Is Chevron’s Dividend in Trouble?

Chevron just raised its dividend for the 39th consecutive year. A 4% bump to $1.78 per share each quarter. That puts the annual payout at $7.12 per share with a yield hovering around 3.4%.

For a company with nearly four decades of unbroken dividend growth, that sounds like exactly the kind of stock dividend investors love to own. Predictable. Reliable. Boring in the best way.

But there’s a number buried in Chevron’s financials that should make you pause.

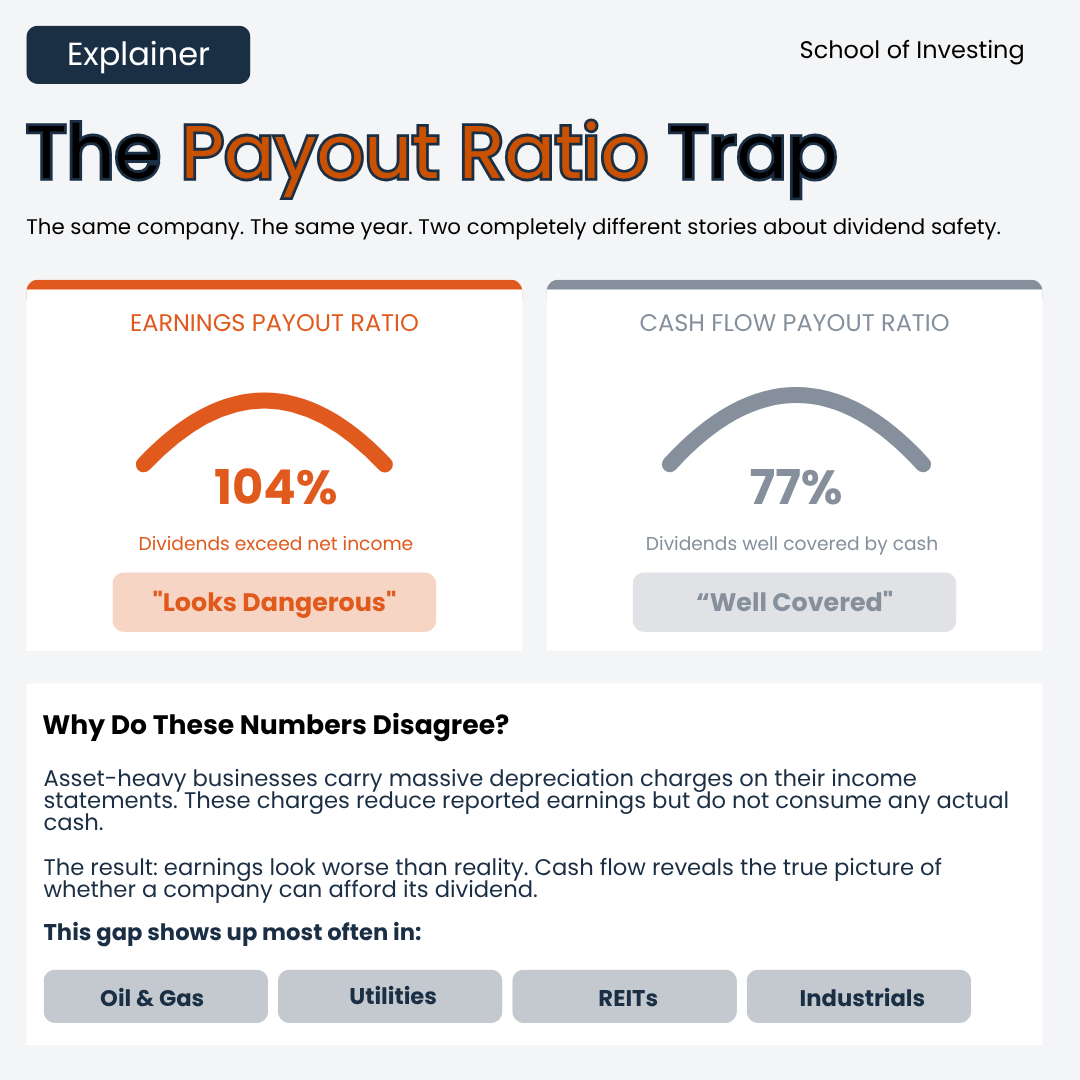

The earnings payout ratio is running above 100%.

That means Chevron is paying out more in dividends than it earned in net income last year. Full year 2025 earnings came in at $12.3 billion, or $6.63 per share. The dividend obligation was roughly $12.8 billion. On an earnings basis, Chevron is underwater.

If you stopped there, you might conclude the dividend is on borrowed time. A lot of investors stop there. They see a payout ratio over 100%, assume the worst, and move on to something that looks safer on a screener.

But that reaction misses something important about how oil companies actually work.

The Gap Between Earnings and Reality

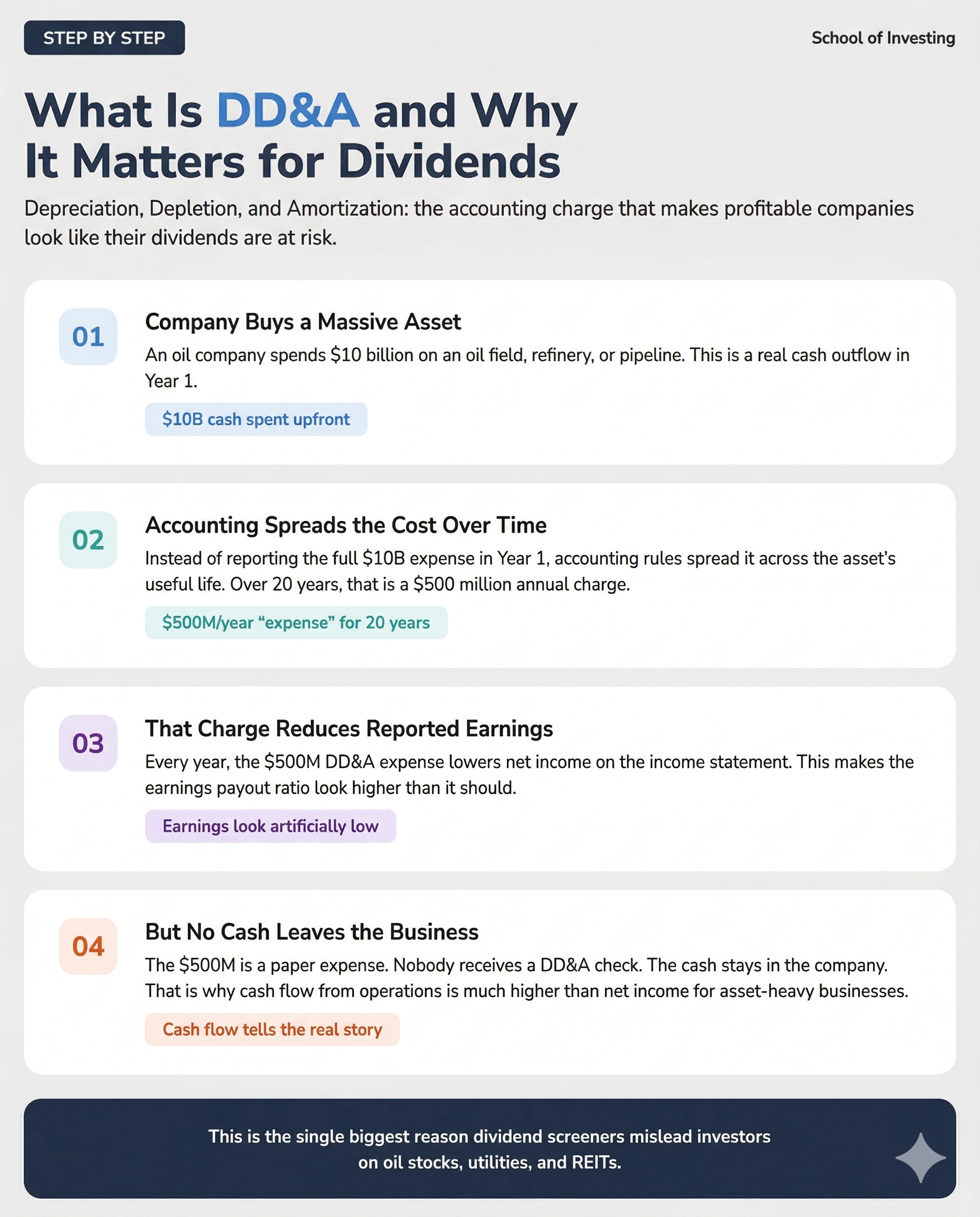

Chevron operates one of the largest asset bases in the energy industry. Oil rigs, refineries, pipelines, drilling equipment, and reserves in the ground. These physical assets get depreciated and depleted on the income statement every single year. That depreciation expense significantly reduces reported earnings.

Here is the thing. Depreciation is an accounting charge, not a cash expense. Chevron is not writing a check to anyone for depreciation. The cash stays in the business.

So, when you look at cash flow from operations rather than net income, the picture changes. Chevron generated strong enough cash flow in 2025 to fund the entire $12.8 billion dividend, buy back $12.1 billion in stock, and still close a $55 billion acquisition of Hess Corporation.

The cash flow payout ratio sits around 86%. That is a completely different story than 104%.

Why This Matters for Your Portfolio

This is one of the most common traps in dividend investing. The earnings payout ratio and the cash flow payout ratio can tell you opposite things about the same company. For asset-heavy businesses like oil majors, utilities, and REITs, the earnings number almost always overstates the actual strain on the dividend.

Knowing which number to trust, and when, is the difference between selling a perfectly healthy dividend stock in a panic and holding with confidence through a down cycle.

That skill, knowing which metric to use and when, is exactly what the paid tier of School of Investing is built around. Each month, Stock Under the Microscope walks through a real company using the full analytical toolkit: cash flow payout ratios, balance sheet stress tests, margin structure, and AI-assisted scenario analysis.

This month, it’s Chevron. Wednesday’s analysis goes deeper than anything in this article.

What Else Is Going On With Chevron

The Hess acquisition closed in July 2025 after a 19-month saga that included an arbitration battle with ExxonMobil over rights to Guyana’s Stabroek Block. Chevron won. That gives them a 30% stake in one of the largest oil discoveries in the last decade, with over 11 billion barrels of recoverable oil.

Production hit record levels in 2025, up 12% worldwide. The Permian Basin crossed 1 million barrels per day. These are real growth drivers that should support cash flow going forward.

But the acquisition also pushed Chevron’s debt ratio up to around 18%, compared to roughly 12-13% before the deal. Net debt-to-cash flow from operations is about 1.2x. The balance sheet absorbed a massive deal and is still in reasonable shape, but it is noticeably more leveraged than it was two years ago.

That creates a second question worth answering: can Chevron maintain its current pace of buybacks ($12 billion a year) while paying down acquisition debt and funding the dividend? Or does something have to give?

The Three Things I Would Watch

If I were evaluating Chevron as a dividend holding today, I would focus on three things each quarter:

Payout ratio on a cash flow basis, not just earnings. The earnings number will keep looking scary as long as commodity prices stay moderate. The cash flow number tells you whether the dividend is actually funded.

The pace of shareholder returns vs. debt reduction. Chevron returned $27.1 billion to shareholders in 2025. That is aggressive for a company that just took on $55 billion in acquisition debt. Watch whether management starts shifting dollars from buybacks toward the balance sheet.

Guyana production ramp. This is the growth story that justifies the Hess deal. If Stabroek Block production scales on schedule, it adds low-cost barrels that improve margins regardless of where oil prices go. If it stalls, the math gets tighter.

Going Deeper

This month’s paid Analysis walks through Chevron step by step using the tools available to paid subscribers. I ran the numbers through the Dividend Safety Calculator, broke down the margin structure using the analysis spreadsheet, and used an AI research prompt to stress-test the shareholder return program at different oil price scenarios.

The 104% earnings payout ratio tells one story. The cash flow analysis told a completely different story. And the AI prompt surfaced a risk I had not considered about the buyback pace.

The Wednesday walkthrough covers the full cash flow analysis, the balance sheet stress test at different oil price scenarios, and the one risk the AI prompt surfaced that I wasn’t expecting going in.

If you want to run this kind of analysis on any stock in your portfolio, not just read about it, that’s what paid membership gets you.

School of Investing is an educational resource. Nothing here is investment advice or a recommendation to buy or sell any security.