Dividends vs. Buybacks: What They Mean for Your Returns

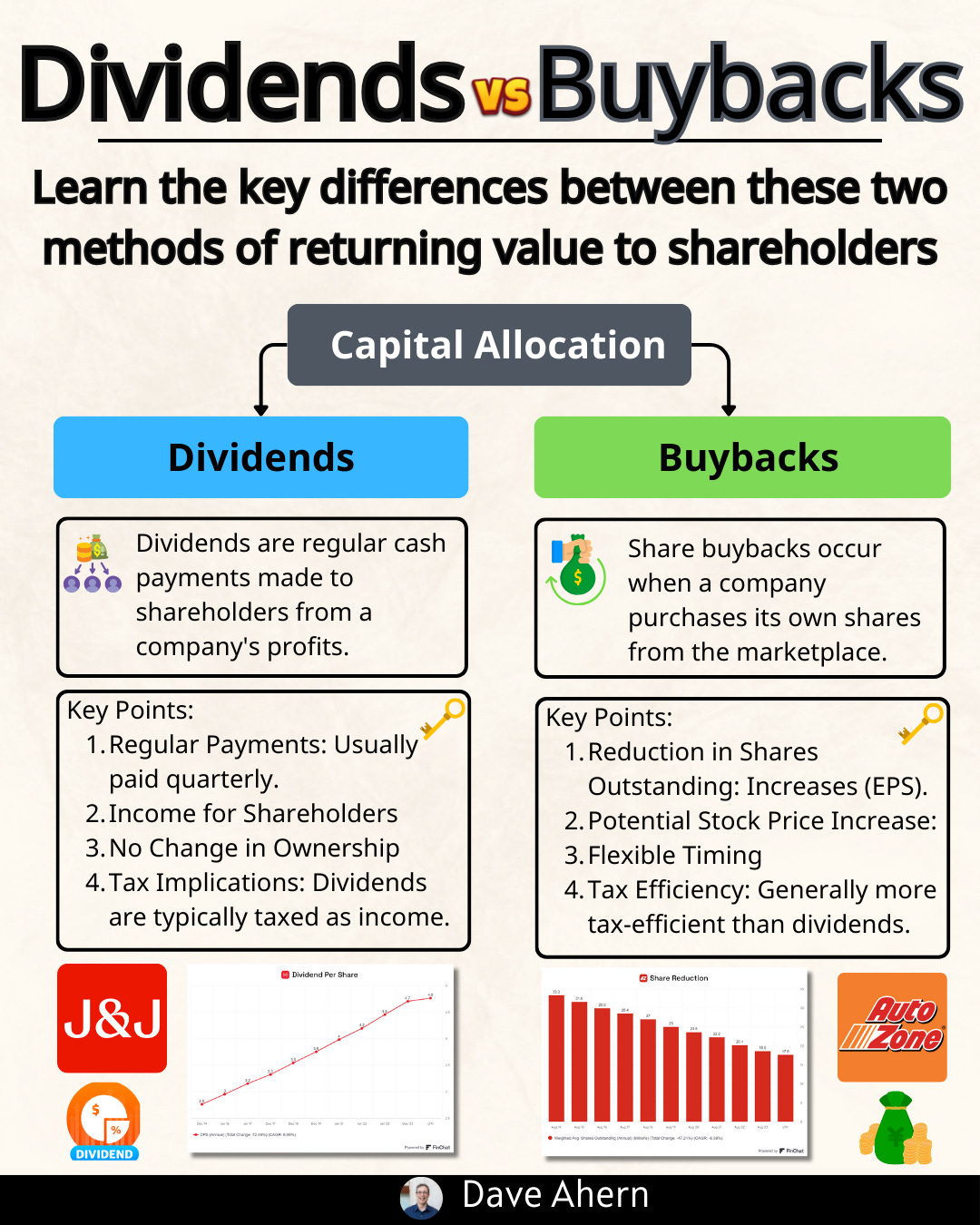

Companies return cash to shareholders in two main ways: dividends and share buybacks. Both can build wealth. Both can also destroy it if used poorly. If your goal is total return, you need to know what each tool does, when it works, and how to judge quality.

Note: This is education, not tax or investment advice. U.S.-specific tax notes below.

What is a dividend?

A dividend is a cash payment per share. If you own the stock on the record date, you get paid. Many firms pay quarterly. Some also issue “special” one-time dividends when cash piles up.

Pros

Cash now: Reliable income without selling shares.

Discipline: A regular payout can curb wasted spending.

Reinvestment: DRIPs can compound share count over time.

Signaling: A steady, growing dividend often signals confidence.

Cons

Taxed today: Qualified dividends are generally taxed in the year received.

Less flexible: Cuts are painful and often punished.

May mask weakness: A high yield can signal limited growth or rising risk.

Opportunity cost: Cash paid out can’t fund high-return projects.

When dividends shine

Mature, steady businesses with predictable free cash flow (FCF).

Investors who want an income “floor.”

Firms with prudent payout ratios and consistent dividend growth.

What to check

Payout ratio: Dividend as a share of earnings or FCF. Lower is safer.

Balance sheet: Net cash or modest leverage supports the payout.

Growth record: A long, steady raise streak beats a high, fragile yield.

What is a share buyback?

A buyback is when a company repurchases its own shares. With fewer shares outstanding, each remaining share owns a larger slice of future earnings and cash flow. EPS often rises even if net income is flat.

Pros

Tax deferral: You don’t owe taxes until you sell, in many cases.

Flexible: Easy to ramp up or pause as conditions change.

Accretive if cheap: Buying below intrinsic value boosts per-share value.

Offsets dilution: Can neutralize stock-based pay over time.

Cons

Price risk: Buying expensively destroys value.

Can mask stagnation: EPS can rise while the core business stalls.

Timing is hard: Firms often buy most near peaks.

Starvation risk: Overdone buybacks can starve R&D or capex.

When buybacks shine

Shares trade below a conservative view of value.

Strong, repeatable FCF and limited better uses of capital.

Management uses a clear price discipline and shrinks share count over years.

What to check

Net buyback yield: Net repurchases divided by market cap.

Share count trend: Is the diluted share count falling over 3–5 years?

SBC coverage: Are repurchases more than offsetting stock comp?

Capital plan: Are buybacks second to high-return reinvestment?

U.S. tax treatment (quick)

Qualified dividends: Generally taxed in the year received at 0%, 15%, or 20% depending on your bracket. The 3.8% NIIT may apply at higher incomes.

Buybacks: No tax event when the company buys shares. You owe capital gains tax only when you sell your stock, based on your basis and holding period.

Corporate buyback tax: A 1% excise tax on net repurchases applies at the company level. Policy can change.

For total return investors, tax deferral can make buybacks more efficient than dividends—if buybacks are done at sensible prices.

How they impact returns: simple, concrete examples

Example A: Dividend compounding

You own 100 shares at $100.

Dividend yield is 3% ($3 per share).

You receive $300 in year one. If you reinvest at $100, you buy 3 more shares (now 103).

If the dividend grows 6% a year and the price later reflects that growth, your total return becomes dividend income + price appreciation. Reinvesting accelerates your share count and future income.

What helps:

Safe payout ratio (often FCF payout < 60%, varies by sector).

Consistent dividend growth above inflation.

Healthy ROIC and balance sheet.

Example B: Buyback-driven EPS lift

Company earns $10 billion. Market cap is $250 billion. It buys back 4% of shares net this year.

If net income is flat next year, but the share count is 4% lower, EPS rises ~4%.

If the market keeps the same P/E, price can follow EPS higher. Your ownership percentage rises without you doing anything.

What helps:

Repurchases below intrinsic value.

Multi-year net share reduction, not just offsetting dilution.

Durable FCF to fund buybacks without stretching the balance sheet.

Hybrid framing for total return

“Owner yield” = dividend yield + net buyback yield.

A firm with 1% dividend yield and 3% net buyback yield delivers ~4% owner yield before growth. Add sustainable earnings growth of, say, 6%, and your rough, long-run return could be ~10% if the valuation doesn’t change. Reality varies, but this is a useful lens.

Short case study: Apple and Costco (U.S.)

Apple: Buybacks as a compounding engine

Reality: Over the past decade, Apple reduced its diluted share count by roughly 40%+, while also paying and growing a modest dividend.

Mechanics: Large, steady FCF funds both investment and cash returns. In several periods, EPS grew faster than net income thanks to repurchases.

Why it worked: Strong FCF, sensible balance sheet, and a long runway to return excess cash. Repurchases were meaningful relative to share count, not just offsetting SBC.

Total return lens: For a long-term holder, net buyback yield + dividend yield + earnings growth drove returns. Tax on buybacks was deferred until the investor sold.

Costco: Regular dividends plus occasional big specials

Reality: Costco pays a modest regular dividend and, at times, large special dividends (e.g., a $15 per-share special announced in late 2023).

Investor math: Owning 100 shares meant $1,500 in cash from that special alone, on top of regular dividends. That is a real boost to total return in that year.

Why it worked: A discipline of “scale economies shared” keeps customers loyal and cash flows steady. When cash builds beyond needs, Costco returns it without committing to a higher ongoing payout.

Total return lens: Regular dividend growth supports income compounding. Specials deliver lump-sum returns when cash is flush. Taxes apply in the year paid, which income-focused holders often accept.

Cautionary note: Buybacks done badly

Some firms have spent heavily near peaks or used debt to fund repurchases while the core business deteriorated. EPS rose for a while, but value did not. Lesson: Buybacks are an amplifier. They make a good business better and a weak plan worse.

How to judge a payout plan for total return

Start with FCF: Are dividends + buybacks covered by free cash flow across a cycle?

Prioritize reinvestment: High-ROIC projects come first. Payouts are what’s left.

Track share count: Look for a steady decline in diluted shares over 3–5 years.

Test dividend safety: Check FCF payout, leverage, and the firm’s raise streak.

Demand price discipline: Repurchase activity should lean heavier when shares are cheap, lighter when expensive.

Align with your goals: If you value tax deferral and compounding, lean toward quality buyback programs. If you need cash today, a safe, growing dividend may fit better.

Pros and cons at a glance

Dividends

Pros: Cash now. Simple. Can enforce capital discipline. Reinvestment optional through DRIPs.

Cons: Taxed now. Less flexible. High yields can be a trap.

Buybacks

Pros: Tax deferral. Flexible. Accretive when done below value. Offsets dilution.

Cons: Prone to poor timing. Can mask weak fundamentals. May crowd out good investment if misused.

Bottom line

Dividends and buybacks are tools, not strategies. Great outcomes come from great businesses that produce surplus cash, reinvest well, and return the rest with discipline. For total return, think in terms of owner yield plus sustainable growth, adjusted for valuation and taxes. Favor companies that:

Grow FCF,

Keep balance sheets sound,

Return cash in ways that are flexible, value-aware, and consistent over time.

As a dividend growth investor, I appreciate this article! Curious on your view of stock buybacks though when it comes to the framing of my publication below.

https://divistockchronicles.substack.com/p/stock-buybacks-confidence-or-financial

The Apple case study perfectly illustrates buybacks done right. 40% share count reduction over a decade while growing the business - that's how you compound wealth. Most companies just use buybacks to offset dilution and call it shareholder-friendly.