Down 51%. Yielding 4.6%. 20 Straight Raises. Is Accenture ($ACN) a Bargain at 10x Earnings?

A 20-year raise streak suddenly yields 4.6%. That only happens for one of two reasons. I checked which.

Accenture is the world’s largest publicly traded consulting and technology services firm, a net-cash balance sheet with a dividend that has grown 13% a year for five years, now trading at less than half its 52-week high because the market believes AI will eat its business model.

1. The stock everyone loved at $290 now yields 4.6%

Accenture was one of the 20 worst performers in the S&P 500 in the first half of 2026.

Read that again. A company with $69.7 billion in revenue, a 20-year record of dividend increases, and more cash than debt lost over half its value in six months. The 52-week range tells the story in one line: $118.15 to $291.09. The stock closed at $142.14 on July 7, 2026.

Here’s the part that got my attention.

While the stock was falling, the business kept reporting growth. Revenue rose 7% through the first nine months of fiscal 2026. EPS grew 9% last quarter. The board raised the dividend 10% in September 2025 and free cash flow guidance still sits at $10.8 to $11.5 billion for the year.

A falling stock and a growing business can only mean one thing: the market is repricing the future, and it is doing so violently.

So the question this deep dive will answer is simple. Is Accenture a wounded blue chip offering a once-in-a-decade starting yield near 4.6%, or is it a value trap where AI slowly dissolves the business underneath the dividend?

Let’s dive in.

2. The bet

Accenture is a bet that large enterprises will pay a trusted partner to install AI for them, and that the disruption everyone fears becomes the biggest project pipeline in the company’s history.

For income investors, the math has never looked like this. You are being offered a forward yield of roughly 4.6% (against a five-year average near 1.5%) from a company paying out less than half its earnings, with a raise streak stretching back two decades.

If the business merely stagnates, the dividend still looks well covered. That is the bet.

3. What the company does

Accenture solves a problem every big company has: they know what technology they need, and they have no idea how to build it, run it, or roll it out to 100,000 employees.

Think of Accenture as the general contractor of the corporate world. When a bank wants to move its systems to the cloud, when a retailer wants an AI agent handling customer service, when a government agency needs its digital infrastructure rebuilt, they rarely do it themselves. They hire Accenture to design the plan, supply the specialists, and often run the finished system for years afterward.

The scale is hard to picture.

People: approximately 799,000 employees worldwide

Clients: approximately 9,000, concentrated among the world’s largest companies

Revenue: $69.7 billion in fiscal 2025, from the fiscal 2025 fourth-quarter earnings release

Those numbers come straight from the company’s own materials, and they make Accenture the largest pure-play IT services and consulting firm on the planet.

One quirk worth knowing: Accenture’s fiscal year ends August 31. So fiscal 2026 is already three quarters reported as I write this, with the year closing next month. Keep that in mind whenever you compare its numbers to calendar-year companies.

The client list is the moat’s foundation, and we will get to that in section five. For now, know that Accenture serves most of the Fortune Global 500, and these relationships run so deep that the company reported 104 client bookings of $100 million or more through the first nine months of fiscal 2026, up 13% from the prior year (Q3 fiscal 2026 earnings release).

Companies do not sign nine-figure contracts with vendors they are about to abandon.

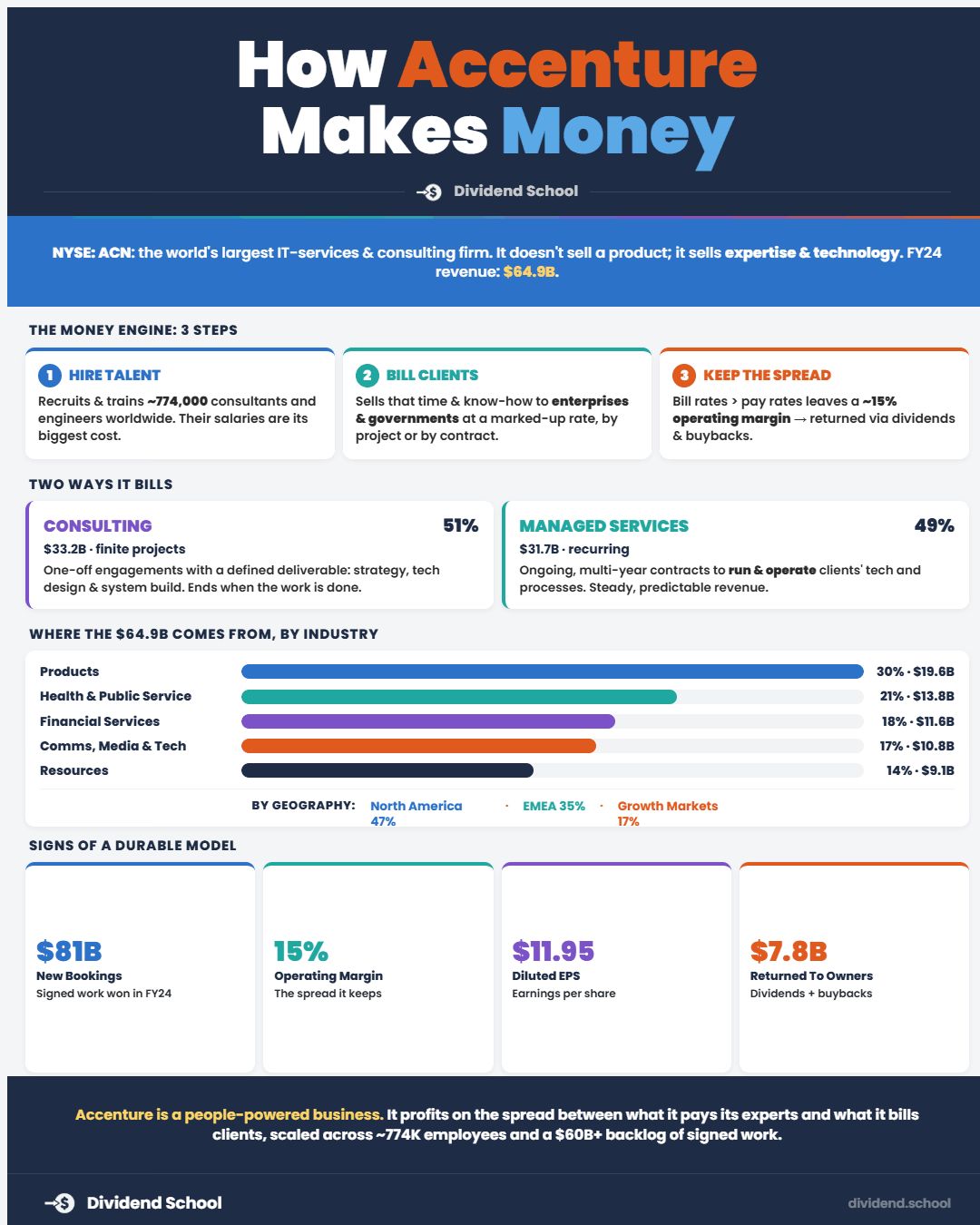

4. How they make money

Accenture sells two things: brains and operations. The company reports them as Consulting and Managed Services, and they are almost exactly the same size.

Consulting is project work. Design the strategy, build the system, integrate the software, then hand over the keys. It is higher touch and more sensitive to the economy, because projects are easy to delay when budgets tighten.

Managed Services is the recurring engine. Accenture runs your technology, your back office, your security operations, on multi-year contracts. This is the closest thing a consulting firm has to subscription revenue.

Here’s how the third quarter of fiscal 2026 split out, from the June 18, 2026 earnings release:

Consulting: $9.33 billion, up 4% in U.S. dollars

Managed Services: $9.39 billion, up 8% in U.S. dollars

Total: $18.72 billion, up 6% in U.S. dollars and 3% in local currency

Managed Services is growing faster, and that matters for dividend investors: the more recurring the revenue, the steadier the cash flow that funds the payout.

Geographically, the Americas is the biggest market at $9.14 billion for the quarter, with EMEA at $6.87 billion and Asia Pacific at $2.71 billion. EMEA grew 10% in U.S. dollars last quarter, the fastest of the three, though a chunk of that was currency.

The company also slices revenue by industry: Products (consumer goods, retail, travel) is the largest group at $5.67 billion for the quarter, followed by Health & Public Service at $3.85 billion, Financial Services at $3.49 billion, Communications, Media & Technology at $3.22 billion, and Resources at $2.50 billion.

Notice how spread out that is. No single industry drives the bus, which is exactly what you want from a dividend payer: diversified demand smooths the cash flows.

Now for the headline numbers. Here’s the fiscal 2025 scorecard, from the fourth-quarter fiscal 2025 earnings release (September 25, 2025):

Revenue: $69.7 billion, up 7% in U.S. dollars and local currency

GAAP diluted EPS: $12.15, up 6%

Adjusted EPS: $12.93, up 8% (excludes $0.78 of business optimization costs)

Free cash flow: $10.9 billion

Cash returned to shareholders: $8.3 billion ($3.7 billion dividends, $4.6 billion buybacks)

And the fiscal 2026 picture through three quarters, from the June 18, 2026 release:

Nine-month revenue: $55.5 billion, up 7% in U.S. dollars and 4% in local currency

Q3 GAAP diluted EPS: $3.80, up 9%

Full-year GAAP EPS guidance: $13.38 to $13.50, a 10% to 11% increase

Full-year free cash flow guidance: $10.8 to $11.5 billion

Capital return guidance: at least $9.5 billion

A business the market has repriced as broken is guiding to double-digit EPS growth and record free cash flow.

5. Moat and competition

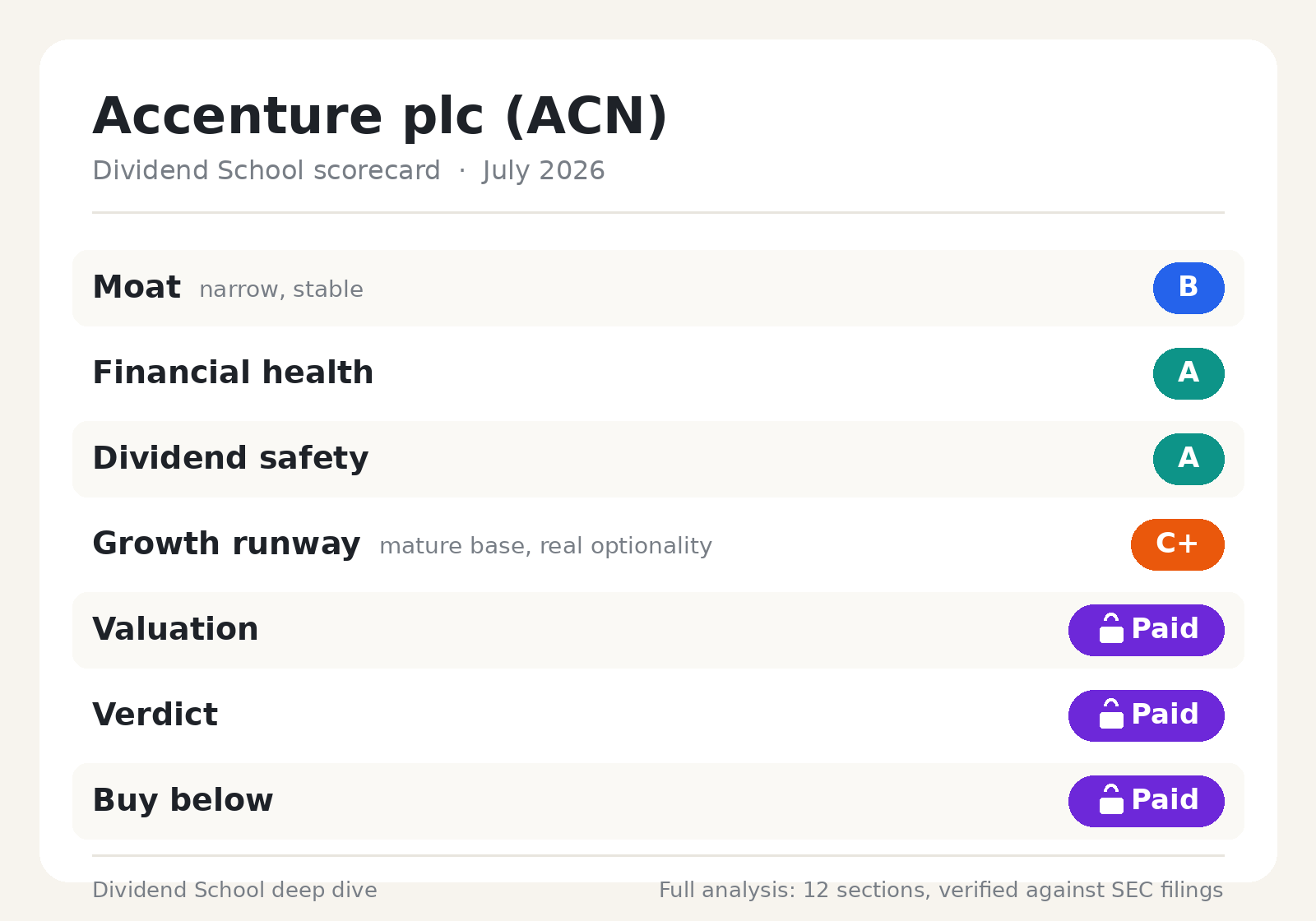

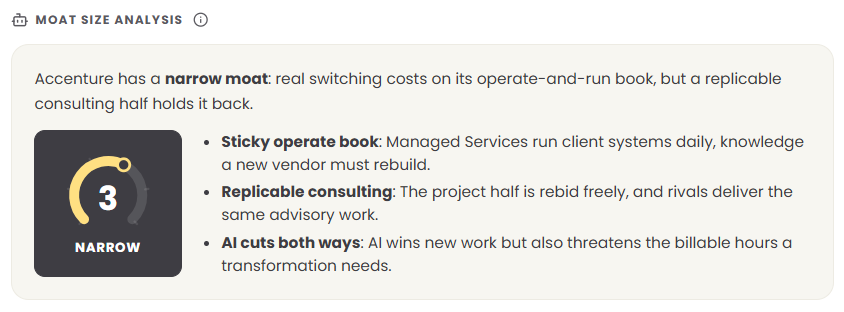

Accenture has a moat. It is narrower than the company’s size suggests, and knowing exactly where it sits is the key to this whole thesis.

Half of Accenture is protected. Half of it is a knife fight.

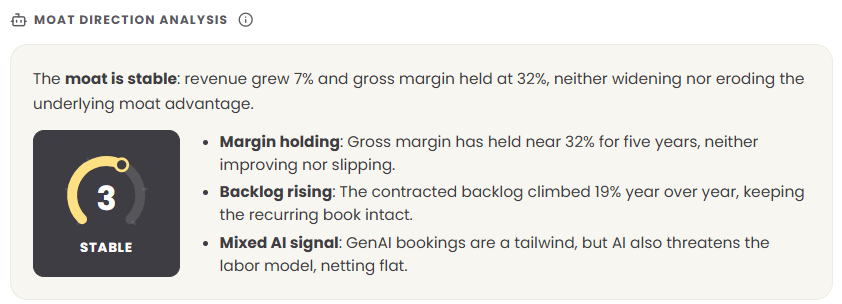

Where the moat is real: the managed-services book. Managed Services generated $34.6 billion in fiscal 2025, roughly half of total revenue, and it is backed by about $37 billion of remaining performance obligations (contracted work already signed), up around 19% in the latest reporting.

This is the operate-and-run business, and the switching costs here are the genuine article. Accenture teams sit inside the client’s systems every day, accumulating years of institutional knowledge about how that specific estate actually works. A client that wants to leave mid-program has to find a replacement vendor, transfer all of that knowledge, and accept disruption to systems running the business right now.

Leaving hurts more than the fees do. That friction is why these relationships persist across multi-year cycles, and why the recurring half of the business grew 8% last quarter while consulting grew 4%.

Where the moat is thin: the consulting half. Project-based consulting work gets rebid freely at the end of each phase. Deloitte (around $70 billion in global revenue) runs a near-identical model and competes for the same boardrooms. IBM Consulting chases the same integration work. TCS and Infosys were built on the offshore-cost playbook and can undercut on price all day, because low-cost delivery already is their business.

None of these rivals gives anything up by copying Accenture. When competitors can copy you freely and without penalty, that half of the business earns no moat.

Running the other moat sources through the checklist. Let’s be honest about what Accenture does and does not have:

Network effects: none. Winning a new bank client adds nothing for the existing automaker client. Engagements are bilateral: one client, one team, one outcome.

Low-cost production: none. Gross margin has held near 32% for five years. A real cost advantage would show up as expanding margins, and it has not.

Brand: average. The name gets Accenture in the room and reduces perceived risk when a board signs a nine-figure transformation. Buyers still run competitive bids against Deloitte, IBM, and the Indian majors, so the brand supports positioning without granting pricing exclusivity.

Scale: real, but internal. 799,000 people means Accenture can staff a 2,000-person global rollout next month. Clients benefit from that as execution quality; they never feel it as lock-in.

One sticky source (switching costs on the operate-and-run book) plus scale earns a narrow moat. The replicable consulting core keeps it from being wide.

What the returns on capital say. High returns held over time are the standard test, so let’s run the fiscal 2025 numbers:

Operating margin: 14.7% GAAP (15.6% adjusted), from the Q4 fiscal 2025 release

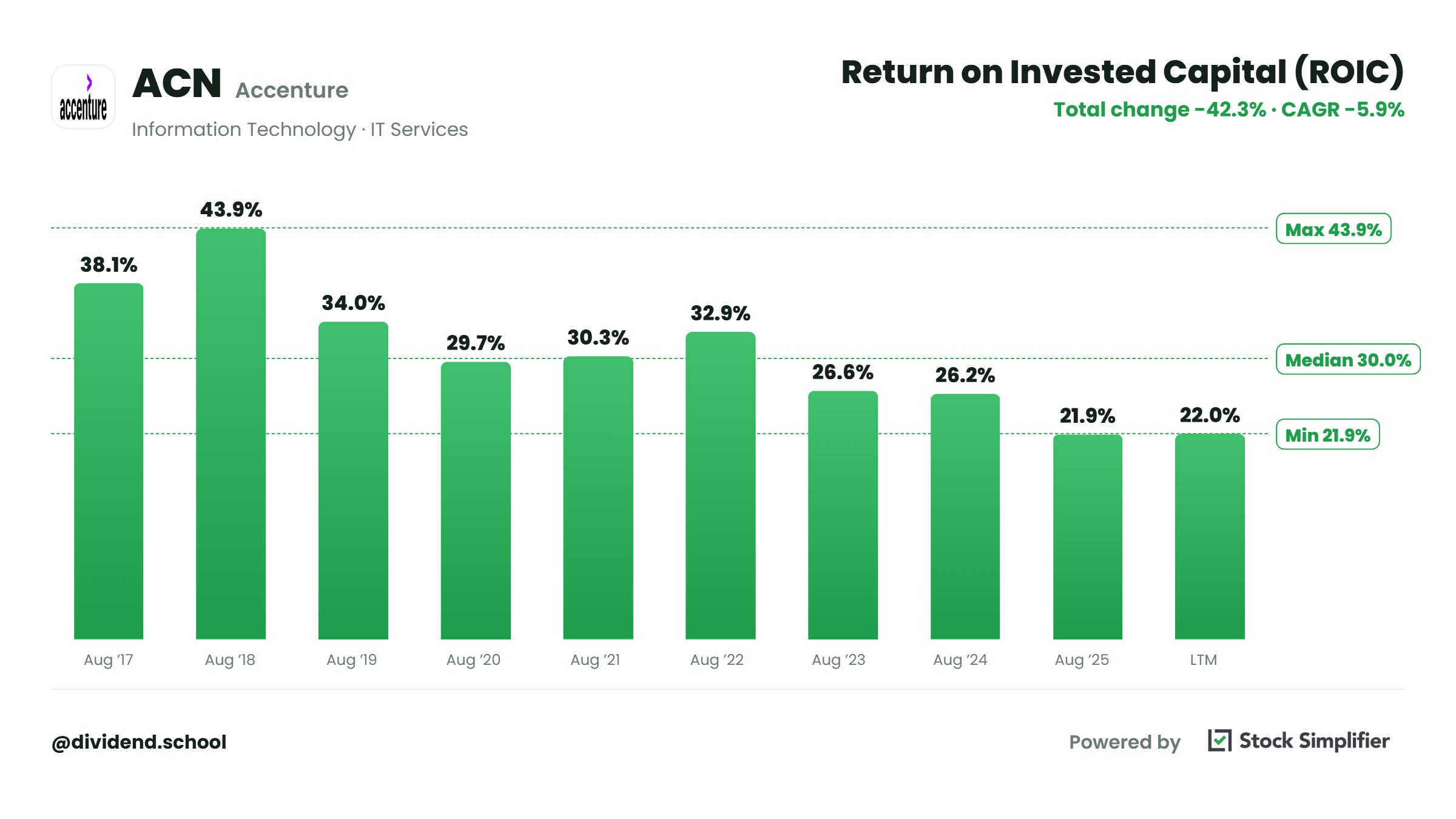

Return on equity: $7.7 billion net income against $31.2 billion of equity, roughly 25%

Return on invested capital: about 21% by my math; Stock Simplifier’s stricter method says 17%

Those returns look wide-moat at first glance. The reconciliation is that consulting is asset-light, so even fiercely contested work produces high returns on capital while it lasts. The returns confirm a quality business; the flat gross margin confirms the competition is real. Both things are true.

The AI swing factor. AI is the variable that decides whether this narrow moat widens or erodes, and the signal today is mixed. Generative AI bookings hit $5.9 billion in fiscal 2025 (Q4 fiscal 2025 release) and management is targeting much more. If that work converts into deeper, stickier managed-services contracts, the switching-cost moat widens. If AI compresses the billable hours a transformation requires faster than new AI work replaces them, the consulting half thins out.

The two tells I am watching: whether AI bookings keep converting into the recurring book, and whether gross margin finally breaks out of its 32% flatline in either direction. Margin expansion would say AI delivery is creating a real cost gap. Margin erosion would say the offshore rivals are winning the pricing war.

My verdict: a narrow moat, stable for now, concentrated in exactly the half of the business that funds the dividend. Section 10 stress-tests what happens if the AI bears are right.

6. Financials

Let’s put the whole business on the table and ask one question: is this a high-quality company?

Is revenue growing? Yes, at a mid-single-digit clip.

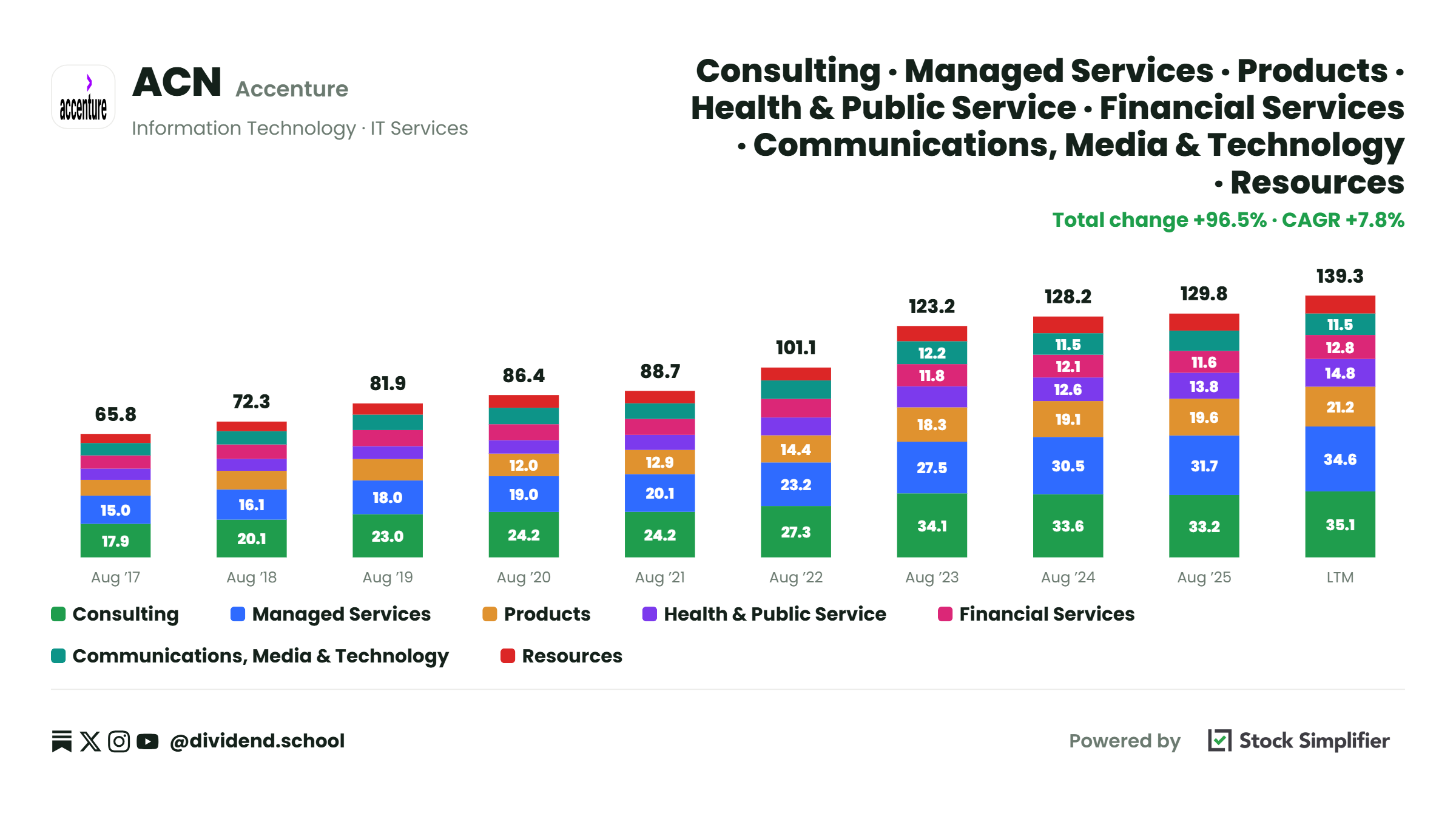

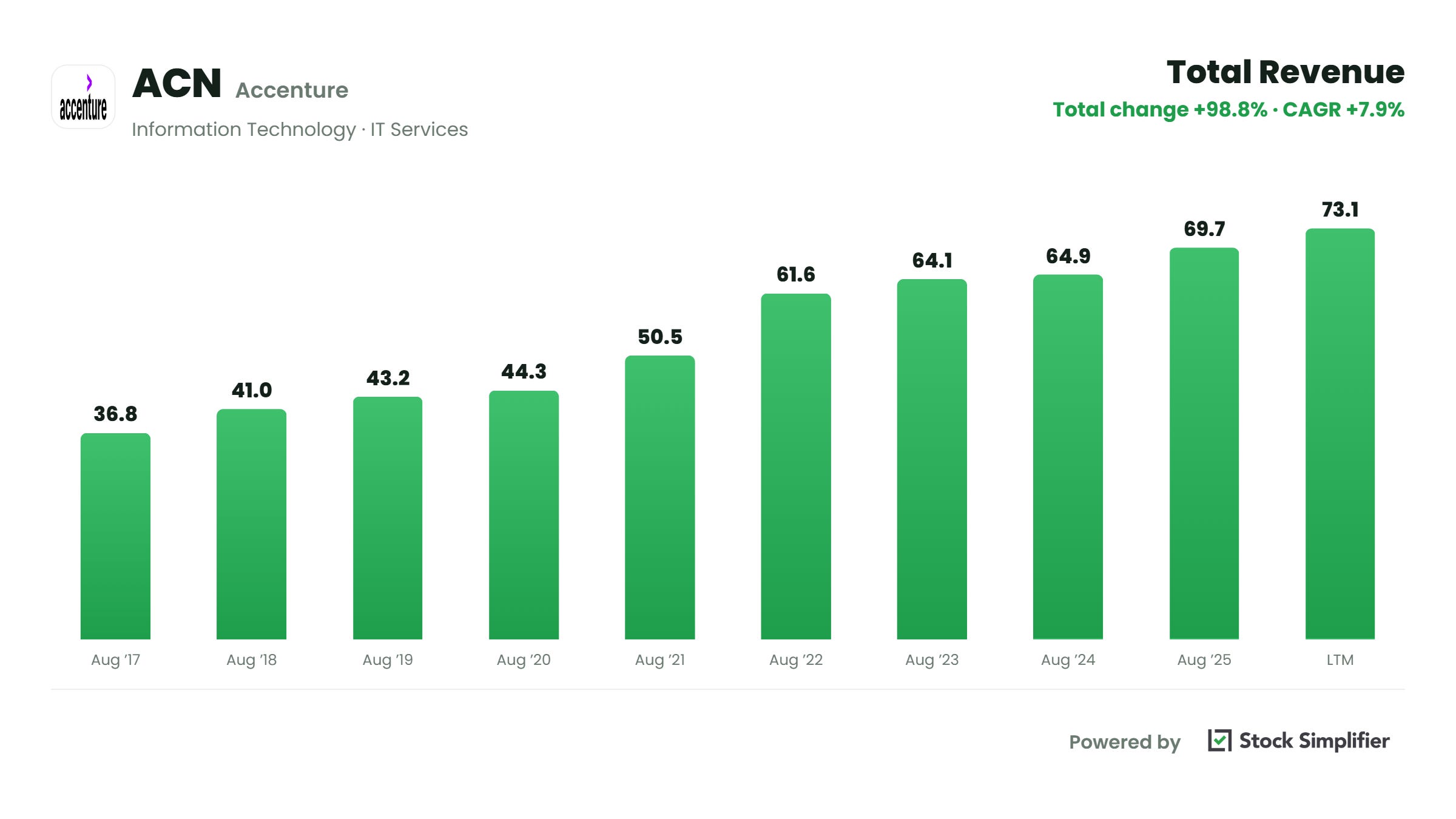

Fiscal 2024: $64.9 billion

Fiscal 2025: $69.7 billion, up 7%

Fiscal 2026 (nine months): $55.5 billion, up 7% in U.S. dollars and 4% in local currency

All figures from the Q4 fiscal 2025 and Q3 fiscal 2026 earnings releases. This is a grower, just a measured one. Management guides fiscal 2026 to 3% to 4% local-currency growth, or 4% to 5% excluding an estimated 1% drag from the U.S. federal business.

Are margins healthy and moving the right way? Yes.

Q3 fiscal 2026 operating margin: 17.0%, up 20 basis points year over year

Fiscal 2026 full-year guidance: 15.3% GAAP operating margin, 60 basis points of expansion over fiscal 2025

Gross margin last quarter: 32.8%

For a people business with 799,000 salaries to pay, holding margins while growing is a sign of pricing power and cost discipline. The company also completed a business optimization program (mostly severance) that cost $615 million in Q4 fiscal 2025 and $308 million in Q1 fiscal 2026, which is why GAAP and adjusted numbers differ this year.

Is the balance sheet safe? This is where Accenture separates itself from almost every high-yield stock.

From the May 31, 2026 balance sheet in the Q3 fiscal 2026 release:

Cash and equivalents: $10.2 billion

Total debt: $5.1 billion ($5.03 billion long-term plus $113 million current)

Net cash position: roughly $5 billion

Total assets: $68.8 billion

Shareholders’ equity: $31.9 billion (Accenture plc portion)

A 4.6% yielder with more cash than debt is rare. Most stocks with this yield carry leverage; Accenture could retire every dollar of debt tomorrow and still have $5 billion left over.

Interest coverage makes the point even louder. Fiscal 2025 operating income of roughly $10.2 billion against interest expense of $229 million (Q4 fiscal 2025 release) works out to coverage of about 45 times. Stock Simplifier shows 44.7x, which matches my math. Debt is a rounding error here.

Does it convert earnings to cash? Beautifully, and this is the number one thing I check for any dividend payer.

Fiscal 2025 operating cash flow: $11.5 billion

Fiscal 2025 capital expenditures: $0.6 billion

Fiscal 2025 free cash flow: $10.9 billion

Free cash flow of $10.9 billion against net income of $7.7 billion means cash conversion above 140% of earnings. Consulting requires almost no capital: no factories, no inventory, no fleets. People walk in, bill hours, and the cash shows up.

Through nine months of fiscal 2026, operating cash flow is $9.3 billion with just $492 million of capex, so free cash flow is running at $8.8 billion with a quarter to go, tracking management’s $10.8 to $11.5 billion full-year guide.

Add it up. Growing revenue, expanding margins, net cash, 45x interest coverage, and a business that turns more than a dollar of every earnings dollar into cash.

This is a high-quality business. The financials are not the risk here.

That’s the free half: the business, the moat, and the financials, every number checked against the filings. The quality question is settled.

The money question is still open. A stock that yielded 1.5% for a decade now pays 4.6%, and that only happens when the market is wrong about the business or the dividend is about to stop growing. The rest of this deep dive tests which.

Below the paywall, members get:

The dividend safety deep dive. Seven tests against the SEC filings, including the one four-year trend in the payout that made me pause.

The growth runway. Where the raises come from when a $70 billion firm grows 4% a year.

Management’s report card. What Julie Sweet did with $8.2 billion of your fellow shareholders’ cash this year.

The honest bear case, ranked. Including the one risk nobody, not even management, can disprove yet.

My three-lens valuation. The multiples, a DCF where I gave the bears the heaviest weight, and a reverse DCF that asks what today’s price actually assumes. That last answer is the single most surprising number in this piece.

The verdict and my Buy Below price, plus the four tripwires that would send this thesis back to the shop.

Membership is $369 a year or $35 a month, with a 30-day money-back guarantee.

Want to see a complete member deep dive before you decide? My full Johnson & Johnson analysis is unlocked, free, start to finish: JNJ Article