How Visa Makes Money: The Toll Booth on Global Commerce

Most investors think Visa is a credit card company. It’s not. Visa doesn’t lend money. It doesn’t issue cards. It doesn’t charge interest. And yet, over the last decade, it has quietly grown from a $13.9 billion business into a $40 billion one.

Understanding how Visa actually makes money is one of the most important lessons in business model analysis.

Today, I’ll break down the machine behind the world’s largest payment network, show you exactly where every dollar of revenue comes from, and explain why this business has produced some of the most consistent financial results in public markets over the past ten years.

What Visa Actually Does

Before we get into the numbers, we need to clear up the most common misconception about this company.

Visa does not issue cards. It does not extend credit. It does not set the interest rates you pay on your credit card balance. As the company states in its fiscal 2024 10-K filed with the SEC: “We do not earn revenues from, or bear credit risk with respect to, interest or fees paid by account holders on Visa-branded cards or payment products.”

That sentence is the key to understanding the entire business.

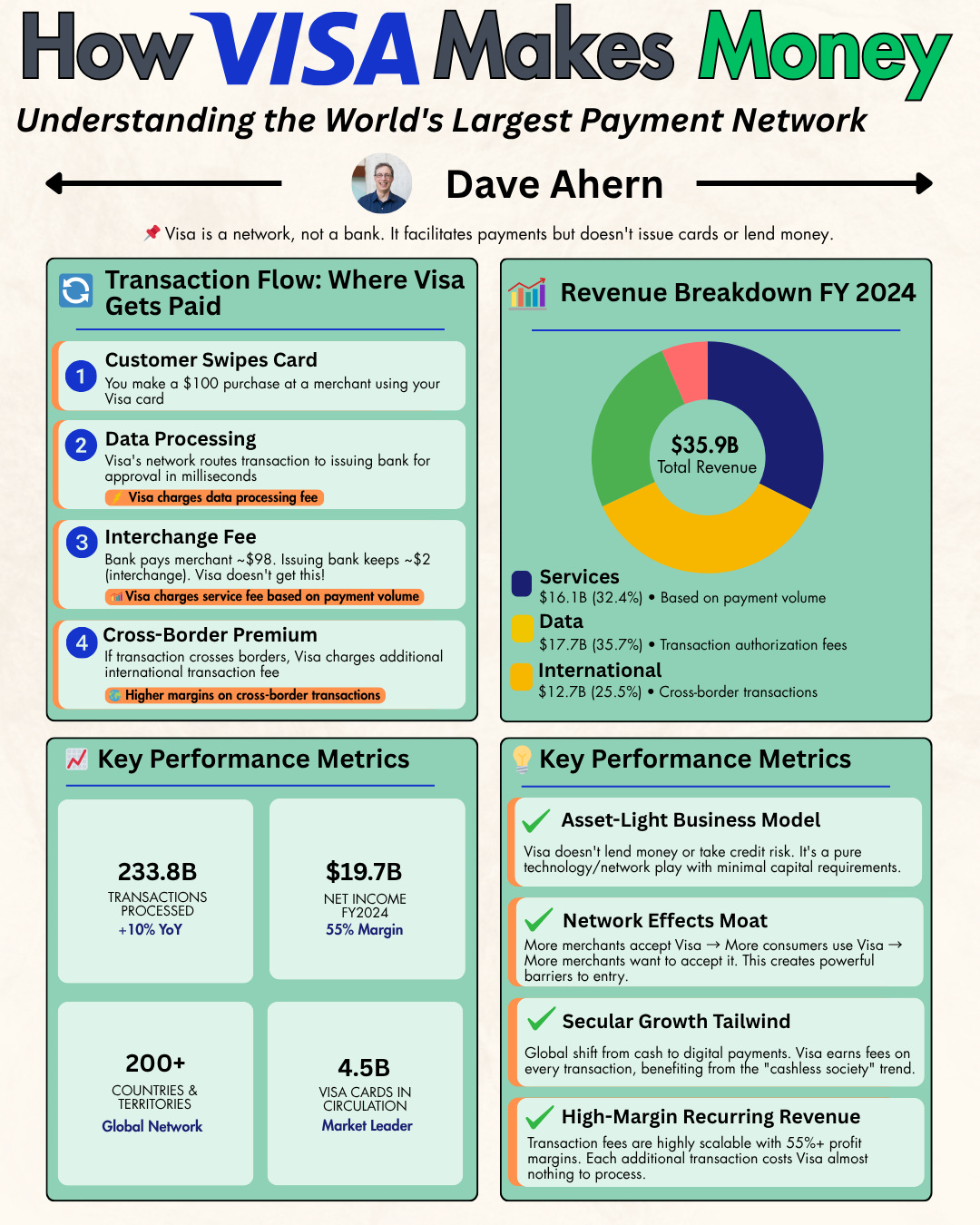

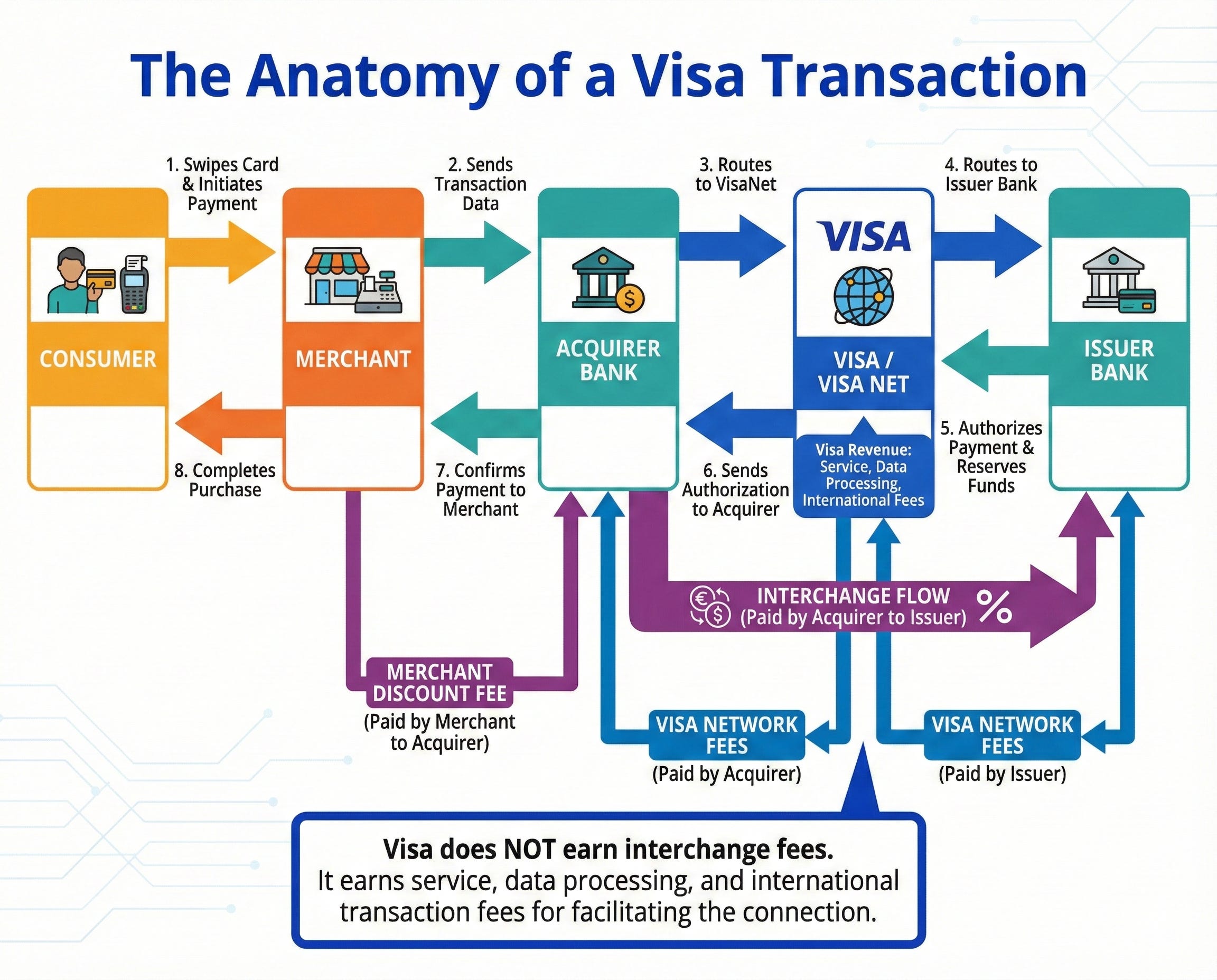

When you swipe your Visa card at a coffee shop, you’re initiating a chain of events that involves four parties: you (the cardholder), your bank (the issuer), the coffee shop’s bank (the acquirer), and Visa (the network sitting in the middle). Your bank issued your card. The coffee shop’s bank processes the payment. Visa’s role is to connect the two banks through its network, VisaNet, which authorizes, clears, and settles transactions in milliseconds.

Think of it this way. Visa is a toll booth on the highway of global commerce. Every time money moves through its network, Visa collects a small fee. It doesn’t own the cars (the cards). It doesn’t own the destinations (the merchants). It owns the road.

This is what makes Visa’s business model so elegant. It captures a small share of every transaction without assuming the credit risk banks bear. If a cardholder defaults on their bill, that’s the issuing bank’s problem. Not Visa’s.

The Four Revenue Streams

Visa’s revenue comes from four distinct sources. According to the company’s fiscal 2025 earnings release (for the year ending September 30, 2025), the breakdown looks like this:

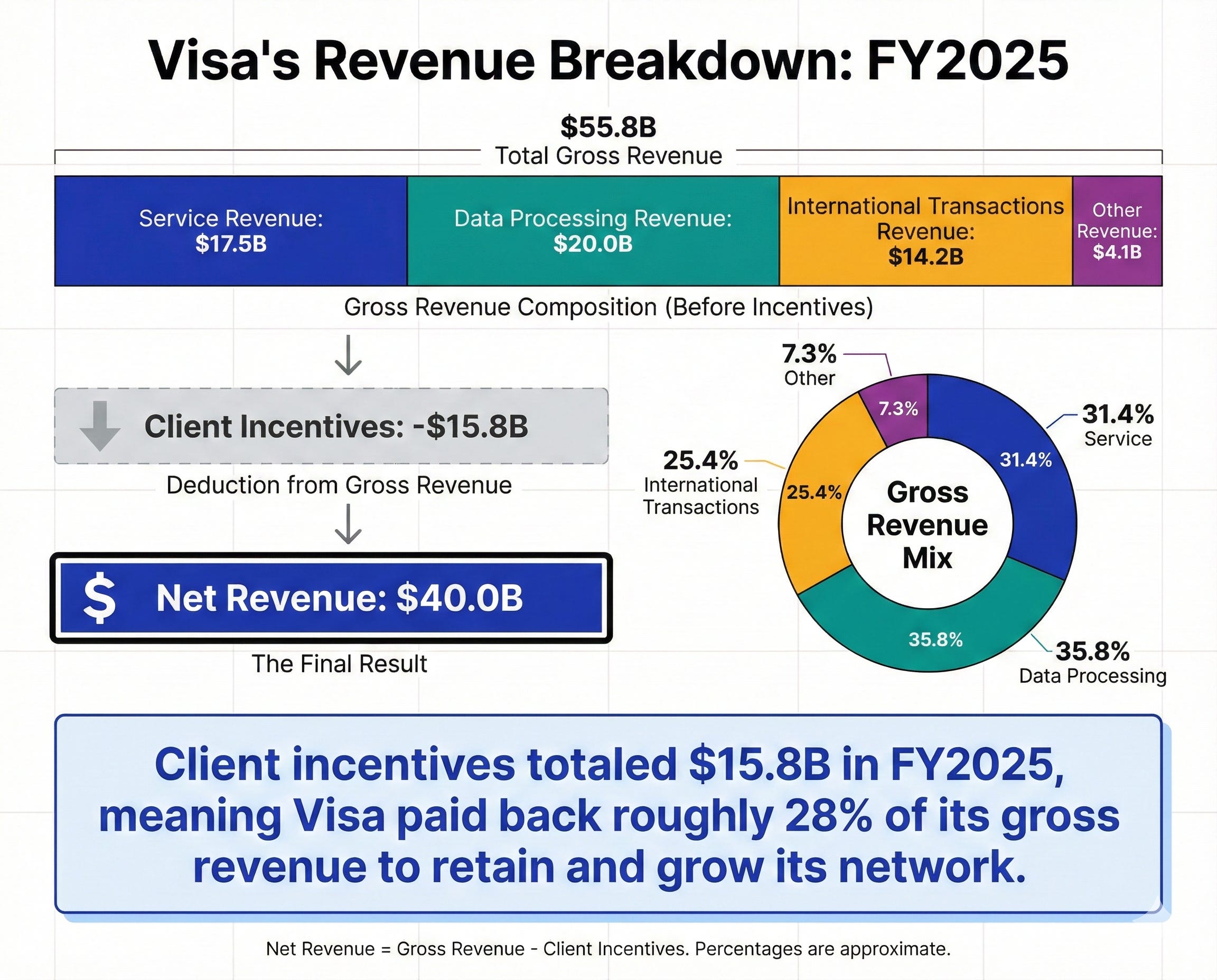

Service Revenue: $17.5 billion (grew 9% year over year)

This is what Visa earns from financial institutions for the right to use Visa-branded products and services. The driver here is payment volume, the total dollar amount of purchases made on Visa-branded cards. Service revenue is actually recognized with a one-quarter lag, meaning Q4’s service revenue is based on Q3’s payment volume.

For fiscal 2025, Visa’s total payment volume was approximately $14 trillion. That number has grown steadily as cash usage declines and more transactions shift to digital payments worldwide.

Data Processing Revenue: $20.0 billion (grew 13% year over year)

This is where Visa is paid for processing transactions through VisaNet, including authorization, clearing, and settlement. The key driver is processed transactions. In fiscal 2025, Visa processed 257.5 billion transactions, a 10% increase over the prior year. That works out to roughly 705 million transactions per day.

Data processing is now Visa’s largest revenue stream, and it has been growing faster than service revenue. Part of this reflects pricing actions, but it also reflects the rising transaction count as consumers make more frequent, smaller electronic payments (think contactless tap-to-pay at vending machines, parking meters, and transit systems).

International Transaction Revenue: $14.2 billion (grew 12% year over year)

Every time you use your Visa card in a foreign country or buy something online from a merchant in another currency, Visa collects a fee for handling the cross-border complexity and currency conversion. The driver here is cross-border volume, which excludes transactions within Europe.

This is Visa’s highest-margin revenue stream and one of its most powerful growth levers. Cross-border volume grew 13% on a constant-dollar basis in fiscal 2025, fueled by the continued recovery and growth in international travel and e-commerce. Cross-border e-commerce alone grew 13% in Q4 2025 and now makes up roughly 40% of total cross-border volume.

Other Revenue: $4.1 billion (grew 27% year over year)

This catch-all category includes licensing fees, account holder services, and portions of Visa’s rapidly growing Value-Added Services (VAS) business. VAS revenue (which is spread across data processing and other revenue) reached approximately $9 billion in fiscal 2025, growing 23% on a constant-dollar basis. These services include fraud prevention tools, consulting, analytics, issuing solutions, and acceptance solutions.

This is not the 2015 Visa. The company has been deliberately building a software and services layer on top of its payment rails, and it is now a meaningful growth engine.

The Hidden Line: Client Incentives

Here’s something most casual investors miss. Visa reports gross revenue from the four streams above and then subtracts a significant contra-revenue line item called Client Incentives. These are payments Visa makes to financial institutions and merchants to win and retain their business, encourage them to issue more Visa-branded products, and steer transaction routing through Visa’s network.

In fiscal 2025, client incentives totaled $15.8 billion, up 14% year over year. That means Visa’s gross revenue was roughly $55.8 billion, but after paying incentives, net revenue was $40.0 billion.

Client incentives have grown faster than revenue in recent years, indicating that the competitive landscape is intensifying. Banks and merchants hold leverage, and Visa must pay to keep them in the network. As an investor, you should monitor the ratio of client incentives to gross revenue over time. If that ratio continues to climb, it could pressure margins.

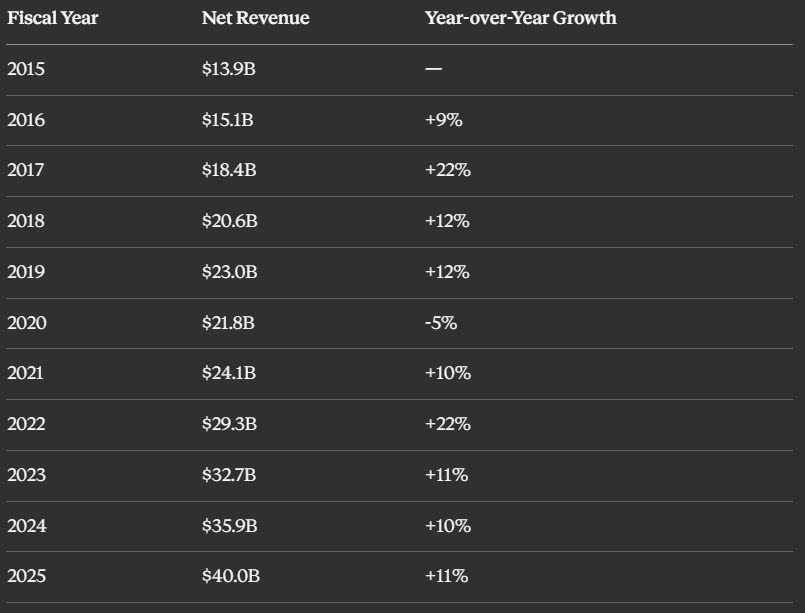

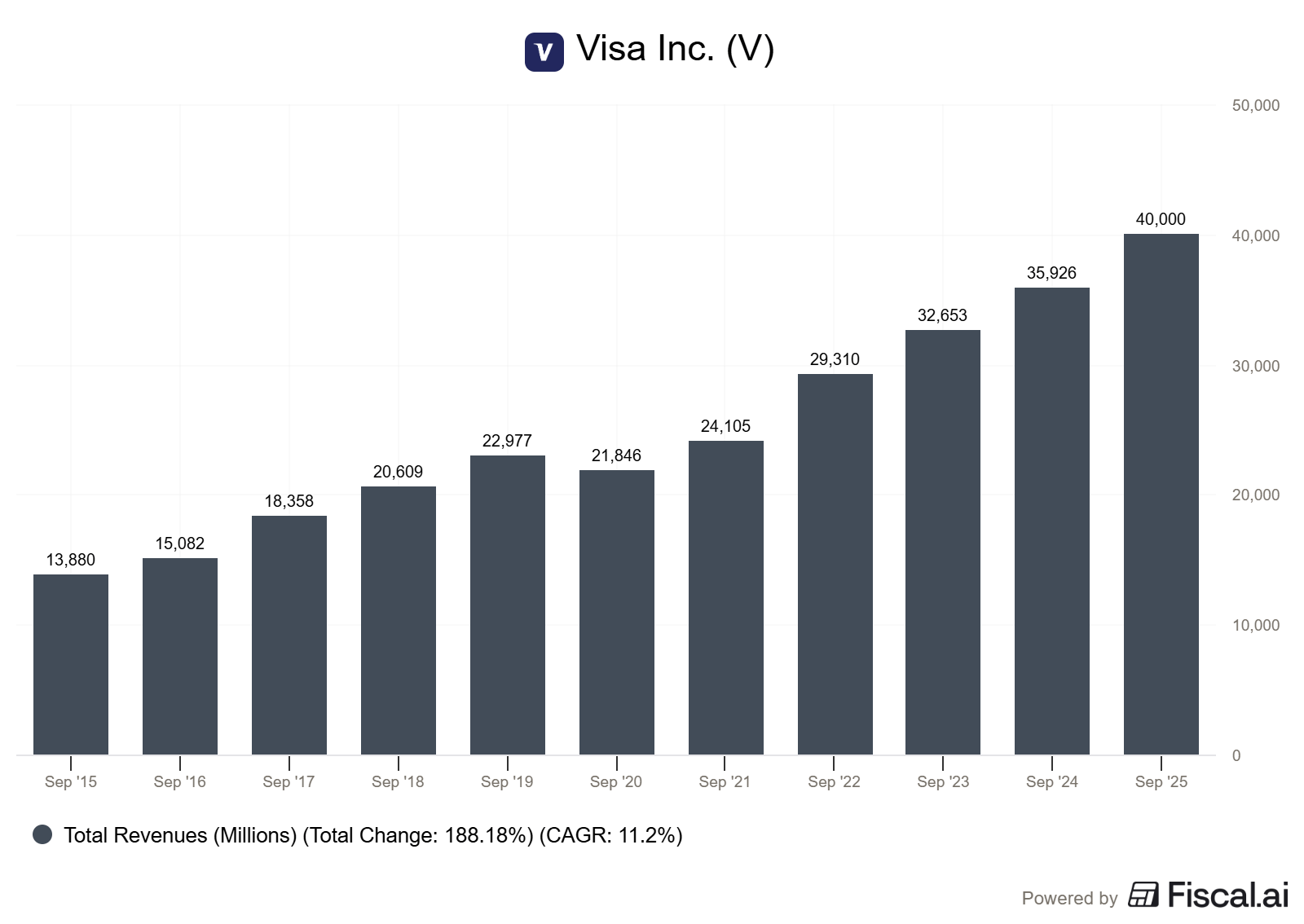

A Decade of Growth: FY2015 to FY2025

Here is where the story gets compelling for long-term investors. Let’s look at how Visa’s net revenue has grown over the past decade:

Sources: Visa Inc. annual earnings releases and 10-K filings on sec.gov. Visa’s fiscal year ends September 30. Revenue figures are rounded.

From $13.9 billion to $40.0 billion in a decade. That is a compound annual growth rate of approximately 11.2%. Three things stand out in this chart:

The Visa Europe inflection (FY2016-2017). Visa completed its acquisition of Visa Europe in June 2016 for approximately $23.4 billion. This reunited the global Visa network under one entity (the two had been separated since Visa’s IPO in 2008). The acquisition added roughly 500 million card accounts, over 3,000 European issuing banks, and more than €1.5 trillion in payments volume. The full impact shows up in FY2017’s 22% revenue jump. This was transformative. Before the deal, Visa Europe operated as a bank-owned cooperative and was far less commercially oriented. At the time, Visa Inc. generated roughly 33 basis points of yield on payment volume, while Visa Europe generated only about 9 basis points. The margin opportunity was enormous.

The COVID dip (FY2020). Visa’s only revenue decline in the decade came in fiscal 2020, when the pandemic crushed cross-border travel. International transaction revenue took the hardest hit. But this revealed something important about the business model: while travel ground to a halt, domestic payments volume held up remarkably well as consumers shifted spending online. The dip was shallow (just 5%), and the recovery was swift.

The post-COVID acceleration (FY2022). Revenue surged 22% as cross-border travel roared back. This was the mirror image of the COVID dip, demonstrating that international travel is a powerful revenue accelerator for Visa. It also showed that the pandemic permanently accelerated the adoption of digital payments, creating a stronger base for growth.

Knowing the concepts is one thing. Being able to sit down with a real dividend stock and actually analyze it is another. Paid membership gives you the tools to bridge that gap:

📊 1. Stock Analysis Infographic Library: 180+ visual references covering financial statements, valuation multiples, and dividend metrics, your cheat sheet for analyzing any company

🤖 2. AI Prompt Library: 10 purpose-built prompts that turn AI into a research partner, stress-test your thesis, dig into financials faster, and catch risks you’d otherwise miss

🔧 3. Investing Tools Suite: 4 analytical tools that take the friction out of the numbers so you can focus on understanding the business, not wrestling with spreadsheets

🎓 4. Skill Workshop: Practical working sessions walking through real company analysis start to finish, not theory, not lectures, actual practice

📈 5. Dividend Analysis Course (Coming Soon): A complete step-by-step course on analyzing dividend stocks using Buffett-inspired fundamental analysis

🔓 6. Everything Added Going Forward: Every new resource, tool, and prompts added automatically, no extra charge, ever

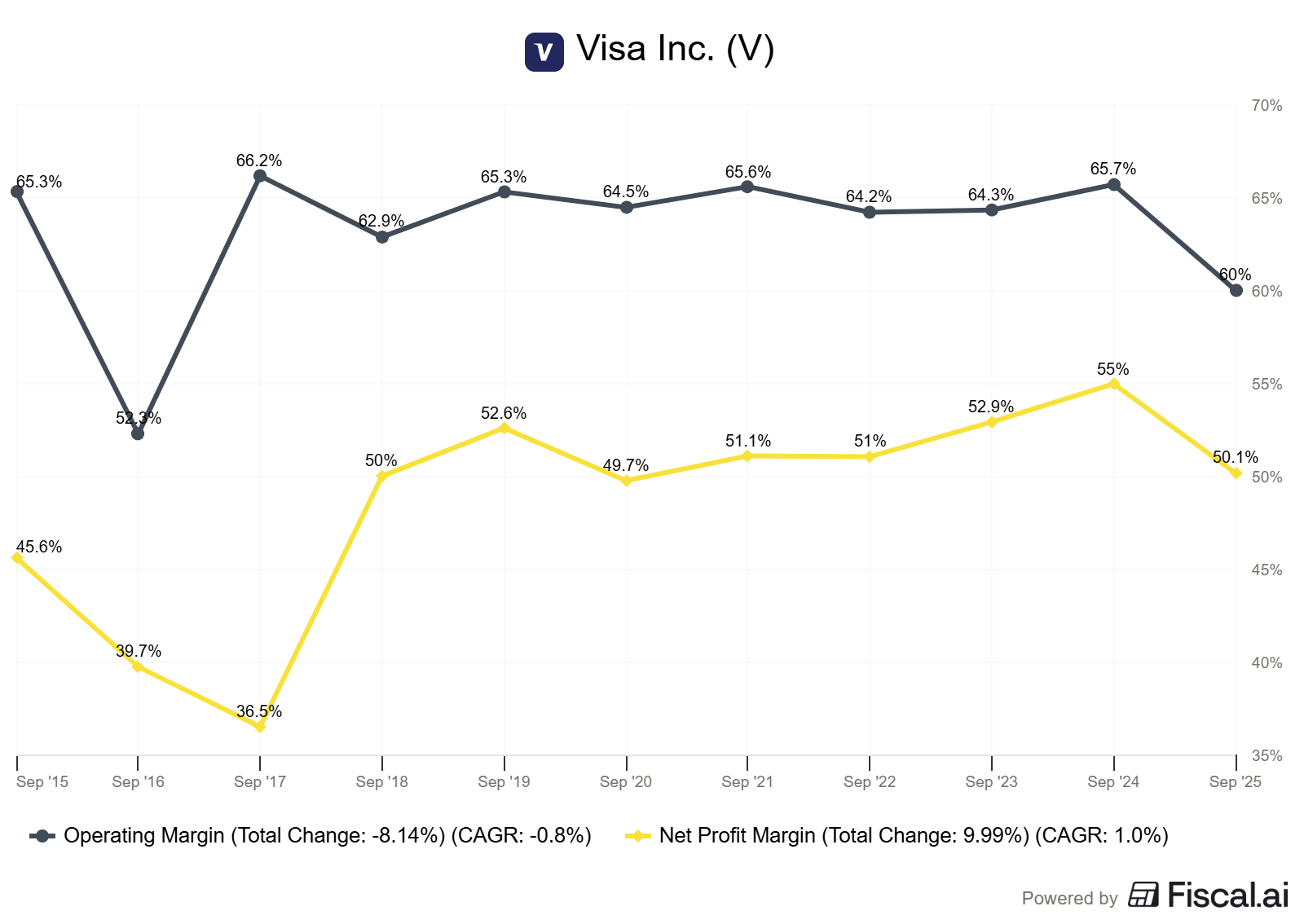

Why the Margins Are Extraordinary

Visa’s operating model produces margins that most businesses can only dream about.

The company’s net profit margin has consistently exceeded 50% in recent years. In fiscal 2025, Visa generated $20.1 billion in GAAP net income on $40.0 billion in net revenue, and non-GAAP net income was $22.5 billion. Operating cash flow was $23.1 billion.

These margins exist because Visa’s cost structure is largely fixed. VisaNet is already built. Processing one more transaction costs Visa almost nothing at the margin. Whether Visa processes 200 billion or 258 billion transactions, the network infrastructure, engineering teams, and brand investments are already in place. Every incremental transaction is nearly pure profit.

This is the power of operating leverage in a network business. As transaction counts and payment volumes grow, revenue scales while costs grow much more slowly. It’s why Visa’s non-GAAP operating expenses grew 11% in fiscal 2025 while revenue also grew 11%, but the company still produced expanding non-GAAP earnings per share (up 14% to $11.47) thanks to share buybacks and other efficiencies.

For context, Visa’s non-GAAP operating margin runs in the high-60% range, and its net margin sits around 50%. Compare that to JPMorgan Chase, the largest U.S. bank, which operates at a net margin of around 30%. The difference? JPMorgan takes credit risk. Visa doesn’t.

Where the Next Decade of Growth Comes From

Visa’s bull case rests on three growth engines that are still in their early innings:

1. The Cash Displacement Opportunity

Even in 2025, cash still accounts for a significant share of global transactions. In developing markets across Asia, Africa, and Latin America, electronic payments are still penetrating rapidly. Visa has 4.6 billion payment credentials globally and operates in more than 200 countries and territories, but the total addressable market continues to expand as more economies digitize.

2. New Payment Flows

Visa’s traditional strength is consumer-to-business (C2B) payments, but the company has been expanding into business-to-business (B2B), person-to-person (P2P), business-to-consumer (B2C), and government-to-consumer (G2C) payments. Commercial payments volume reached $1.8 trillion in fiscal 2025, growing 7% in constant dollars. Visa Direct, the company’s real-time push payment platform, is a key enabler of these new flows.

3. Value-Added Services

This is arguably the most important strategic shift of the last five years. Visa’s VAS business has grown into a roughly $9 billion revenue stream, growing at over 20% annually. These services, which include fraud prevention (powered by AI), consulting, data analytics, issuing solutions, and acceptance solutions, allow Visa to monetize its network far beyond simple transaction processing.

In December 2024, Visa acquired Featurespace, a developer of real-time AI payments protection technology, to further strengthen its fraud prevention capabilities. The company has completed 19 acquisitions in total, many aimed at building out this services layer.

CEO Ryan McInerney described the strategy in the fiscal 2025 earnings call: “As technologies like AI-driven commerce, real-time money movement, tokenization, and stablecoins converge to reshape commerce, our focus on innovation and product development positions Visa to lead this transformation.”

What Investors Get Wrong About Visa

The most common mistake I see is treating Visa like a financial stock. It’s not. Visa has no loan book, no credit losses, and no interest rate sensitivity in the traditional banking sense. It’s a technology and services company that operates in the payments industry.

The second mistake is ignoring client incentives. When you hear Visa’s revenue discussed casually, make sure you know whether the number cited is gross revenue or net revenue. The difference (currently about $15.8 billion annually) is material to valuation.

The third mistake is assuming Visa’s growth has to slow because of its size. Visa’s revenue growth has been remarkably consistent, averaging roughly 10-12% annually (excluding COVID). The combination of cash displacement, new payment flows, value-added services, and geographic expansion gives the company multiple vectors for continued growth, even as the core C2B business matures in developed markets.

How to Use This in Your Investing Process

When evaluating “toll booth” businesses like Visa, here is what to focus on:

Look at the volume and transaction trends rather than just the revenue line. Are payment volumes and processed transactions still growing? Is cross-border volume accelerating or decelerating? These are the fundamental drivers.

Watch the client incentives ratio. If incentives grow persistently faster than gross revenue, the company’s competitive position may be eroding.

Pay attention to the Value-Added Services growth rate. This is where Visa is evolving from a payment network into a payment platform. If VAS growth decelerates sharply, it signals that the diversification strategy is stalling.

Evaluate the operating margin trajectory. A network business should see margins expand (or hold steady) as it scales. Persistent margin compression is a warning sign.

And remember: Visa’s revenue grows with nominal GDP. Inflation, which is bad for most businesses, actually helps Visa because its fees are based on the dollar amount of transactions. When prices go up, so does payment volume, and so does Visa’s revenue. The company doesn’t need to raise prices to grow. It just needs people to keep spending.

The Bottom Line

Visa is not a credit card company. It’s a toll booth on $14 trillion in annual payment volume, collecting a fraction of a percent on each transaction, and converting roughly half of its revenue into pure profit. Over the past decade, it has nearly tripled its net revenue from $13.9 billion to $40.0 billion while maintaining extraordinary margins and generating enormous free cash flow.

The business model is elegant in its simplicity and powerful in its compounding. For investors studying how great businesses create and sustain economic moats, Visa is one of the clearest examples in public markets.

Knowing the concepts is one thing. Being able to sit down with a real dividend stock and actually analyze it is another. Paid membership gives you the tools to bridge that gap:

📊 1. Stock Analysis Infographic Library: 180+ visual references covering financial statements, valuation multiples, and dividend metrics, your cheat sheet for analyzing any company

🤖 2. AI Prompt Library: 10 purpose-built prompts that turn AI into a research partner, stress-test your thesis, dig into financials faster, and catch risks you’d otherwise miss

🔧 3. Investing Tools Suite: 4 analytical tools that take the friction out of the numbers so you can focus on understanding the business, not wrestling with spreadsheets

🎓 4. Skill Workshop: Practical working sessions walking through real company analysis start to finish, not theory, not lectures, actual practice

📈 5. Dividend Analysis Course (Coming Soon): A complete step-by-step course on analyzing dividend stocks using Buffett-inspired fundamental analysis

🔓 6. Everything Added Going Forward: Every new resource, tool, and prompts added automatically, no extra charge, ever

This model is elegant,till EUROPEAN Union, issues it's new Payment System,the model dies in sec.

Great share