Dividend Yield: What It Really Tells You (And What It Doesn’t)

A stock’s dividend yield just jumped to 8%. Time to buy?

Not so fast. That high yield might be a golden opportunity, or a flashing warning sign that the dividend is about to be slashed. The difference between those two outcomes comes down to understanding what dividend yield actually measures, how it moves, and where it can mislead you.

Dividend yield is one of the most widely quoted metrics in investing. It is also one of the most misunderstood. Too many investors treat it like a shopping discount: the higher the number, the better the deal. That thinking has destroyed more wealth than almost any other mistake in dividend investing.

In today’s post, we will learn:

What Dividend Yield Is and How to Calculate It

Trailing Yield vs. Forward Yield (And Why the Difference Matters)

The Inverse Relationship: Why Yield Rises When Price Falls

What Dividend Yield Actually Tells You

What Dividend Yield Cannot Tell You

A Practical Framework for Using Yield in Your Process

Okay, let’s dive in and learn more about what dividend yield really means for your portfolio.

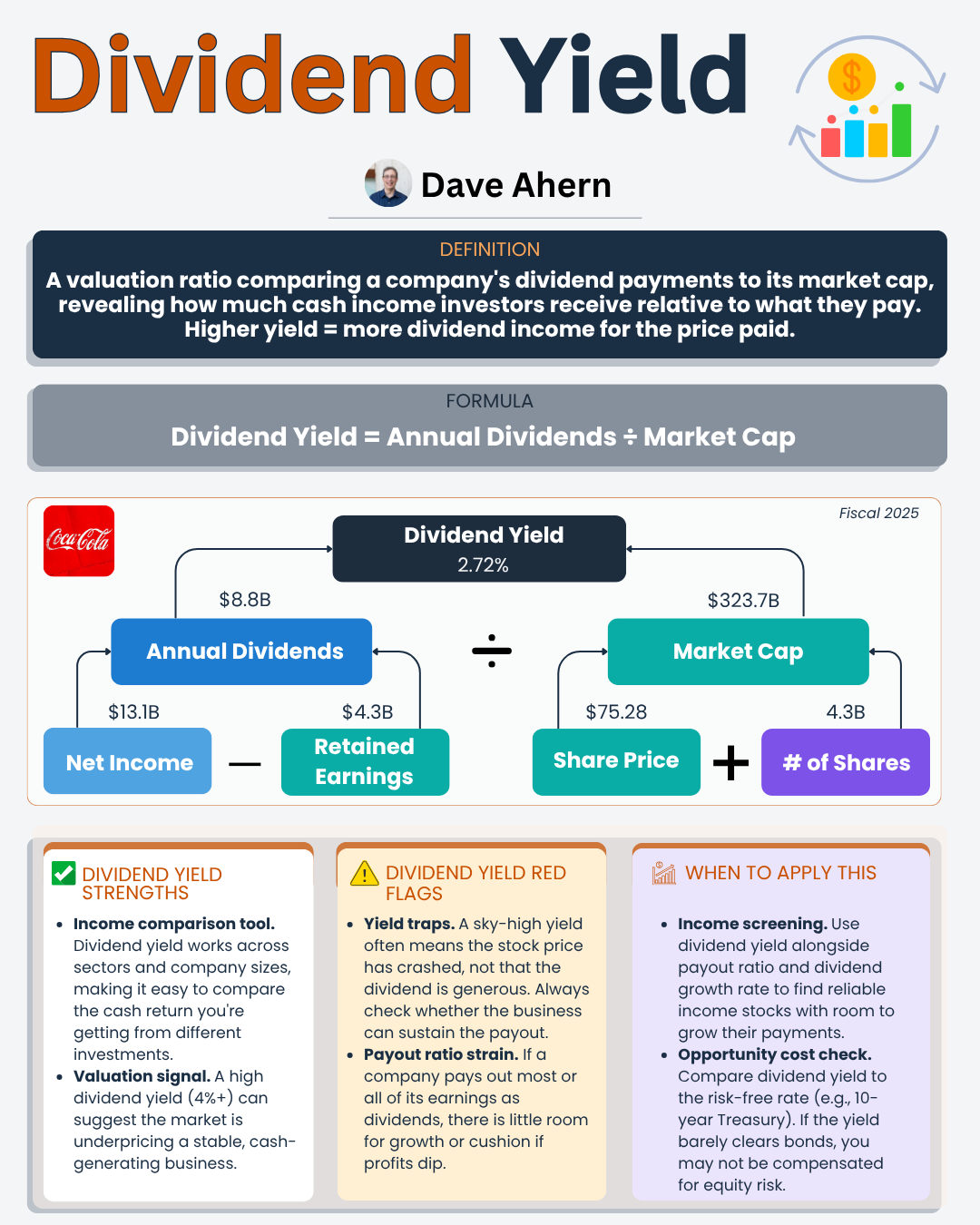

What Dividend Yield Is and How to Calculate It

Dividend yield measures how much income a stock pays relative to its price. Think of it as the “interest rate” on your stock investment, though the comparison is imperfect (more on that shortly).

The formula is straightforward:

Dividend Yield = Annual Dividend Per Share / Stock Price

Let’s use Coca-Cola (KO) as our example. According to SEC filings, Coca-Cola declared a quarterly dividend of $0.53 per share in early 2026, which translates to an annual dividend of $2.12 per share. With the stock trading around $74, the math looks like this:

Dividend Yield = $2.12 / $74.00 = 2.86%

That 2.86% tells you that for every $100 you invest in Coca-Cola at $74 per share, you would receive approximately $2.86 in annual dividend income.

Simple enough. But here is where it gets interesting, and where most investors stop paying attention too soon.

Notice that the formula has two moving parts: the dividend (numerator) and the stock price (denominator). Both change over time, and both change for different reasons. That creates a dynamic number that can shift in meaning depending on which variable is moving.

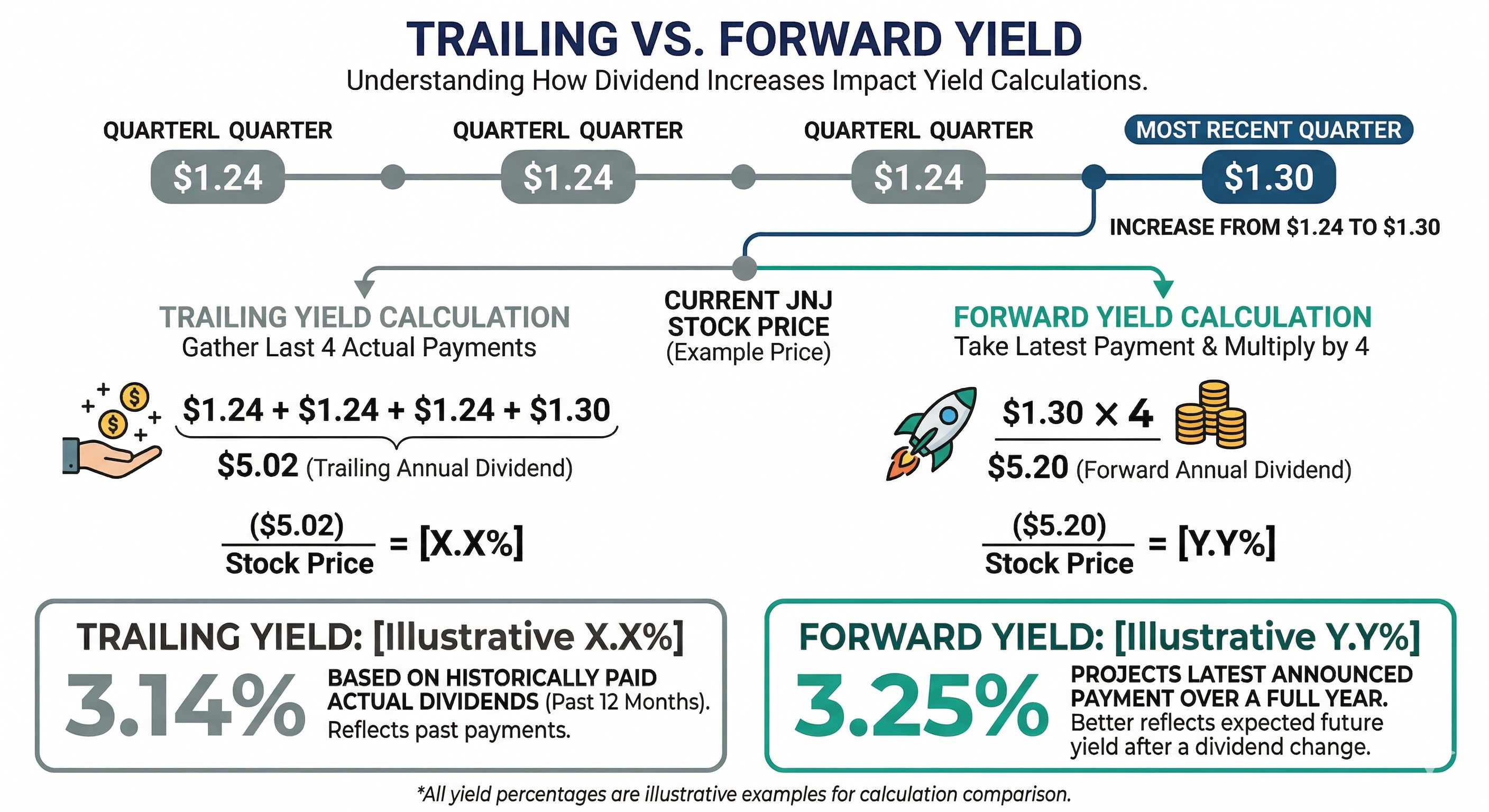

Trailing Yield vs. Forward Yield

When someone quotes a stock’s dividend yield, they could mean two different things. Understanding which version you are looking at matters more than most investors realize.

Trailing Dividend Yield uses the dividends the company has already paid over the past twelve months. This is backward-looking. You are dividing the sum of the last four quarterly payments by the current stock price.

Forward Dividend Yield takes the most recently declared quarterly dividend, multiplies it by 4 (assuming quarterly payments), and divides the result by the current stock price. This is forward-looking and assumes the company will maintain that payment level.

The distinction matters most when a company has recently changed its dividend.

Consider Johnson & Johnson (JNJ). In April 2025, the company announced a 4.8% increase in its quarterly dividend from $1.24 to $1.30 per share, marking 63 consecutive years of annual dividend increases (per an SEC Form 8-K filed in April 2025).

Immediately after that announcement, the trailing yield still reflected three quarters at $1.24 plus one quarter at $1.30. The forward yield jumped to reflect $5.20 annualized ($1.30 x 4). For a few months, the trailing and forward yields told different stories about the same stock.

Now consider the opposite scenario. When AT&T slashed its quarterly dividend from $0.52 to $0.2775 per share in early 2022 (a cut of approximately 47%), the trailing yield temporarily looked much higher than the forward yield because it still included quarters paid at the old, higher rate. An investor screening for high trailing yield would have found AT&T looking attractive at exactly the wrong moment.

The practical takeaway: forward yield is generally more useful because it reflects the current payment level. But forward yield assumes the company will maintain the dividend, which brings us to the most important concept in dividend yield analysis.

The Inverse Relationship: Why Yield Rises When Price Falls

This is the concept that separates informed dividend investors from those who walk into yield traps.

Because the stock price sits in the denominator of the yield formula, there is a direct mathematical relationship: when the stock price drops, the yield rises. When the price rises, the yield falls. They move in opposite directions.

Let’s make this concrete.

Imagine a company paying $2.00 per share in annual dividends:

At $50 per share: Yield = $2.00 / $50.00 = 4.0%

At $40 per share: Yield = $2.00 / $40.00 = 5.0%

At $25 per share: Yield = $2.00 / $25.00 = 8.0%

The dividend hasn’t changed. The yield doubled. And it doubled for the worst possible reason: the stock price collapsed.

This is exactly what happened with Walgreens Boots Alliance (WBA). The company had raised its dividend for 47 consecutive years and was on the verge of becoming a Dividend King (50+ years of consecutive increases). But the stock price cratered, falling from roughly $96 per share in 2015 to below $10 per share by late 2024. As the share price plummeted, the yield soared above 10%.

Investors who chased that 10% yield got burned. In January 2024, Walgreens cut its quarterly dividend by 48%, from $0.48 to $0.25 per share. Then, in early 2025, the company suspended the dividend entirely. The yield went from 10% to 0%.

Here is the lesson: a rising yield caused by a falling stock price is not a gift. It is a question. The question is whether the business can sustain the dividend. Sometimes the answer is yes, and you have found a genuine bargain. Other times, the market is telling you something the dividend hasn’t caught up to yet.

Conversely, a stock with a declining yield might be a sign of strength. If Johnson & Johnson’s stock price rises from $150 to $200 while the dividend grows from $4.76 to $5.20, the yield will drop despite the company paying you more money. That is a good problem to have.

What Dividend Yield Actually Tells You

Yield is not useless. It provides several useful pieces of information once you understand its limits.

1. Your income rate at the current price.

This is the most straightforward use. If you buy 100 shares of Coca-Cola at $74 and the company pays $2.12 per year, you will collect $212 annually (before taxes) on your $7,400 investment. Yield tells you what your cash-on-cash return looks like from dividends alone.

2. A rough comparison tool across similar companies.

If you are choosing between two consumer staples companies with similar growth profiles and balance sheet strength, yield can help you identify which is offering more income per dollar invested at the current price. The keyword here is “similar.” Yield comparisons across different industries or between companies with vastly different risk profiles are misleading.

3. A signal that something may have changed.

When a stock’s yield deviates significantly from its own historical average, that is worth investigating. If a stock typically yields 2.5% to 3.5% and suddenly yields 6%, either the dividend increased dramatically (rare) or the price dropped significantly. Both scenarios deserve a closer look.

4. A starting point for total return expectations.

For mature, stable dividend payers, total return is roughly equal to the dividend yield plus the dividend growth rate. A stock yielding 3% with 5% annual dividend growth has a reasonable shot at delivering 8% total returns over time (before valuation changes). This is not a guarantee, but it is a useful mental model.

What Dividend Yield Cannot Tell You?

Here is where most investors go wrong. They treat yield as a complete answer when it is only part of the question.

1. Yield says nothing about dividend safety.

A 7% yield tells you nothing about whether the company can afford to keep paying. AT&T yielded over 7% before cutting its dividend by 47%. Walgreens yielded over 10% before suspending its dividend entirely. The yield looked generous right up until it vanished.

To assess safety, you need to look at the payout ratio (dividends divided by earnings or free cash flow), the company’s balance sheet, and the trend in underlying business performance. These are the metrics that yield cannot provide.

2. Yield ignores dividend growth.

A stock yielding 1.5% that grows its dividend by 12% annually will generate far more income over a decade than a stock yielding 5% with no growth. But the yield snapshot makes the 5% stock look three times better.

Think of it this way. If you plant two apple trees and one produces five apples today but never grows, while the other produces two apples today but doubles its output every few years, which tree do you want? Yield only counts today’s apples.

3. Yield cannot distinguish between a bargain and a trap.

This is the critical limitation. A stock yielding 6% after dropping 40% could be a wonderful business temporarily on sale. Or it could be a deteriorating business heading toward a dividend cut. Yield alone cannot tell you which. You need to analyze the fundamentals, the balance sheet, and the competitive position to make that determination.

4. Yield comparisons across sectors are misleading.

A utility yielding 4% and a tech company yielding 1% are not comparable on yield alone. Utilities carry more debt, grow more slowly, and distribute more earnings as dividends. Technology companies reinvest more, grow faster, and typically return capital through buybacks. Comparing their yields is like comparing the fuel efficiency of a cargo ship and a bicycle. They serve different purposes.

5. Yield does not account for tax treatment.

REIT dividends are generally taxed as ordinary income. Qualified dividends from most U.S. corporations receive preferential tax rates. A 4% REIT yield and a 3% qualified dividend yield might deliver similar after-tax income depending on your bracket. Yield ignores this distinction entirely.

Understanding a formula is step one. Knowing how to sit down and evaluate any dividend stock yourself, with confidence, is the goal. That's what School of Investing is built to help you do.

A Practical Framework for Using Yield in Your Process

Given the yield’s limitations, how should you actually use it? I think of yield as the first filter, not the final answer. Here is my approach.

Step 1: Compare yield to the company’s own history.

Every stock has a typical yield range. Coca-Cola has historically yielded between roughly 2.5% and 3.5%. Johnson & Johnson has historically yielded between 2% and 3%. When the current yield falls outside that band, it is worth asking why.

If the yield is above the historical range, check whether the price has fallen (investigate the business) or the dividend has increased meaningfully (positive signal). If the yield is below the historical range, the stock may be overvalued, or the market may be pricing in faster growth.

Step 2: Check the payout ratio immediately.

Before you get excited about any yield above 4%, look at the payout ratio. For most non-REIT companies, I want to see a payout ratio below 75% of free cash flow. For REITs, I use Adjusted Funds From Operations (AFFO), and I look for a payout ratio below 85%.

If the payout ratio is above 90%, the dividend is on thin ice. The company has almost no cushion for a bad quarter or an unexpected expense. That high yield might not survive.

Step 3: Look at dividend growth, not just the current payment.

A company that has raised its dividend consistently for 10, 20, or 50 years is telling you something about the durability of its business model. Johnson & Johnson’s 63 consecutive years of increases did not happen by accident. It reflects a business that generates reliable cash flows through economic cycles.

Compare that to a company paying a large static dividend with no growth. The yield might look attractive today, but inflation will erode that purchasing power over time.

Step 4: Ask yourself why the yield is where it is.

This is the most important step. High yield because of a falling price requires you to diagnose the cause. Temporary headwinds (a lawsuit, a bad quarter, sector rotation) in an otherwise strong business can create real opportunities. Structural decline in the business model (think Walgreens competing against Amazon’s pharmacy business) is a fundamentally different situation.

Low yield despite rising prices means the market is pricing in growth. Determine whether that growth is realistic before dismissing the stock as “too expensive.”

Red Flags: When High-Yield Signals Danger

Over the years, I have noticed several patterns that frequently precede dividend cuts. When I see a high yield combined with any of these warning signs, I become extremely cautious.

Yield significantly above sector average. If the average yield in a sector is 3% and one company yields 8%, the market is pricing in the risk you need to understand.

Rising payout ratio. A company that paid out 50% of earnings three years ago but now pays 90% is stretching. That trajectory matters more than the current number alone.

Declining free cash flow. Dividends come from cash. If the cash is shrinking while the dividend stays flat or grows, something has to give.

Increasing debt to fund the dividend. Some companies borrow money to maintain their dividend. This is a red flag. Borrowing to invest in growth can be smart. Borrowing to pay shareholders is a sign of distress.

Management is hedging on dividend commitments. When CEOs say things like “we will evaluate our capital allocation priorities” or “everything is on the table,” they are preparing you for a cut. Pay attention to the language.

Putting It All Together: Two Different 5% Yields

Let me paint two pictures to show why identical yields can mean completely different things.

Company A yields 5%. The yield is above its five-year average of 3.5% because the stock dropped 30% after missing one quarter’s earnings estimate. But the business has 15 years of consecutive dividend increases, a 55% payout ratio, no debt maturities for 3 years, and management reaffirmed the dividend on the earnings call.

Company B yields 5%. The yield is in line with its recent average, which has been climbing because the stock has been declining for three years. The payout ratio has expanded from 60% to 95%, free cash flow is falling, and the CEO recently said the company is “evaluating all capital allocation options.”

Same yield. Completely different situations. Company A looks like a potential opportunity. Company B looks like a yield trap. Only by looking beneath the yield can you tell the difference.

Common Mistakes Investors Make with Dividend Yield

Sort by yield and buy the highest number. This is the most common and most damaging approach. The highest-yielding stocks in any screen are often the most dangerous because their prices have collapsed for fundamental reasons.

Ignoring yield on cost vs. current yield. Your yield on cost (the dividend divided by what you originally paid) is a fun personal metric, but it should not drive decisions. What matters for new money is the current yield and the forward outlook.

Treating yield as guaranteed income. Unlike a bond’s coupon, a stock’s dividend can be cut or eliminated at any time. Walgreens taught that lesson painfully. A company’s board votes on the dividend each quarter. There is no contractual obligation to maintain it.

Anchoring to a past yield. “I’ll buy when the yield hits 4% again” might sound disciplined, but if the company has grown its dividend and the business has improved, the stock might never yield 4% again. Valuation should be based on the business, not on matching a historical yield.

Investor Takeaway

Dividend yield is a useful starting point, but a terrible finishing point. It answers one narrow question: how much income does this stock generate per dollar invested at today’s price? It says nothing about whether that income is sustainable, growing, or at risk.

The investors who build lasting wealth from dividends are the ones who look past the yield and ask harder questions. Is the dividend safe? Is it growing? Can the business sustain it through tough times? What is the payout ratio telling me? Why is the yield where it is?

Use yield to identify candidates. Then do the real work of analyzing the business underneath.

That is going to wrap up our discussion for today.

As always, thank you for taking the time to read this post, and I hope you find something of value on your investing journey.

If I can further assist, please don’t hesitate to reach out.

Until next time, take care and be safe out there,

Dave

If you want to build the skill of analyzing companies on your own, not just follow someone else's picks, that's exactly what School of Investing is for. Join a community of investors learning to think for themselves.

This is an excellent analysis which I plan to use in educating my son and granddaughter about investing.

A high yield always looks like generosity, but it often arrives at the exact moment generosity is least affordable. Price falls first, yield rises second, and the dividend is the last to admit what the market already suspects.

That’s what makes it seductive. It feels like getting paid more for taking less risk, when in reality you’re being offered a larger slice of something that may be shrinking underneath you. The real work isn’t spotting the number, it’s understanding why it’s there. Yield is the invitation. The balance sheet is the answer.