Microsoft: Reinvention and the Financial Evidence of Transformation

When Satya Nadella took over as Microsoft CEO in February 2014, the company faced a critical question: Could a mature tech giant built on Windows and Office licensing truly reinvent itself for the cloud era? Ten years later, the numbers tell a story of one of the most successful business transformations in tech history.

This isn’t just about a stock price that climbed 10x. The real story is in how Microsoft fundamentally changed what business it’s in, and how those changes show up in the financial statements. As investors evaluating corporate reinventions, we need to ask: What does a successful transformation actually look like in the numbers?

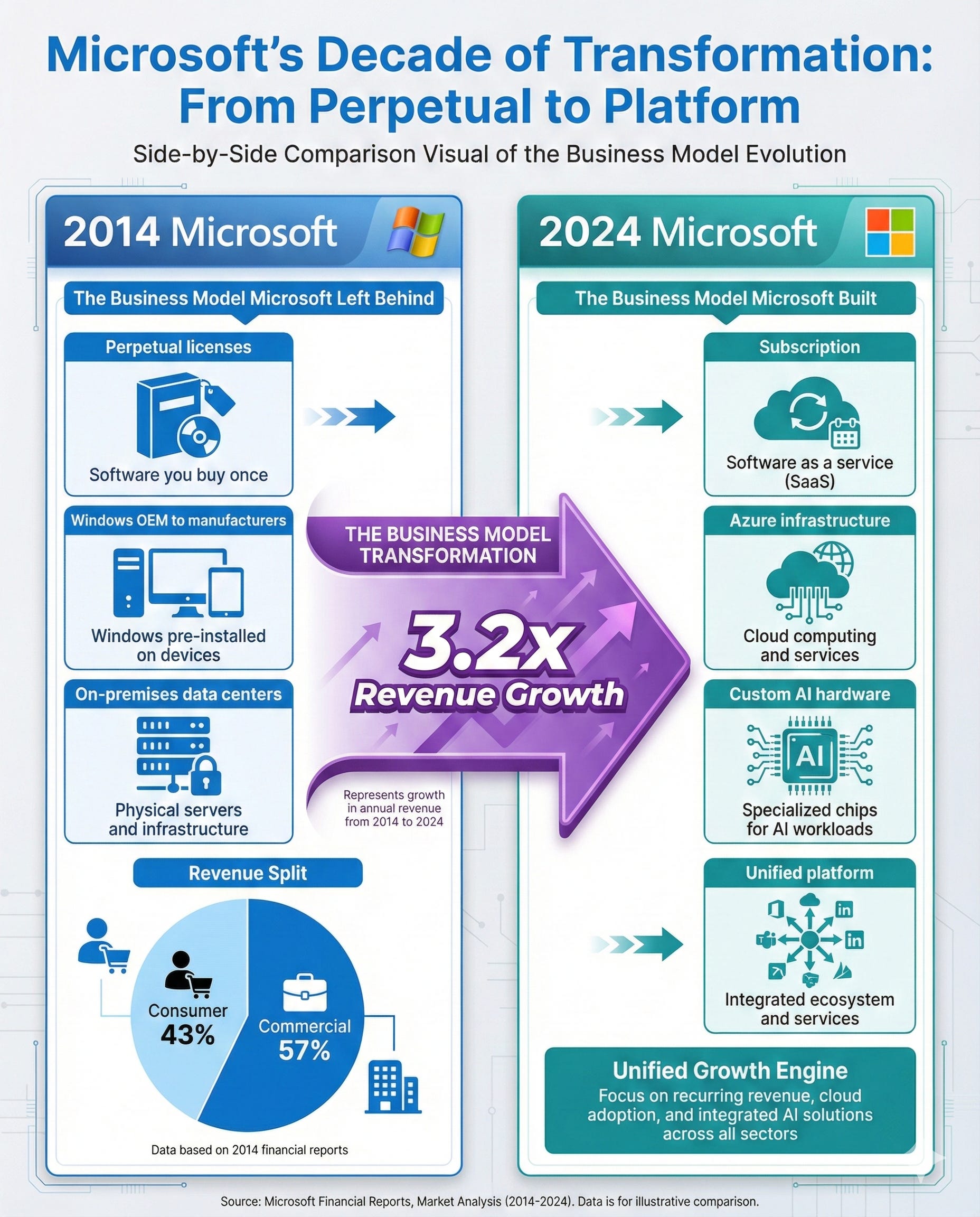

The Business Model Microsoft Left Behind

To understand Microsoft’s transformation, start with what the company looked like in fiscal 2014 (ending June 30, 2014). According to Microsoft’s 10-K filed that year, the company was organized into five segments following a restructuring: Devices and Consumer Licensing, Computing and Gaming Hardware, Phone Hardware, D&C Other, Commercial Licensing, and Commercial Other.

Total revenue for FY2014 was $86.8 billion. The revenue breakdown revealed Microsoft’s legacy business model:

Devices & Consumer ($37.7B total, 43% of revenue):

D&C Licensing (Windows, Office Consumer): $18.8B

Computing and Gaming Hardware (Xbox, Surface): $9.6B

Phone Hardware (Nokia acquisition): $2.0B

D&C Other (Bing, Xbox Live, search ads): $7.3B

Commercial ($49.6B, 57% of revenue):

Commercial Licensing (Windows Server, SQL Server, Office Commercial): $42.0B

Commercial Other (Enterprise Services, early cloud): $7.5B

The company’s mission statement in 2014 was “to enable people and organizations throughout the world to do more and achieve more.” It positioned itself as a “productivity and platform company for the mobile-first and cloud-first world.” The language was aspirational, acknowledging a future direction without having fully arrived there yet.

The 2014 10-K reveals that the company is still deeply anchored in its legacy businesses. Windows OEM licensing (selling operating systems to PC manufacturers) remained central to the business model. The company had just acquired Nokia’s phone business, a $7.2 billion bet on competing directly with Apple and Google in smartphones. Xbox consoles and Surface tablets were relatively new hardware experiments.

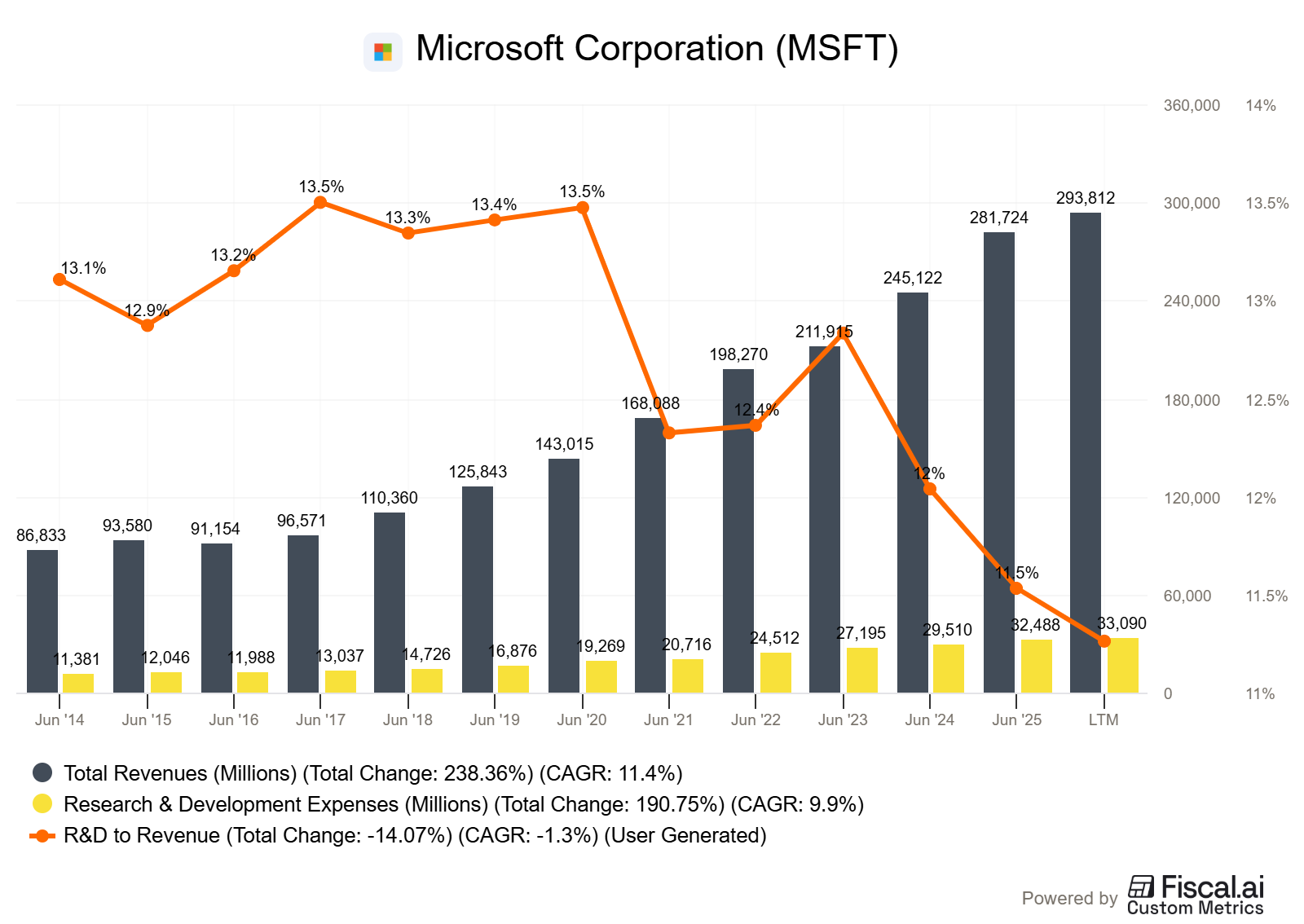

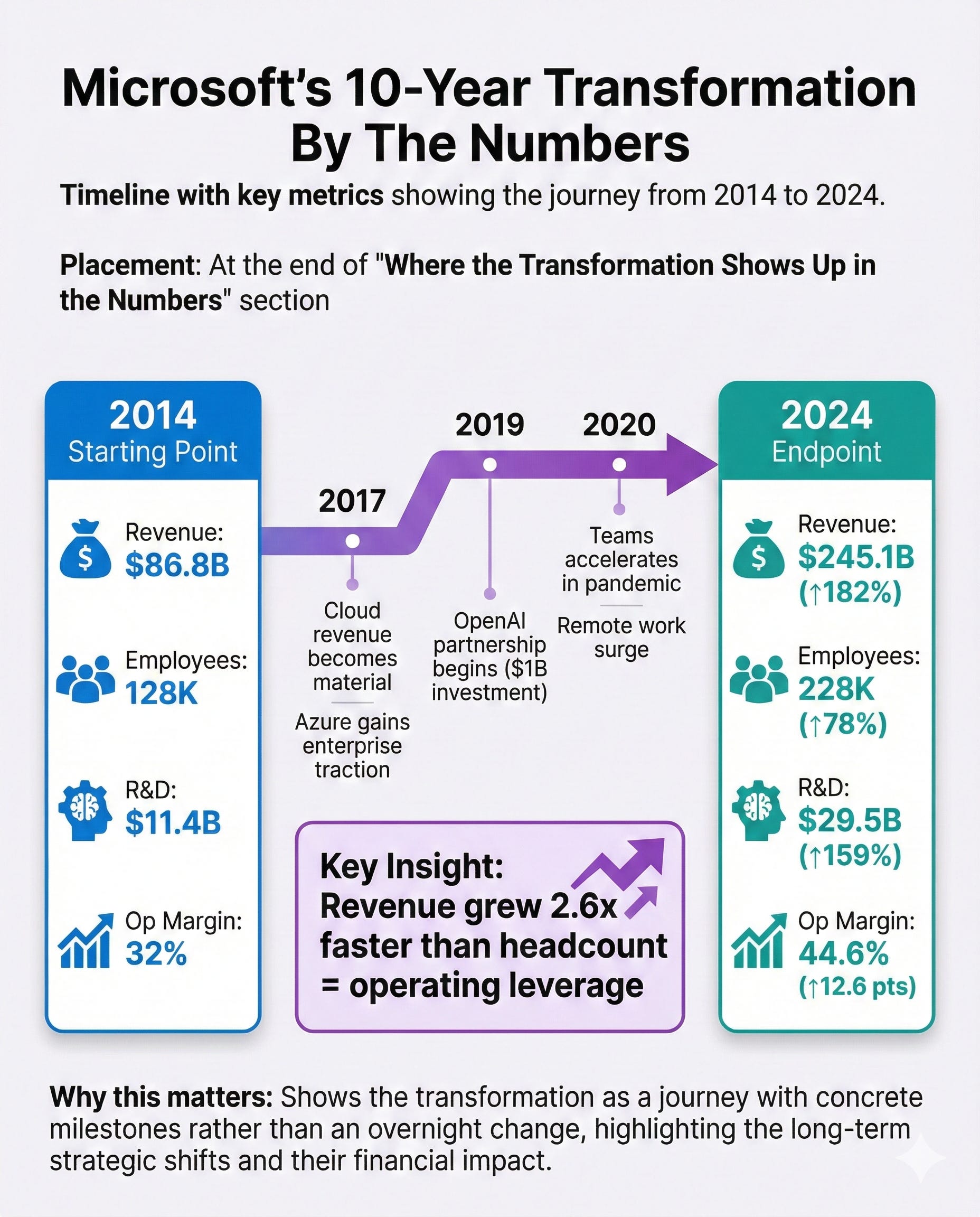

Cloud services existed but weren’t yet the dominant force. Azure was mentioned alongside other services like Bing, Office 365, and OneDrive, but the company didn’t break out “Microsoft Cloud” as a separate reportable figure. Research and development spending was $11.4 billion (13% of revenue), and the company employed 128,000 people.

The Business Model Microsoft Built

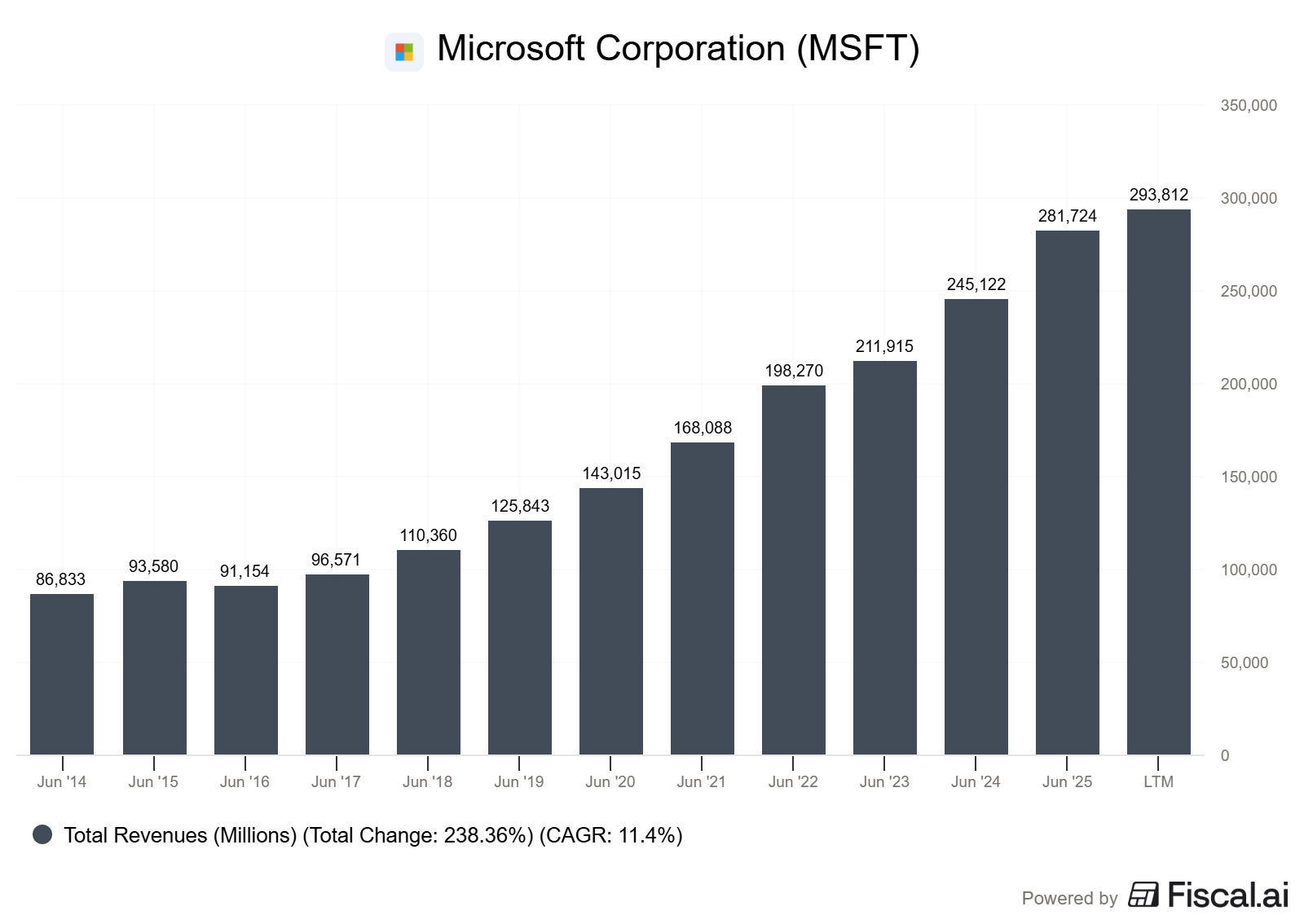

Fast forward to fiscal 2024 (ending June 30, 2024). Total revenue had grown to $245.1 billion, a 182% increase. By fiscal 2025, revenue reached $281.7 billion, representing a 224% increase from 2014 or 3.2x growth over the decade.

Microsoft’s 10-K now organizes the company into three segments: Productivity and Business Processes, Intelligent Cloud, and More Personal Computing.

The mission statement has evolved to “empower every person and every organization on the planet to achieve more.” More importantly, the first line of the Business section states directly: “Microsoft is a technology company committed to making digital technology and artificial intelligence (’AI’) available broadly and doing so responsibly.”

The company now leads with Azure—”a comprehensive set of cloud services” that enables customers to “devote more resources to development and use of applications that benefit their organizations, rather than managing on-premises hardware and software.” The Intelligent Cloud segment is discussed first and most extensively.

Microsoft now operates datacenters across multiple global regions. It has built custom AI infrastructure, including purpose-built chips (Azure Maia for AI acceleration, Azure Cobalt for CPUs). It has a “long-term partnership with OpenAI,” in which “Azure powers all of OpenAI’s workloads,” and Microsoft is “OpenAI’s exclusive cloud provider.”

The transformation extends beyond infrastructure. Products that were once sold as perpetual licenses are now subscription services: Office 365, Microsoft 365, and Dynamics 365. Even traditional software like Windows is increasingly delivered via cloud-connected services such as Windows 365.

This isn’t incremental change. This is a fundamentally different business selling fundamentally different products to customers in fundamentally different ways.

Knowing the concepts is one thing. Being able to sit down with a real dividend stock and actually analyze it is another. Paid membership gives you the tools to bridge that gap:

📊 1. Stock Analysis Infographic Library: 180+ visual references covering financial statements, valuation multiples, and dividend metrics, your cheat sheet for analyzing any company

🤖 2. AI Prompt Library: 10 purpose-built prompts that turn AI into a research partner, stress-test your thesis, dig into financials faster, and catch risks you’d otherwise miss

🔧 3. Investing Tools Suite: 4 analytical tools that take the friction out of the numbers so you can focus on understanding the business, not wrestling with spreadsheets

🎓 4. Skill Workshop: Practical working sessions walking through real company analysis start to finish, not theory, not lectures, actual practice

📈 5. Dividend Analysis Course (Coming Soon): A complete step-by-step course on analyzing dividend stocks using Buffett-inspired fundamental analysis

🔓 6. Everything Added Going Forward: Every new resource, tool, and prompts added automatically, no extra charge, ever

Where the Transformation Shows Up in the Numbers

Revenue Composition Changed Dramatically

In FY2014, Commercial Licensing (traditional perpetual software licenses) generated $42.0 billion, and nearly half of the company’s revenue came from selling on-premises software licenses. The “Commercial Other” category, which included early cloud services, was only $7.5 billion.

Today’s segment structure makes direct comparison difficult by design, but the shift is unmistakable. The company now reports “Productivity and Business Processes” and “Intelligent Cloud” as its primary segments, both of which are dominated by subscription- and consumption-based cloud revenue rather than perpetual licenses.

Microsoft doesn’t face the same revenue recognition challenges it did in 2014 when selling primarily perpetual licenses. Cloud subscriptions provide predictable, recurring revenue that accrues ratably over time. This is why unearned revenue (prepaid subscriptions not yet recognized as revenue) has become such an important metric—it represents contracted future revenue.

R&D Investment Scaled With Revenue Growth

Research and development spending grew from $11.4 billion in FY2014 (13.1% of revenue) to $29.5 billion in FY2024 (12.0% of revenue) to $32.5 billion in FY2025 (11.5% of revenue).

In absolute terms, Microsoft nearly tripled its R&D spending over the decade. But as a percentage of revenue, R&D has actually decreased slightly. This is the sign of a successfully scaled transformation. Early-stage transformations require disproportionate R&D investment. Mature transformations should show operating leverage, revenue grows faster than R&D spending once the core platform is built.

Microsoft achieved this by building Azure as a platform that serves both its own products and third-party developers. The same infrastructure investments that support Copilot for Microsoft 365 also generate Azure consumption revenue from customers running their own workloads.

Headcount Grew, But Operating Leverage Emerged

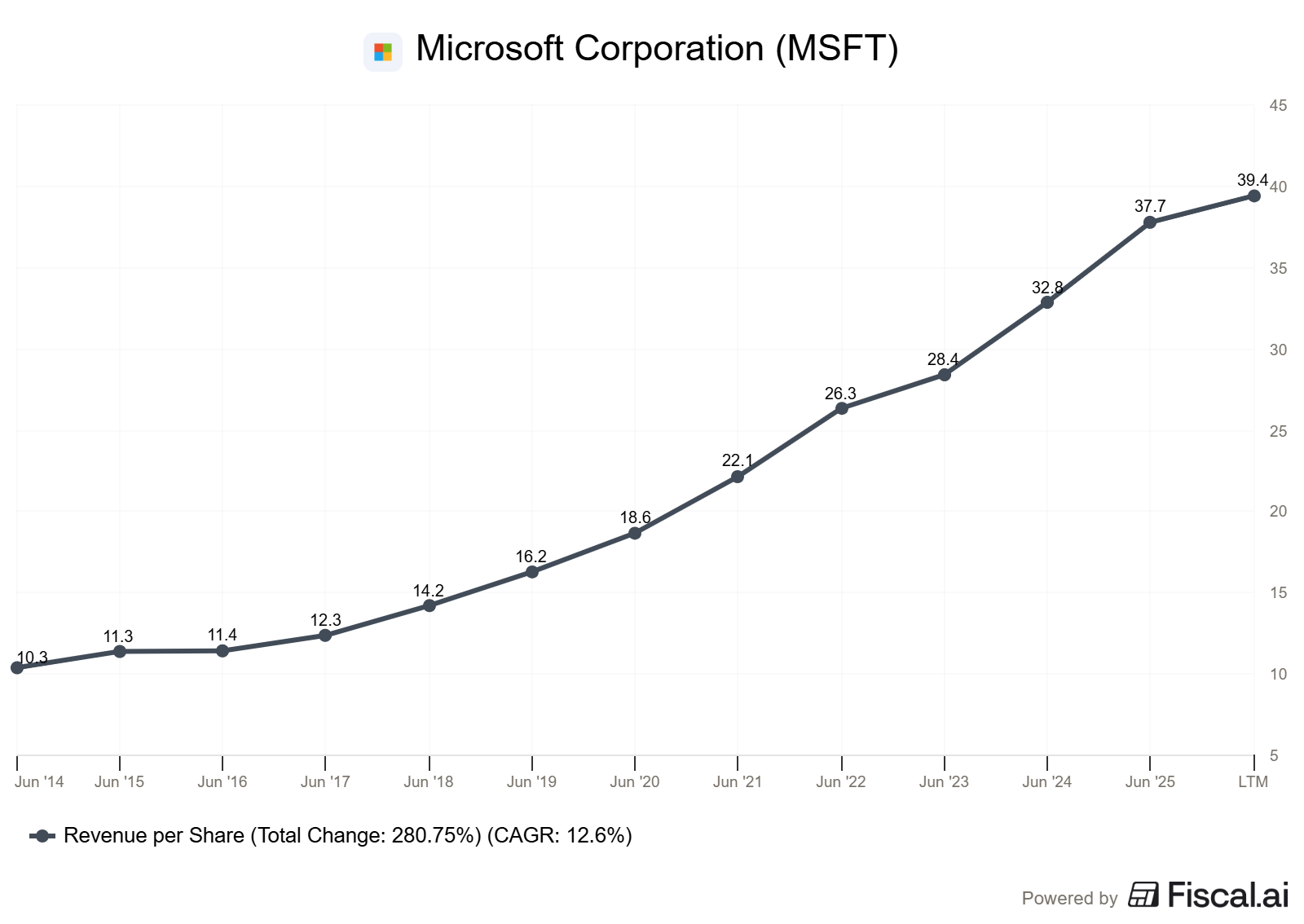

Employment grew from 128,000 in FY2014 to 228,000 in FY2024, a 78% increase. Revenue grew 182% over the same period. Revenue per employee nearly doubled, from $678,000 to $1.075 million.

This workforce growth funded three areas: (1) datacenter operations to support cloud infrastructure, (2) cloud-native engineering talent to build Azure services and AI capabilities, and (3) sales and support for enterprise cloud customers.

The company added 100,000 employees while nearly tripling revenue. That’s operating leverage from a platform business.

Capital Expenditures Exploded

While the 10-Ks don’t make this comparison easy without detailed analysis, Microsoft’s shift from software licensing to cloud infrastructure required a massive capital investment in data centers, servers, networking equipment, and, increasingly, GPUs for AI workloads.

In a traditional software model, capital expenditures are relatively light—you’re selling copies of software you’ve already developed. In cloud infrastructure, you’re running the hardware that executes customer workloads. This is a fundamental shift from selling software to selling computing.

The company absorbed this infrastructure cost because cloud economics work at scale: once built, adding incremental customers to existing data center capacity yields very high gross margins. But you must build the capacity first.

What This Teaches Investors About Corporate Reinvention

The Microsoft story provides a template for evaluating whether a mature company is successfully reinventing itself.

1. The business model should actually change, not just the marketing language

Between 2014 and 2024, Microsoft didn’t just talk about the cloud differently; it rebuilt its entire product-delivery infrastructure. The shift from perpetual licenses to subscriptions isn’t terminology; it’s a change in revenue recognition, customer relationships, and economic incentives.

When a customer buys a perpetual Office license, Microsoft recognizes that revenue immediately and hopes the customer upgrades in three years. When a customer subscribes to Microsoft 365, Microsoft recognizes revenue monthly over the subscription term, and the customer always has the current version. These aren’t the same product with different pricing, they’re fundamentally different businesses.

2. R&D priorities should reallocate decisively

Microsoft tripled R&D spending in absolute terms but maintained it as roughly 11-13% of revenue throughout the transformation. This suggests the company reallocated R&D within that envelope rather than simply spending more everywhere.

In 2014, R&D supported Windows client, Office desktop applications, Xbox games, and early Azure services. By 2024, the priority had shifted to Azure infrastructure, AI models, cloud-native applications, and Copilot integration across the product line.

This reallocation doesn’t show up as a dramatic change in total R&D percentage. It shows up in what products ship and where revenue growth occurs.

3. Revenue mix should shift dramatically over time

A true reinvention means old revenue sources become smaller percentages of the total, even if they’re still growing in absolute terms.

Microsoft’s legacy Windows OEM business likely still generates several billion dollars annually, but it’s now a small fraction of a $282 billion revenue base instead of a cornerstone of an $87 billion business.

The company doesn’t break out all the details in its current filings (segment definitions were specifically changed to make these comparisons harder), but the directional shift is clear: cloud and subscription revenue grew from a minor part of the business to the majority of revenue.

4. Operating margins may compress temporarily, but should eventually expand

Cloud businesses require significant upfront infrastructure investment. If a company is truly building something valuable, those investments should eventually generate operating leverage.

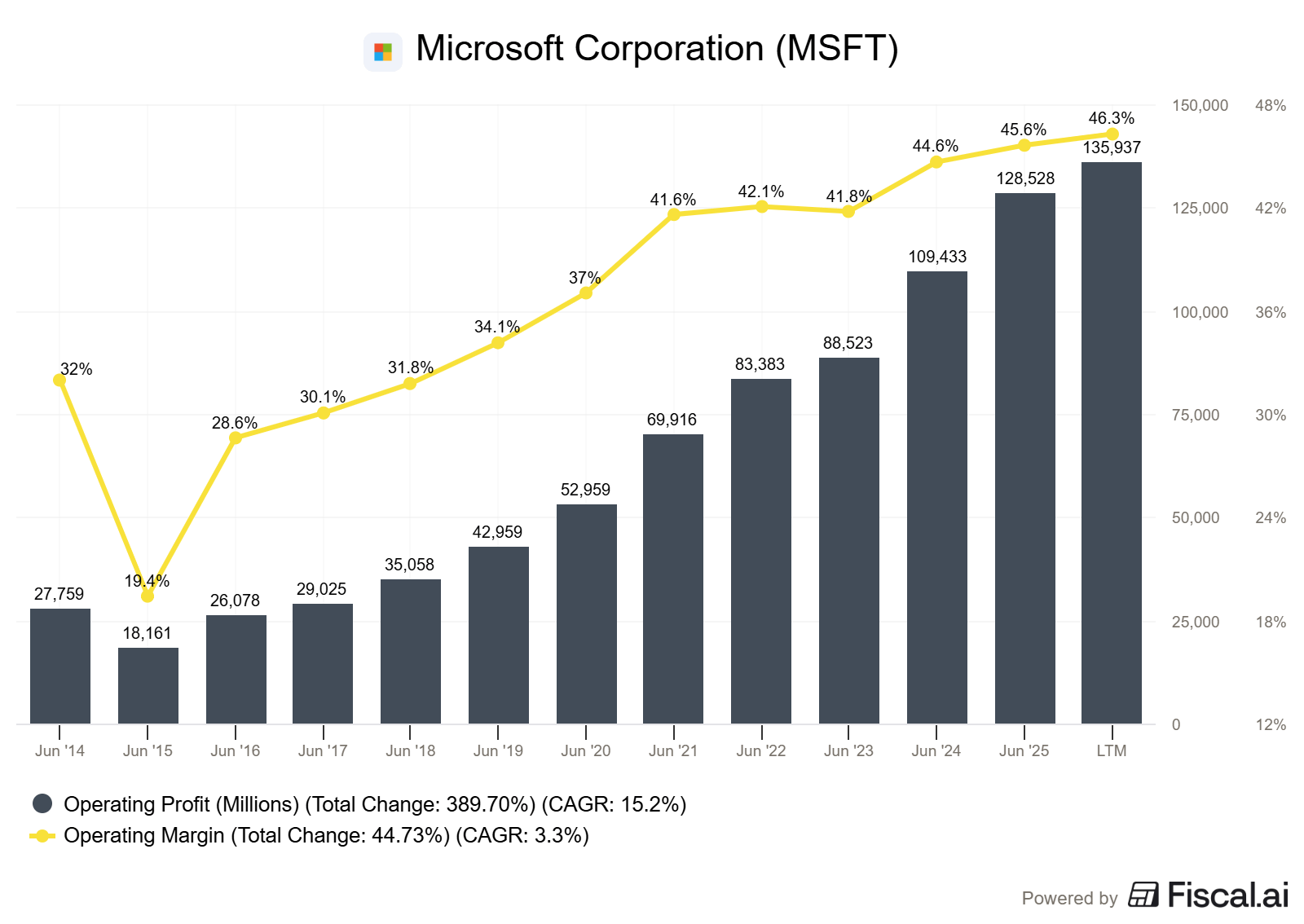

Microsoft’s operating income grew from $27.8 billion in FY2014 (32.0% operating margin) to $109.4 billion in FY2024 (44.6% operating margin) to $128.5 billion in FY2025 (45.6% operating margin).

The company didn’t just grow revenue; it grew operating income faster than revenue. This is the financial signature of successful platform economics.

5. The competitive positioning should strengthen, not weaken

Microsoft’s position in enterprise IT strengthened significantly during this period. Its Azure/Microsoft 365 combination created a moat in enterprise productivity that didn’t exist in 2014.

In 2014, Microsoft competed with Google Docs, Salesforce, and Amazon Web Services as separate threats in separate categories. By 2024, Microsoft had integrated Azure infrastructure, Microsoft 365 productivity tools, Dynamics 365 business applications, and GitHub developer tools into a unified platform. And it had partnered with OpenAI to lead in enterprise AI.

This isn’t reflected in a single financial metric. It’s reflected in customer behavior: enterprises increasingly standardize on Microsoft’s cloud platform because the integration benefits are substantial.

The Takeaway

Microsoft’s transformation wasn’t guaranteed. In 2014, the company was trying to compete with Apple in phones (it failed), with Sony and Nintendo in gaming consoles (it survived but never dominated), and with Google in search (it’s still losing). The Nokia acquisition would eventually result in billions in writedowns.

What made the difference wasn’t picking every battle correctly. It correctly identified which battle mattered most (cloud infrastructure and cloud-delivered productivity software), committed resources decisively to that battle, and executed well enough to become one of two dominant players (alongside Amazon) in enterprise cloud infrastructure.

For investors, the lesson isn’t “buy mature tech companies attempting transformations.” Most transformations fail. The lesson is: When evaluating a potential transformation, look past the press releases to the financial statements.

Ask these questions:

Are capital expenditures shifting? A real transformation requires redeploying capital, not just rebranding existing products.

Is R&D being reallocated? Total R&D spending might not change dramatically, but what the company is building should change completely.

Are revenue streams actually changing? New revenue should grow fast enough that old revenue becomes a smaller percentage of total revenue over time.

Is the operating model different? Moving from software licenses to cloud infrastructure isn’t just a pricing change—it’s a complete change in how the company creates and captures value.

Is competitive positioning improving? Real transformations make the company harder to displace, not just bigger.

In Microsoft’s case, every one of these indicators showed real change. The revenue mix shifted from perpetual licenses to subscriptions. R&D priorities moved from Windows client features to Azure services and AI. Capital expenditures exploded to build datacenter infrastructure. Operating margins expanded as cloud economics matured. Competitive positioning strengthened as integration benefits became clear.

The stock price followed, not because investors were betting on promises, but because the financial evidence of transformation was already showing up in the 10-Ks.

That’s the difference between a press release about transformation and an actual transformation. One is a narrative. The other is a set of facts in SEC filings that investors can verify independently.

When Microsoft said in 2014 that it was becoming a cloud-first company, investors had to decide: believe the narrative or wait for the evidence. By 2016, the evidence was emerging in the numbers. By 2018, it was unmistakable. By 2024, the transformation was complete.

The investors who won weren’t the ones who believed the earliest narratives. They were the ones who knew which financial metrics to watch and started buying when those metrics began to move.

Knowing the concepts is one thing. Being able to sit down with a real dividend stock and actually analyze it is another. Paid membership gives you the tools to bridge that gap:

📊 1. Stock Analysis Infographic Library: 180+ visual references covering financial statements, valuation multiples, and dividend metrics, your cheat sheet for analyzing any company

🤖 2. AI Prompt Library: 10 purpose-built prompts that turn AI into a research partner, stress-test your thesis, dig into financials faster, and catch risks you’d otherwise miss

🔧 3. Investing Tools Suite: 4 analytical tools that take the friction out of the numbers so you can focus on understanding the business, not wrestling with spreadsheets

🎓 4. Skill Workshop: Practical working sessions walking through real company analysis start to finish, not theory, not lectures, actual practice

📈 5. Dividend Analysis Course (Coming Soon): A complete step-by-step course on analyzing dividend stocks using Buffett-inspired fundamental analysis

🔓 6. Everything Added Going Forward: Every new resource, tool, and prompts added automatically, no extra charge, ever

I like to compare company stories like these to the story of Sears. Sears saw the Internet coming and didn't adapt to the changes and so Amazon swooped in and took their place as the shopping giant. Microsoft saw a change coming before GenAI hit and they adapted accordingly. Could have been the same result but Microsoft chose to adapt and change where Sears decided to stick with what they knew.