Buybacks vs. Dividends: Two Paths to Returning Cash (and Why Apple Chose Both)

What does a mature, cash-generating business do when it runs out of attractive places to reinvest its own profits?

Every profitable company eventually faces the same question: we made more money than we need, what now? The answer shapes your returns as a shareholder more than most investors realize. In today’s post, we will learn how to think about the two primary ways a company returns cash to owners, when each one makes sense, and how to evaluate whether management is making smart choices. We will use Apple’s fiscal 2025 10-K as our case study, since no company better illustrates the modern approach to capital return.

In today’s post, we will cover:

What Management Actually Does with Free Cash Flow

Dividends: The Predictable Path

Buybacks: The Flexible (and Sometimes Misunderstood) Path

When Buybacks Beat Dividends (and When They Don’t)

Apple: A Case Study in Doing Both

What This Means for Your Investing Process

Okay, let’s dive in.

What Management Actually Does with Free Cash Flow

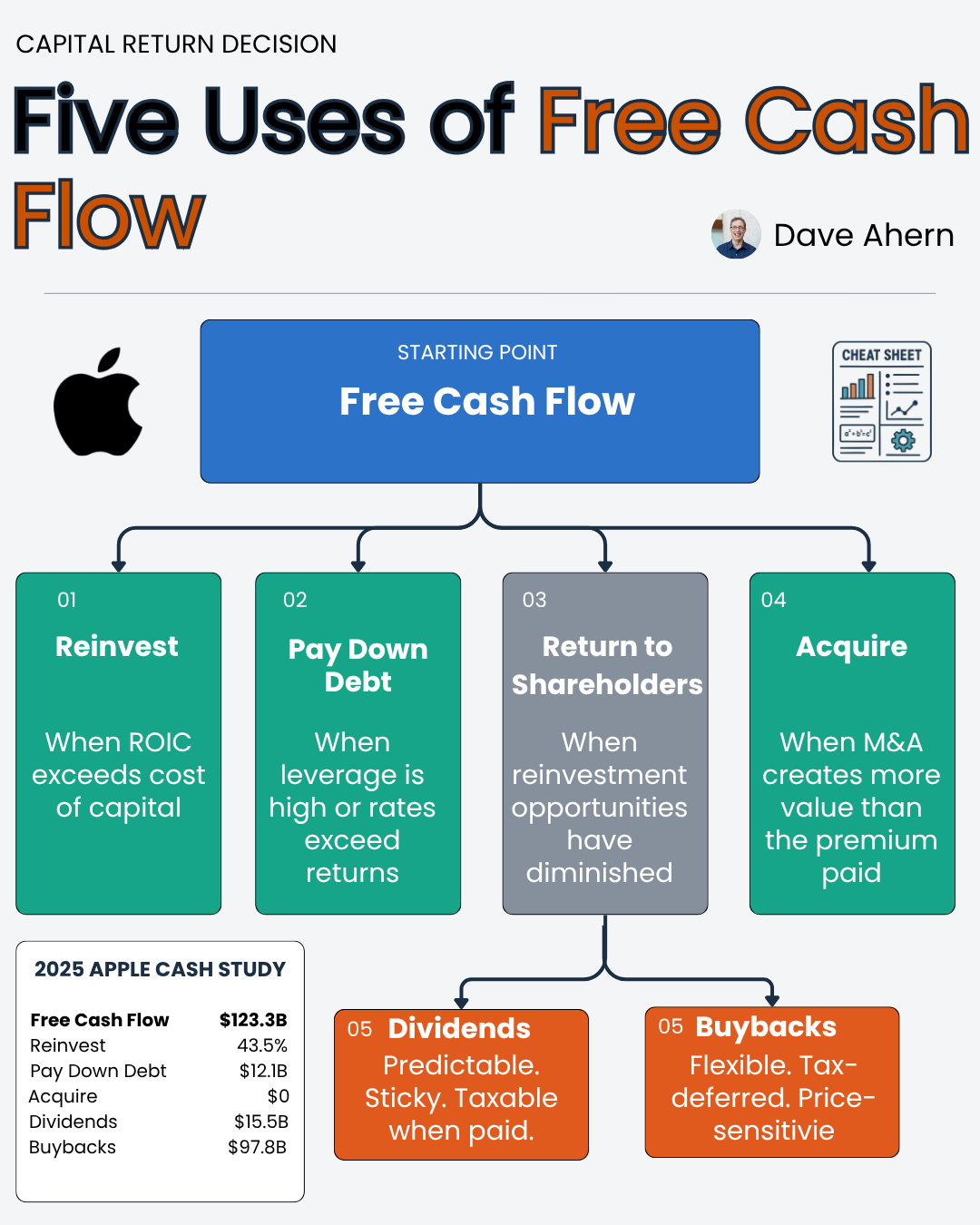

Before we compare buybacks and dividends, we need to zoom out. A company’s CEO has four main options for the free cash flow the business generates each year:

Reinvest in the business (new products, new factories, new markets)

Acquire other businesses

Pay down debt

Return cash to shareholders (through dividends or buybacks)

The first three are value-creating when the returns exceed the company’s cost of capital. When they don’t, returning cash to shareholders becomes the best option. This is the concept Warren Buffett has been hammering on for decades. A business that can reinvest profits at 25% returns should keep the cash. A business that can only reinvest at 5% should return the excess to the owners and let them deploy it elsewhere.

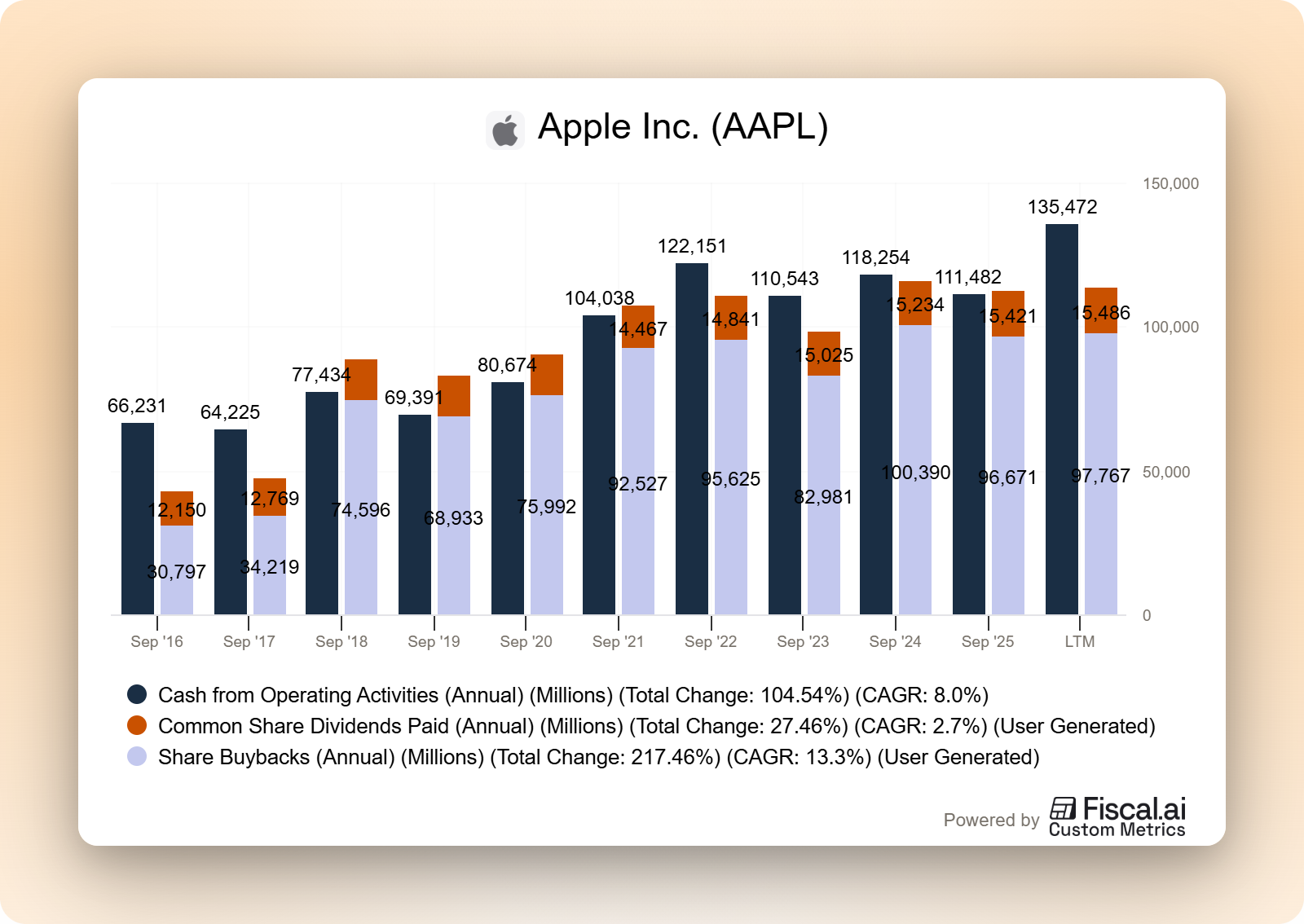

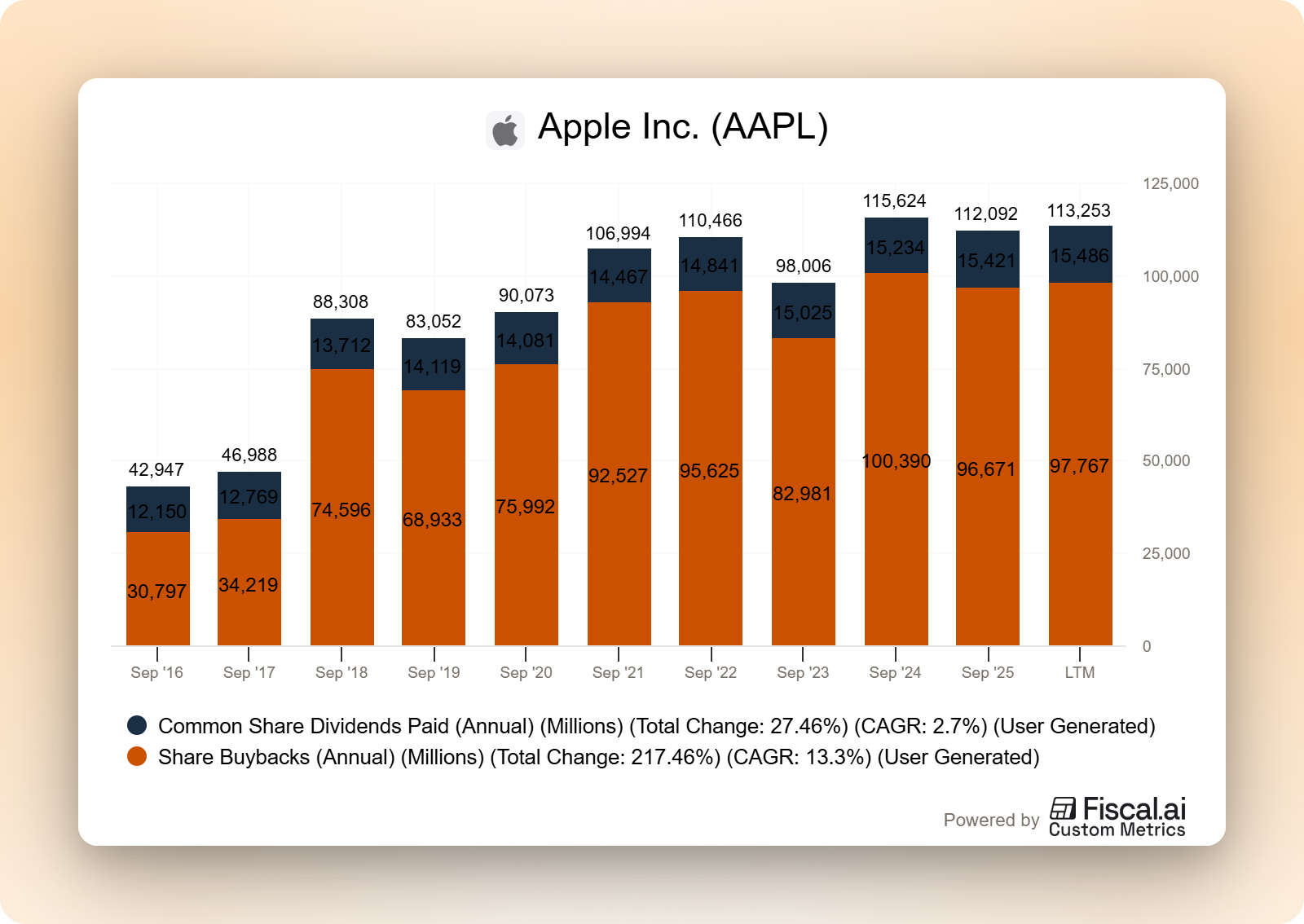

Apple generated $111.5 billion in operating cash flow in fiscal 2025, according to its 10-K for the year ended September 27, 2025. After $12.7 billion in capital expenditures, roughly $98.8 billion remained in free cash flow. Apple’s management decided that the best use of most of it was to return it to shareholders. They sent back $104.7 billion, split between $89.3 billion in buybacks and $15.4 billion in dividends. That is the decision we are going to unpack.

Dividends: The Predictable Path

A dividend is a cash payment that the company sends directly to shareholders on a regular schedule, usually quarterly. If you own 100 shares of Apple and the quarterly dividend is $0.26 per share, you receive $26 deposited into your brokerage account every three months.

The mechanics are simple, but the signaling is powerful. When a company declares a dividend, management is telling the market three things:

We expect to generate enough cash to cover this payment indefinitely

We have more cash than we can productively reinvest

We are committing, at least implicitly, to keep paying (cutting a dividend is brutal for the stock price)

Apple raised its quarterly dividend from $0.25 to $0.26 per share in May 2025, according to its fiscal 2025 10-K. That is a 4% increase and marks the thirteenth consecutive year Apple has raised its dividend since reinstating one in 2012. The 10-K states directly that the company “intends to increase its dividend on an annual basis, subject to declaration by the Board.”

Dividends create a tax event for shareholders in the year they are paid. For most long-term U.S. investors, qualified dividends are taxed at favorable long-term capital gains rates (0%, 15%, or 20% depending on income bracket). But the key point is you cannot defer the tax. When the check hits your account, the IRS takes its cut.

Dividends are also sticky. Management teams know that cutting a dividend signals distress, so they tend to set the level conservatively and raise it slowly. This is why you will see companies pay dividends during rough years, even when it strains the balance sheet.

You are learning to evaluate capital return programs the way an institutional analyst would. Buffett's filters, Apple's SEC filings, the five-question checklist, this is the work most retail investors never do, and it's why they get surprised when management destroys value with poorly timed buybacks. School of Investing is where investors go to stop guessing and start analyzing, with weekly deep dives, calculators, an infographic library, and AI prompts that make it possible.

Buybacks: The Flexible (and Sometimes Misunderstood) Path

A share buyback (also called a share repurchase) is when the company uses its cash to buy its own stock on the open market and retire those shares. If Apple buys back 100 million shares and retires them, there are now 100 million fewer shares outstanding. Your ownership stake and your claim to future earnings grow without you doing anything.

Here is the math that makes buybacks powerful. Imagine a company earns $10 billion in net income with 1 billion shares outstanding. Earnings per share are $10. If the company buys back 100 million shares and net income stays flat at $10 billion, EPS jumps to $11.11 (that is $10 billion divided by 900 million shares). Same company, same profits, but each remaining share now represents 11% more ownership.

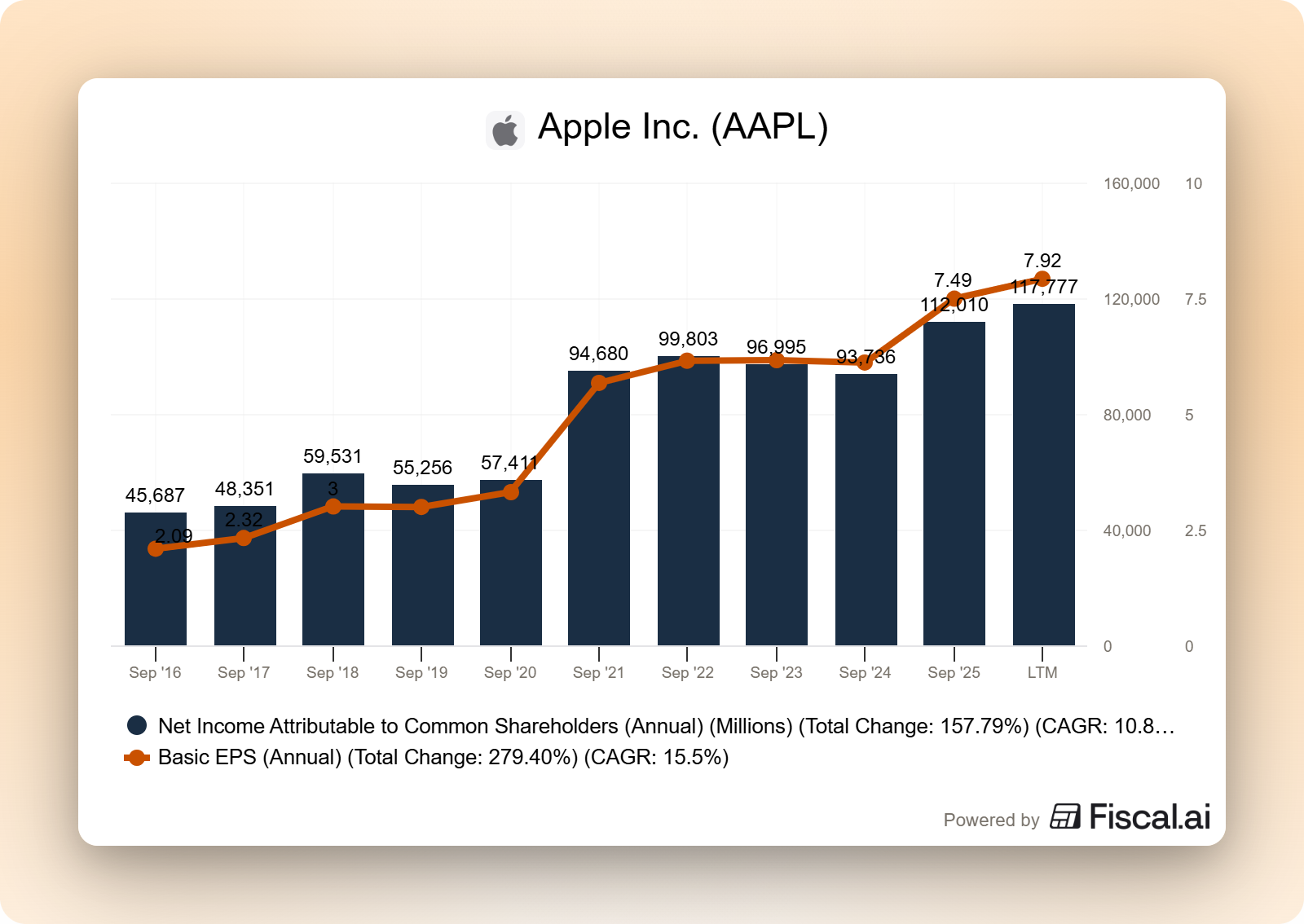

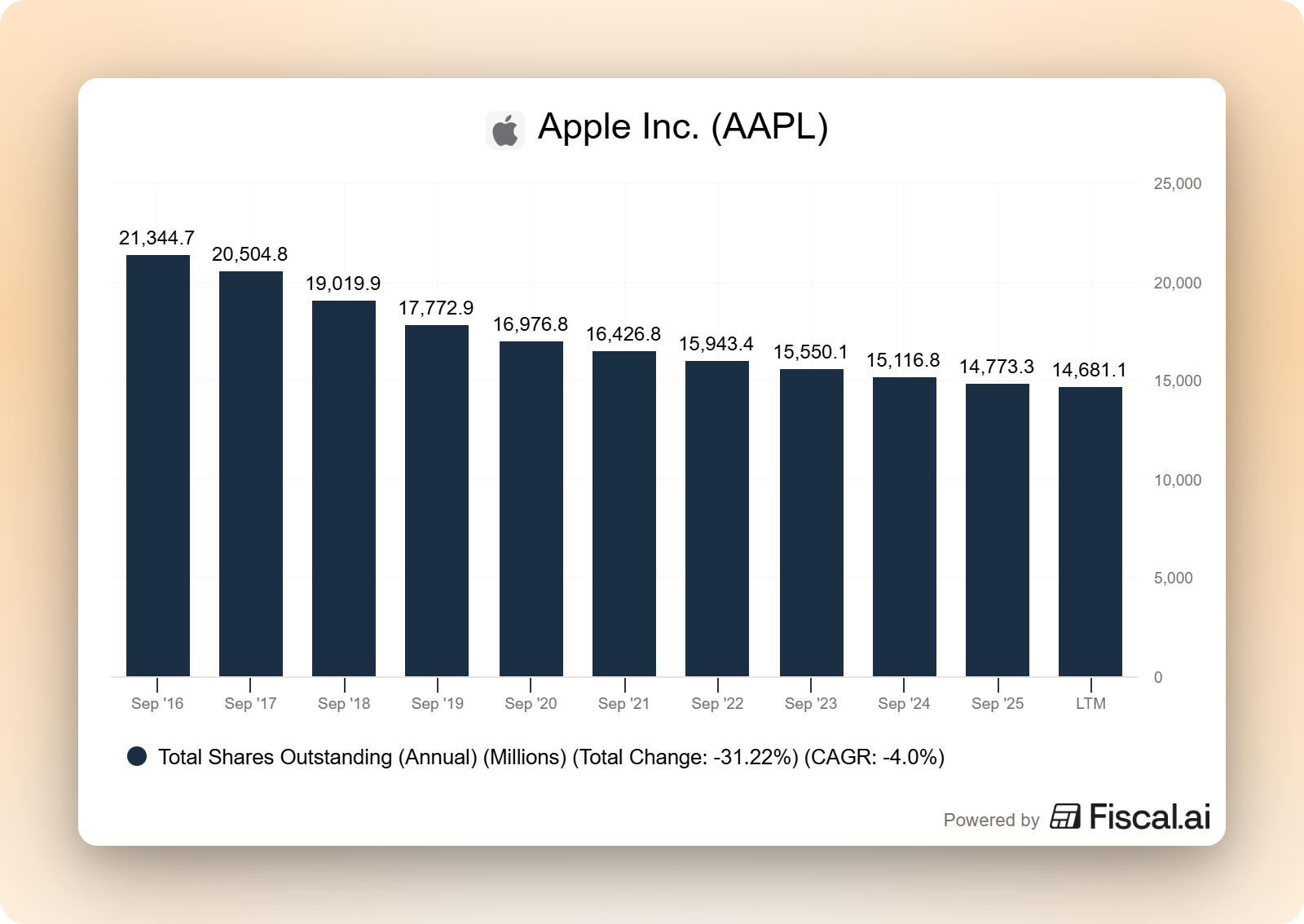

Apple’s fiscal 2025 10-K shows this mechanism at work in real time. The company repurchased 402 million shares for $89.3 billion during the year, bringing total shares outstanding from 15.12 billion at the start of fiscal 2025 to 14.77 billion at year-end. Net income for the year was $112.0 billion, up from $93.7 billion the prior year. But diluted EPS grew even faster, from $6.08 in fiscal 2024 to $7.46 in fiscal 2025. Part of that EPS growth came from fewer shares in the denominator.

Three things make buybacks different from dividends:

They are flexible. Management can speed up, slow down, or pause buybacks without signaling financial distress the way a dividend cut would.

They create no immediate tax event for shareholders. You only owe capital gains tax when you sell your shares.

They only create value when shares are bought at reasonable prices. This is the catch that almost nobody talks about.

That last point deserves its own paragraph. Buybacks transfer wealth from selling shareholders to remaining shareholders. If a company buys back stock at $200 per share and the intrinsic value is $300, the remaining shareholders got a bargain. If the company buys back stock at $300 when it is only worth $200, management just destroyed value.

When Buybacks Beat Dividends (and When They Don’t)

The choice between buybacks and dividends is not either/or in practice, but the trade-offs matter.

Buybacks tend to win when:

The stock trades below intrinsic value (management can buy $1 of value for $0.80)

Shareholders prefer to defer taxes

The company wants flexibility to adjust capital return based on market conditions

Management wants to offset dilution from stock-based compensation

Dividends tend to win when:

The stock trades above intrinsic value (buybacks would destroy value; a dividend returns cash at par)

Shareholders want predictable income (retirees, income-focused funds)

The business is mature enough to commit to regular payments

Management wants to signal discipline and long-term confidence

The most common critique of buybacks is that management teams are notoriously bad at timing them. Companies tend to buy back heavily when times are good, and their stock is expensive, then pull back during downturns when shares are cheap. That is the opposite of what creates value. A 2019 Harvard Business Review study found that the S&P 500’s buyback yield peaks near market tops and declines during corrections.

The second critique is that buybacks can mask weakness. A company with flat net income can still show EPS growth by buying back shares. If you only look at EPS, you might miss that the underlying business is not actually growing.

This is why I look at both net income growth and share count trend separately when I evaluate a company. If earnings are flat and EPS growth is coming entirely from buybacks, that is a very different story than a business growing earnings and reducing share count.

Apple: A Case Study in Doing Both

Apple is the textbook example of a mature, cash-generating business using both tools aggressively. Here is what the capital return program looked like over the last three fiscal years, pulled directly from the fiscal 2025 10-K cash flow statement:

The pattern is clear. Apple returns nearly all of its operating cash flow to shareholders, with roughly 85% going to buybacks and 15% to dividends. That split is deliberate.

On May 1, 2025, Apple’s board authorized a new $100 billion share repurchase program, on top of completing the previous $110 billion authorization announced in May 2024. According to the fiscal 2025 10-K, Apple utilized the final $19.8 billion of the May 2024 program during the fourth quarter and had used only $221 million of the new $100 billion program by year-end. That means Apple entered fiscal 2026 with roughly $99.8 billion of buyback authorization still to deploy.

The impact on share count has been dramatic. Apple’s diluted share count fell from 15.81 billion in fiscal 2023 to 15.00 billion in fiscal 2025. That is a reduction of roughly 810 million shares, or about 5%, in two years. Each remaining Apple share now represents a meaningfully larger claim on the company’s earnings than it did three years ago.

Why does Apple lean so heavily on buybacks instead of paying a larger dividend? A few reasons worth noting:

Apple’s stock has compounded strongly. Per the 10-K’s five-year total return comparison, $100 invested in Apple on September 25, 2020, grew to $234 by September 27, 2025. Buying back shares at reasonable (if not cheap) prices has worked out for remaining shareholders.

Flexibility matters at Apple’s scale. A larger dividend would be harder to adjust if the business environment changed. Buybacks can flex.

Tax efficiency. Apple’s shareholders include many long-term holders who would rather defer capital gains than pay dividend taxes each quarter.

Offsetting stock-based compensation. Apple expensed $12.9 billion in share-based compensation in fiscal 2025 per the 10-K. Without ongoing buybacks, the share count would creep up, diluting existing shareholders.

Apple’s approach is not perfect. Valuation matters: buybacks at elevated multiples return less per dollar than those at cheap multiples. But the company’s capital return program is disciplined, transparent, and massive.

What This Means for Your Investing Process

When you evaluate a company’s capital return program, here is what I look for:

Does the company generate more free cash flow than it can reinvest profitably? If not, neither dividends nor buybacks are appropriate. Management should reinvest in the business.

If the company pays a dividend, is it covered by free cash flow with room to spare? A payout ratio above 90% of free cash flow is a warning sign.

If the company buys back shares, is the share count actually declining? Some companies “buy back” shares only to offset dilution from stock-based compensation. Check the share count trend, not just the buyback dollars.

Is management buying back shares at reasonable prices? Compare the average repurchase price to your estimate of intrinsic value. Apple’s fiscal 2025 10-K shows the company paid an average of $210.43, $224.25, and $238.56 per share in the three months of its fourth quarter. Whether those were good prices depends on your view of Apple’s intrinsic value.

Is the total capital return program sustainable? Add up dividends and buybacks and compare to operating cash flow. For Apple in fiscal 2025, $106.1 billion was returned against $111.5 billion in operating cash flow. That is sustainable.

The companies I want to own are those that generate far more cash than they need, return most of it to shareholders, and do so with discipline. Apple hits all three. Not every business can.

One important limitation: This framework applies to mature, profitable businesses. A young, fast-growing company should almost never pay dividends or buy back shares. If a business can reinvest at 25% returns, keep every dollar in the business. The capital return question only becomes interesting when the company’s internal reinvestment opportunities have diminished.

The core insight from Buffett applies here, too. The best businesses are those that can retain and reinvest at high rates of return. The next-best are those that cannot find enough high-return reinvestment opportunities but have disciplined management willing to send excess cash back. Apple is now in the second category, and its shareholders are better off because management understands it.

That is going to wrap up our discussion for today.

As always, thank you for taking the time to read this post, and I hope you find something of value on your investing journey.

If I can further assist, please don’t hesitate to reach out.

Until next time, take care and be safe out there,

Dave

You now know how to tell the difference between a company returning cash with discipline and one destroying value with poorly timed buybacks. That's a skill most investors never develop. Do this every week for a year, across dividends, buybacks, moats, valuation, capital allocation, and you become the analyst you used to rely on. That is what the School of Investing is built for.