How Dividend Distributions Work: A Step-by-Step Guide Using Merck

The four dates that decide whether you actually get paid, walked through with a real Merck dividend.

You see “ex-dividend date” in the news, you check your brokerage account expecting cash, and instead you find a payment scheduled three weeks out. What actually happened between the company’s announcement and the deposit hitting your account?

Most dividend investors collect the check without understanding the machinery behind it. That’s fine until you try to time a purchase around a dividend, get confused by the price drop on the ex-date, or wonder why your “qualified” dividend got taxed as ordinary income.

The dividend distribution process has four specific dates, three parties involved in the transaction, and a few rules that determine whether you actually receive the payment. Once you understand the sequence, you’ll never misread a dividend announcement again.

In today’s post, we will learn:

The Four Critical Dates Every Dividend Investor Must Know

How the Distribution Actually Flows from Company to You

Walking Through a Real Merck Dividend, Start to Finish

What Happens to the Stock Price on the Ex-Date

Common Mistakes Investors Make Around Dividend Dates

Investor Takeaway

Okay, let’s dive in and learn how dividend distributions actually work.

The Four Critical Dates Every Dividend Investor Must Know

Every quarterly dividend involves four specific dates. They always happen in the same order, and missing the distinction between them is the single most common mistake new dividend investors make.

Declaration Date

This is the day the Board of Directors formally announces the dividend. The board votes, the company files an 8-K with the SEC, and a press release goes out. The declaration creates a legal liability on the company’s balance sheet. Until the board declares a dividend, no dividend exists, no matter how reliably the company has paid in the past.

Record Date

This is the cutoff. Whoever the company’s transfer agent has on its books as a shareholder at the close of business on the record date receives the dividend. Anyone who buys after the record date gets nothing this quarter.

Ex-Dividend Date

Here’s where investors get tripped up. Because U.S. stock trades settle on a T+1 basis (one business day after the trade), the ex-dividend date is set as the same day as the record date under current SEC rules. To receive the dividend, you must own the stock before the ex-date. Buy on the ex-date, and the seller keeps the dividend.

Payment Date

The day the cash actually moves. Your brokerage receives the funds from the company’s transfer agent and credits your account, usually the same day or the next day.

The sequence matters: Declare → Ex-Date/Record Date → Pay. Typically, two to three weeks separate the declaration from the ex-date, and another two to four weeks separate the ex-date from payment.

How the Distribution Actually Flows from Company to You

The cash doesn’t move directly from the company’s bank account to yours. There’s a chain of intermediaries, and understanding it explains why dividends sometimes hit accounts at different times for different investors.

The flow looks like this:

Company → Transfer Agent. The company wires the total dividend amount (shares outstanding × dividend per share) to its transfer agent. For Merck, that’s EQ Shareowner Services.

Transfer Agent → DTC (Depository Trust Company). Most shares aren’t held directly by individual investors. They’re held in “street name” by brokerages, which in turn use DTC as the central custodian. The transfer agent sends DTC the dividend share owed to all street-name holders.

DTC → Your Brokerage. DTC allocates cash among brokerages based on the number of shares each brokerage held on the record date.

Your Brokerage → You. Schwab, Fidelity, or whoever holds your account credits the dividend to your cash balance.

This is why two investors who both “own Merck” can see the dividend hit their accounts hours apart. The company paid on time. The brokerage processing speed is what differs.

Most investors collect dividends without understanding them. The ones who become real analysts go further. They learn the mechanics, then build the frameworks to evaluate which dividends are worth owning in the first place. That's what the paid School of Investing membership is built for.

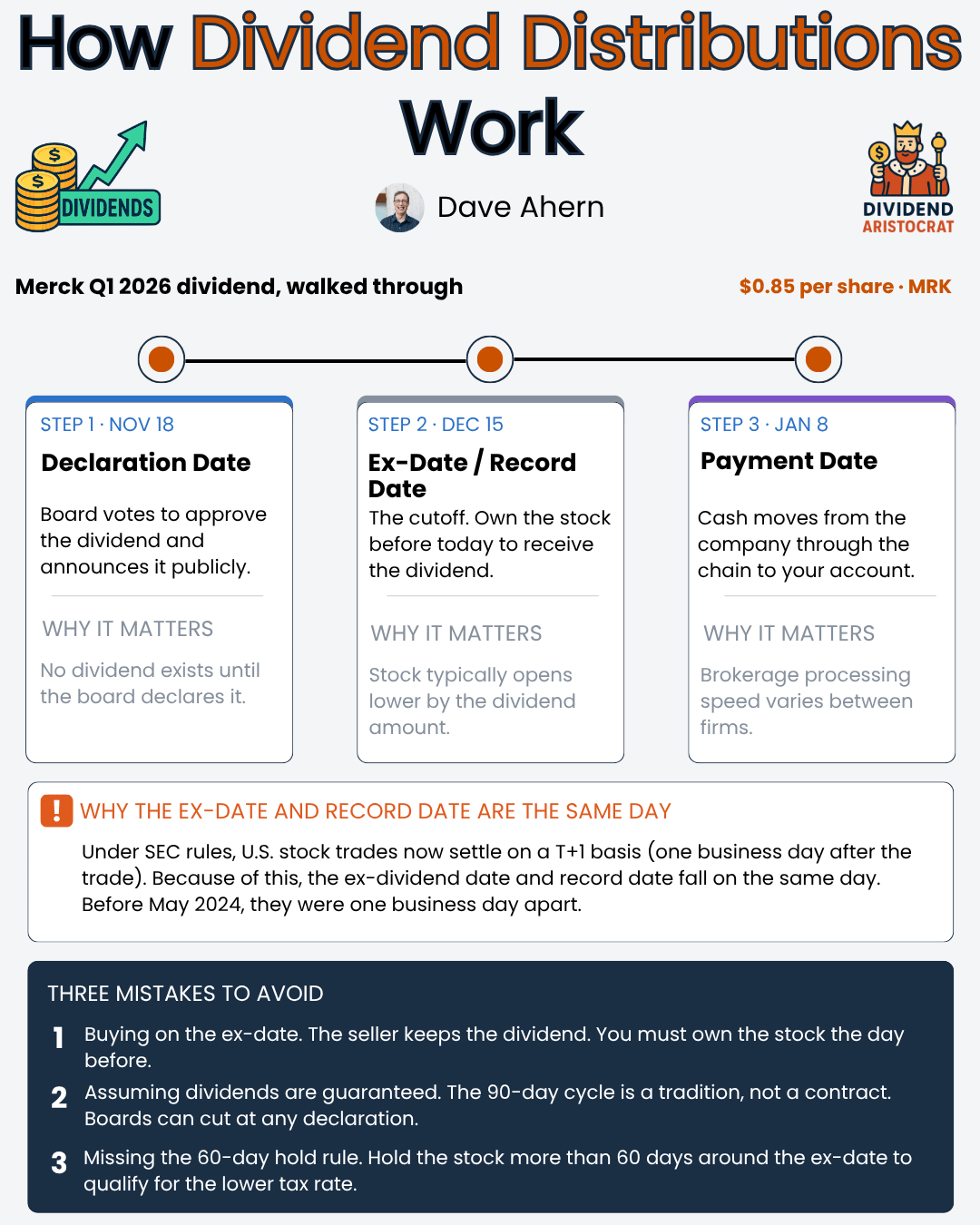

Walking Through a Real Merck Dividend, Start to Finish

Let’s trace an actual Merck dividend from board declaration to your account. I’ll use the Q1 2026 dividend because it’s the most recent as of this writing.

Declaration Date: November 18, 2025 Merck’s Board of Directors declared a quarterly dividend of $0.85 per share, an increase from the prior $0.81 quarterly rate. The increase was announced via press release and filed with the SEC.

Record Date: December 15, 2025. To receive this dividend, you needed to be a shareholder of record at the close of business on December 15, 2025.

Ex-Dividend Date: December 15, 2025. You needed to have purchased Merck shares no later than December 12, 2025 (the last trading day before the ex-date) to receive this payment. Buy on or after December 15, and the prior owner keeps the $0.85.

Payment Date: January 8, 2026. The cash hit shareholder accounts. For an investor holding 100 shares, that’s $85.00 deposited.

Notice the gap: roughly seven weeks from declaration to payment. This is typical for Merck and most large-cap dividend payers.

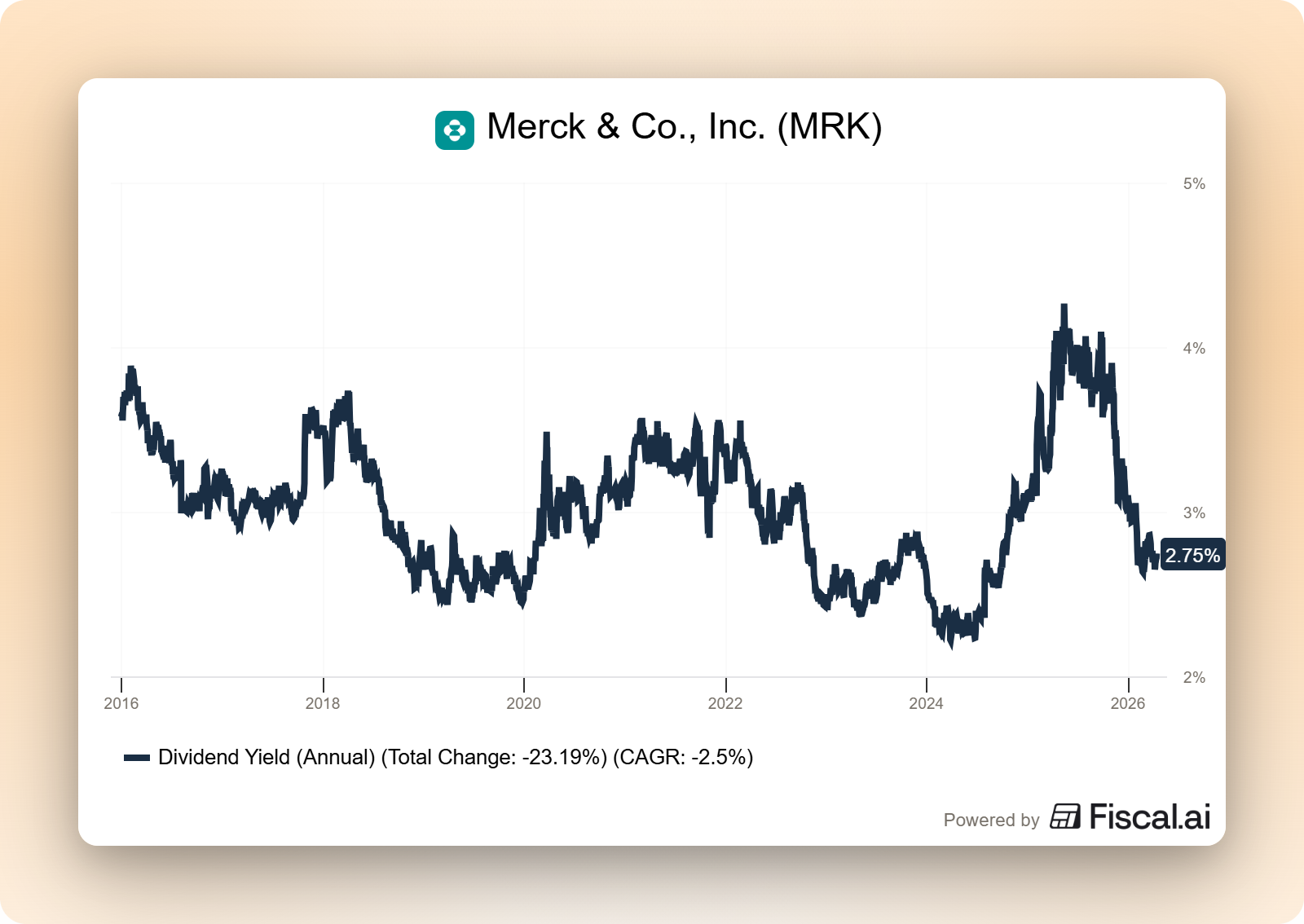

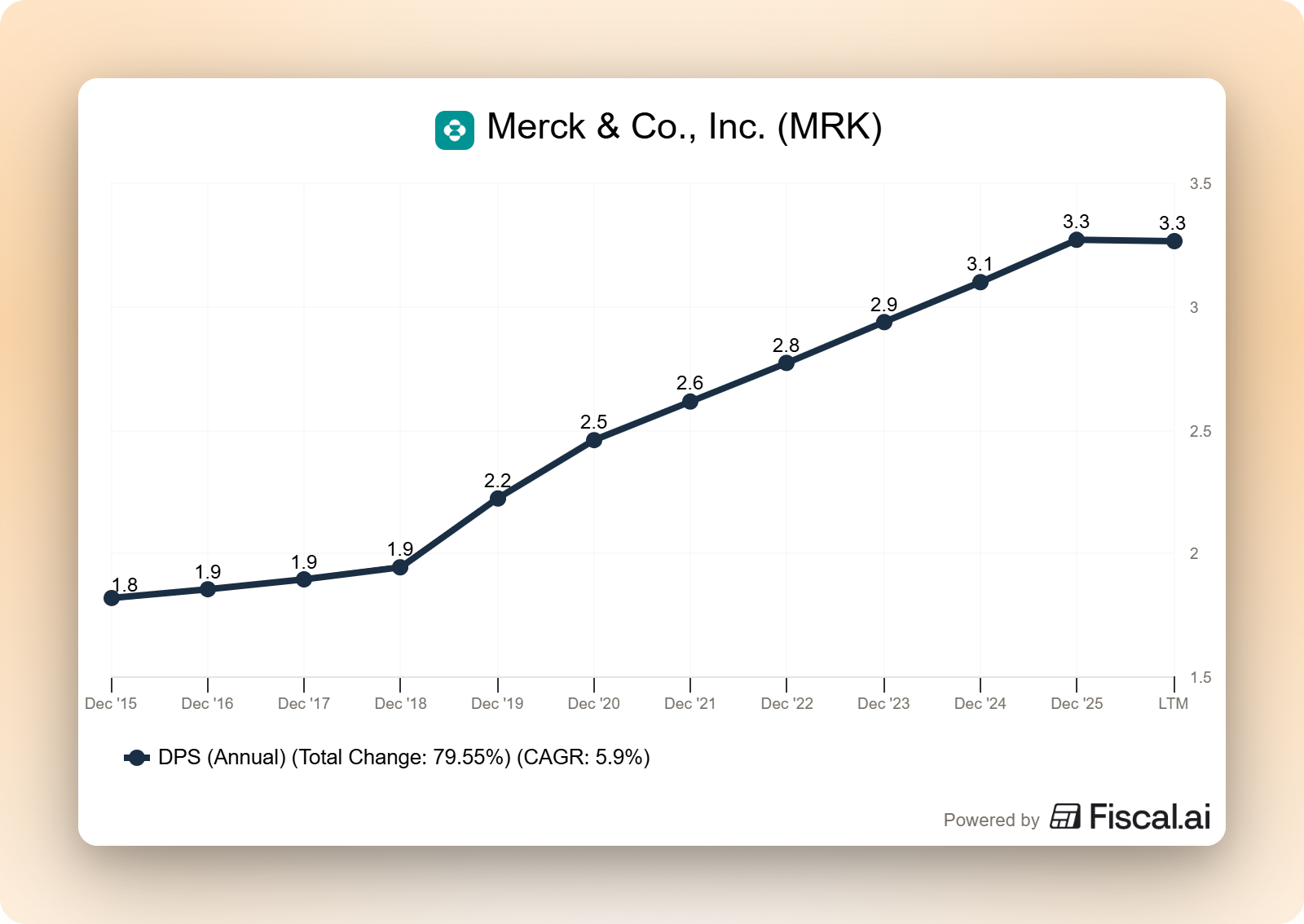

Now let’s zoom out and look at Merck’s full-year picture to understand what this process produces in aggregate. According to Merck’s 2024 10-K filed with the SEC, the company returned $9.1 billion to shareholders in 2024, with $7.8 billion of that coming through dividends. The board raised the quarterly rate from $0.77 to $0.81 in November 2024, then to $0.85 in November 2025. That’s two consecutive November increases, which tells you when Merck typically reviews its dividend policy.

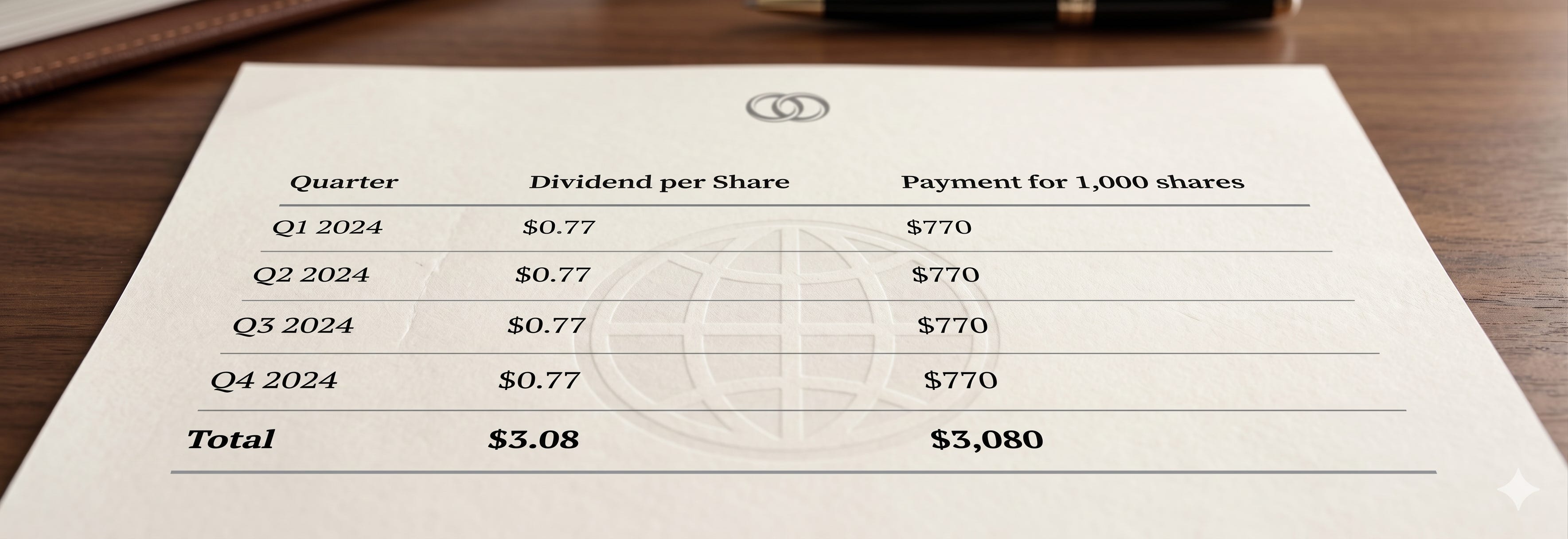

For an investor holding 1,000 shares of Merck across 2024, the dividend math looked like this:

That $3,080 is recurring income, paid in four installments, with each installment requiring you to own the shares before the relevant ex-date.

What Happens to the Stock Price on the Ex-Date

This is the part that confuses new investors most. On the ex-dividend date, the stock price typically drops by approximately the dividend amount at the open.

Why? Because the company is about to send cash out the door. A buyer on the ex-date is buying a slightly less valuable company (less cash on the balance sheet) and isn’t entitled to the upcoming dividend. The market prices that in immediately.

If Merck closes at $100.00 the day before the ex-date and pays an $0.85 dividend, you can expect the stock to open around $99.15 on the ex-date, all else equal. Of course, “all else equal” rarely holds in practice. Broader market moves, news, and earnings can swamp the dividend adjustment in either direction.

The practical implication: there is no “free lunch” in buying right before the ex-date to capture the dividend. You received the $0.85, but you also bought a stock that immediately trades $0.85 lower. Tax treatment can actually make this strategy a net loser if the dividend gets taxed at ordinary income rates while the price drop creates no offsetting tax benefit until you sell.

Common Mistakes Investors Make Around Dividend Dates

Three errors come up over and over.

Confusing the ex-date with the record date when buying. Investors see “record date: June 16” and assume buying on June 16 qualifies them. It does not. The ex-date is what matters for new buyers. Always look for the ex-dividend date, not the record date.

Assuming declared dividends are guaranteed forever. A board can cut, suspend, or eliminate a dividend at any future declaration. The 90-day cycle is a tradition, not a contract. Companies like General Electric and AT&T have demonstrated this painfully in recent years. The fact that Merck has paid reliably for decades reflects management discipline and cash generation, not a legal obligation.

Misunderstanding qualified vs. ordinary dividend tax treatment. To receive qualified dividend treatment (taxed at the lower long-term capital gains rate), you generally must hold the stock for more than 60 days during the 121-day period beginning 60 days before the ex-dividend date. Buy a stock the week before the ex-date, collect the dividend, sell two weeks later, and you’ll likely owe ordinary income tax on that dividend. This wipes out a big chunk of the after-tax yield.

Investor Takeaway

The dividend distribution process isn’t complicated once you’ve seen it laid out. A board declares. A record date establishes who gets paid. An ex-date determines who can still buy in. A payment date moves the cash. The same four-step sequence runs on every U.S. dividend stock you’ll ever own.

Investors create problems for themselves in the small details: buying on the wrong side of the ex-date, assuming a declared dividend is permanent, or violating the qualified dividend holding period and surrendering the tax advantage.

Merck’s pattern is a useful template to memorize. Declarations roughly two months ahead of payment, ex-dates and record dates aligned, payments on the 7th or 8th of the month following each quarter-end. Once you’ve watched one full cycle, you’ve watched them all.

That is going to wrap up our discussion for today.

As always, thank you for taking the time to read this post, and I hope you find something of value on your investing journey.

If I can further assist, please don’t hesitate to reach out.

Until next time, take care and be safe out there,

Dave

Want to go from collecting dividends to actually understanding them?

The free posts give you the foundation. Paid subscribers get the full analyst toolkit: the dividend screening framework I use to find quality payers, the valuation calculators to know what they’re worth, the infographic library you can save and reference, and AI prompts that turn 10-K reading from a chore into a 20-minute process.

The goal isn’t to give you stock tips. It’s to make you the kind of investor who doesn’t need them.

n