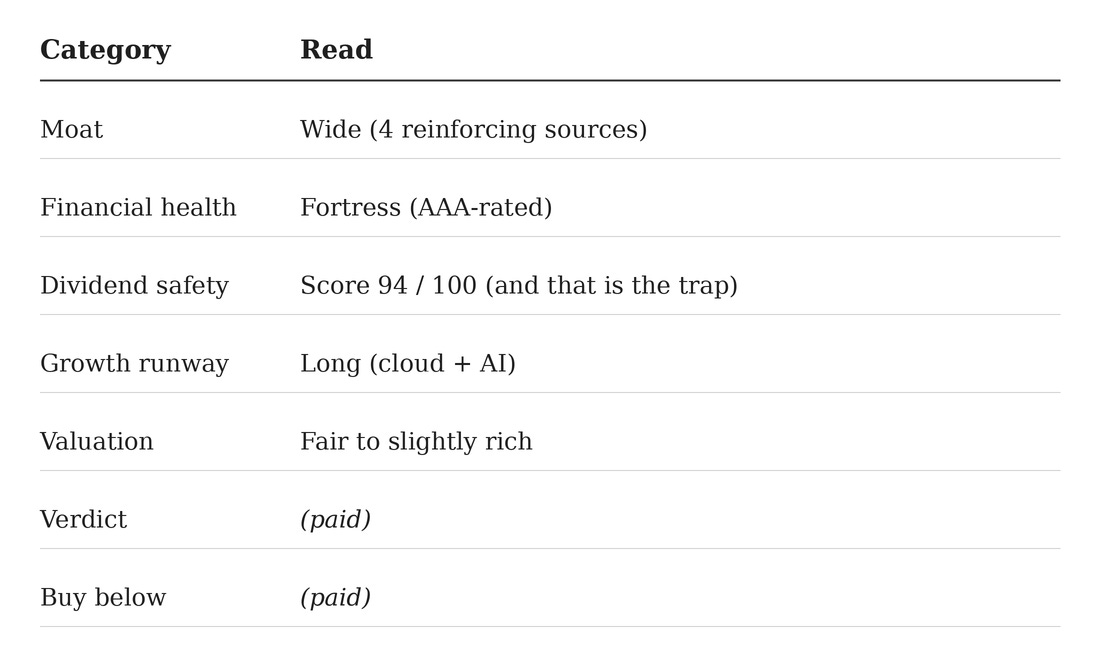

Scorecard

Microsoft is the rare company that scores a 94 on dividend safety while quietly rewriting the cash-return math on which the score is built. This month, we look at why both things are true at once.

1. Intro

Run Microsoft through a dividend safety screen today and it comes back a 94 out of 100. Near perfect.

The payout eats about a quarter of earnings. Free cash flow covers it almost three times over. The balance sheet is one of two in America still rated AAA. The company has raised the dividend every year for more than two decades.

Then look at one number the screen never sees: Microsoft plans to spend roughly $190 billion on capital expenditures in calendar 2026.

That is about seven times the entire dividend. And it is the reason a 94 might be the most misleading number in this whole report.

A safety score is a photograph. It captures a company as it was over the last several years of reported numbers. Microsoft just walked out of the frame. The company that earned that 94 returned more cash to shareholders than it spent building its own future. The company reporting next year will spend more building its future than almost any business in history. Same dividend. Same ticker. Very different math.

This deep dive answers one question. Is Microsoft’s dividend as safe as the score says, or is the score reading a chapter the company already finished writing?

2. The bet

Microsoft is a toll booth on the digital economy that happens to pay a tiny, fast-growing dividend.

For an income investor, the appeal was never the yield. It was the combination of a payout that compounds near 10% a year and a business durable enough to keep doing it. A 0.92% yield that grows 10% a year and never gets cut is worth more over twenty years than a 5% yield that stalls. That is the trade Microsoft offers.

The bet is that the AI buildout strengthens that toll booth rather than starving the dividend that rides on top of it. Get that judgment right and you own one of the great compounding machines of the era. Get it wrong and you paid a fortress price for a company that just turned far more capital-hungry than its reputation suggests.

3. What the company does

Microsoft sells the software and computing that businesses and people run their day on.

Three things drive it. There is the productivity stack most offices live in: Windows, Office (now Microsoft 365), Teams, and LinkedIn. There is Azure, the cloud platform companies rent instead of running their own server rooms. And there is everything personal: Windows licenses, Xbox, search, and devices.

Think of Azure as renting apartments instead of building your own house.

A company that would once have bought servers, hired staff, and cooled a room full of hardware now pays Microsoft a monthly bill and lets Microsoft own the building. The tenant gets flexibility and no maintenance headaches. The landlord gets a check every month, forever, and a tenant who finds moving out more trouble than it is worth.

That last part is the whole game. Once a business runs its email, its files, its identity logins, and its custom software on Microsoft, switching to a competitor means retraining every employee and rebuilding systems that already work.

Most companies decide the hassle is not worth it. They stay, and they keep paying.

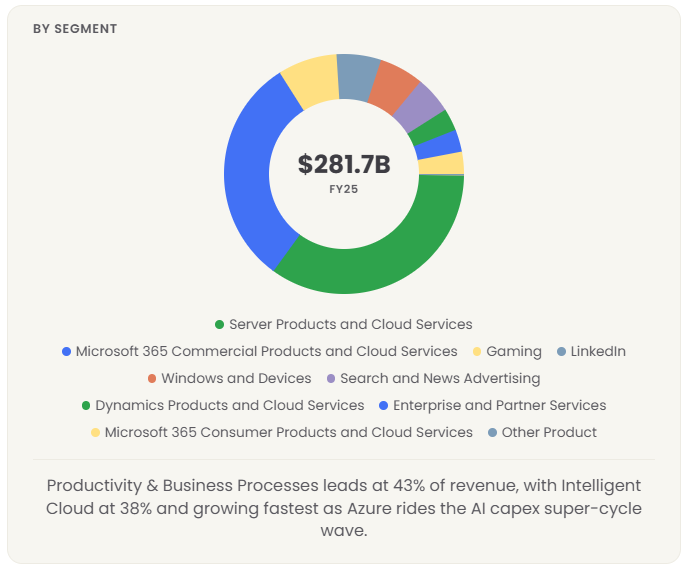

Pull Microsoft apart and three engines show up, each one bigger than most companies on the market. In fiscal 2025, Productivity and Business Processes (Microsoft 365, Dynamics, LinkedIn) brought in about $121 billion. Intelligent Cloud (Azure, server products, GitHub) brought in about $106 billion. More Personal Computing (Windows, Surface, Xbox, search) added close to $55 billion. Three businesses, each generating tens of billions a year, sitting under one roof.

Who actually pays for all of this? Close to everyone. Microsoft’s customer base is one of the broadest in technology: nearly the entire Fortune 500, several hundred thousand mid-market firms, most major governments, the bulk of small businesses running Windows, and about 89 million consumer Microsoft 365 subscribers.

That consumer number grew from 51.9 million in 2021, a quiet mid-teens compounder running underneath the louder enterprise story.

The stickiness shows up in one figure better than any other. Microsoft’s commercial backlog, the revenue it has signed under contract but not yet delivered, reached $368 billion at the end of fiscal 2025 and $627 billion by the third quarter of fiscal 2026, up 99% year over year — a doubling in a single year on long-dated AI and cloud commitments. Think of that backlog as a freight rail timetable.

The trains are already scheduled and the tickets already sold, which is how a software company can spend like a utility and still sleep at night.

The relationships deepen rather than fade.

Once a company puts its employee logins on Microsoft’s identity system, then its email, then its files, then a Copilot assistant on top, leaving becomes close to unthinkable. Customers with 50,000 or more Copilot seats quadrupled over the past year. Accenture alone runs nearly 740,000 Copilot seats. This is not a customer base that turns quickly, and that is the bedrock under the dividend.

4. How they make money

We just met the three engines. The more useful question for an income investor is how the cash actually arrives, because the billing model is what makes Microsoft’s cash flow so steady and the dividend so easy to fund in a normal year.

Two motions do most of the work. Microsoft 365 bills per seat, a fixed charge every month or year for each employee, which throws off smooth, predictable revenue that barely flinches with the economy. Azure bills on consumption, charging for compute and storage as customers use it, with multi-year enterprise commitments sitting behind that usage. Azure grew 40% last quarter and is the fastest-moving piece of the mix. LinkedIn and Dynamics layer their own recurring subscriptions on top.

The economics are the dream version of software. A customer signs up, and the cost of serving them barely rises as they stay, so gross margins on cloud and software run high and improve with scale. That is why a few points of revenue growth drop through to a lot more profit.

The headline results, from Microsoft’s own filings:

Fiscal 2025 revenue: $281.7 billion, up 14.9%

Fiscal 2025 net income: $101.8 billion, up 15.5%

Fiscal 2025 diluted EPS: $13.64, up 15.6%

Microsoft Cloud revenue: $168 billion, up 23%

Most recent quarter (Q3 FY2026): revenue $82.9 billion, EPS $4.27 (up 21% year over year), AI now at a ~$37 billion annualized run rate, up 123%

A high-quality, growing, cash-rich business. Now the part you pay for: whether that quality is enough to protect the dividend through the most expensive building project in corporate history, and what the real risk is if it is not.

The free magnet ends here. Everything below is the paid build: the moat, the financials, the full dividend safety read that the 94 hides, the forward cash-flow scenarios, a bull/base/bear valuation, and the buy-below price.

Want to know whether a 94 safety score is hiding the real risk? Want the forward free-cash-flow scenarios? Want the buy-below price I would actually pay? Everything below is for paid subscribers.

Included is a downloadable PDF of the full deep dive to keep.