AT&T Cut Its Dividend 47% in 2022. Here Are the 5 Mistakes Behind It.

The five questions every dividend investor should ask before chasing a headline yield.

A 9% dividend yield can look like easy money next to a 3% payer. But that 9% is usually trying to tell you something, and most dividend investors learn the lesson the hard way.

Today I will walk you through the five most common mistakes I see dividend investors make, with the fix for each one. By the end, you will have a checklist you can run before you click buy on any income stock.

In today’s post, we will discuss:

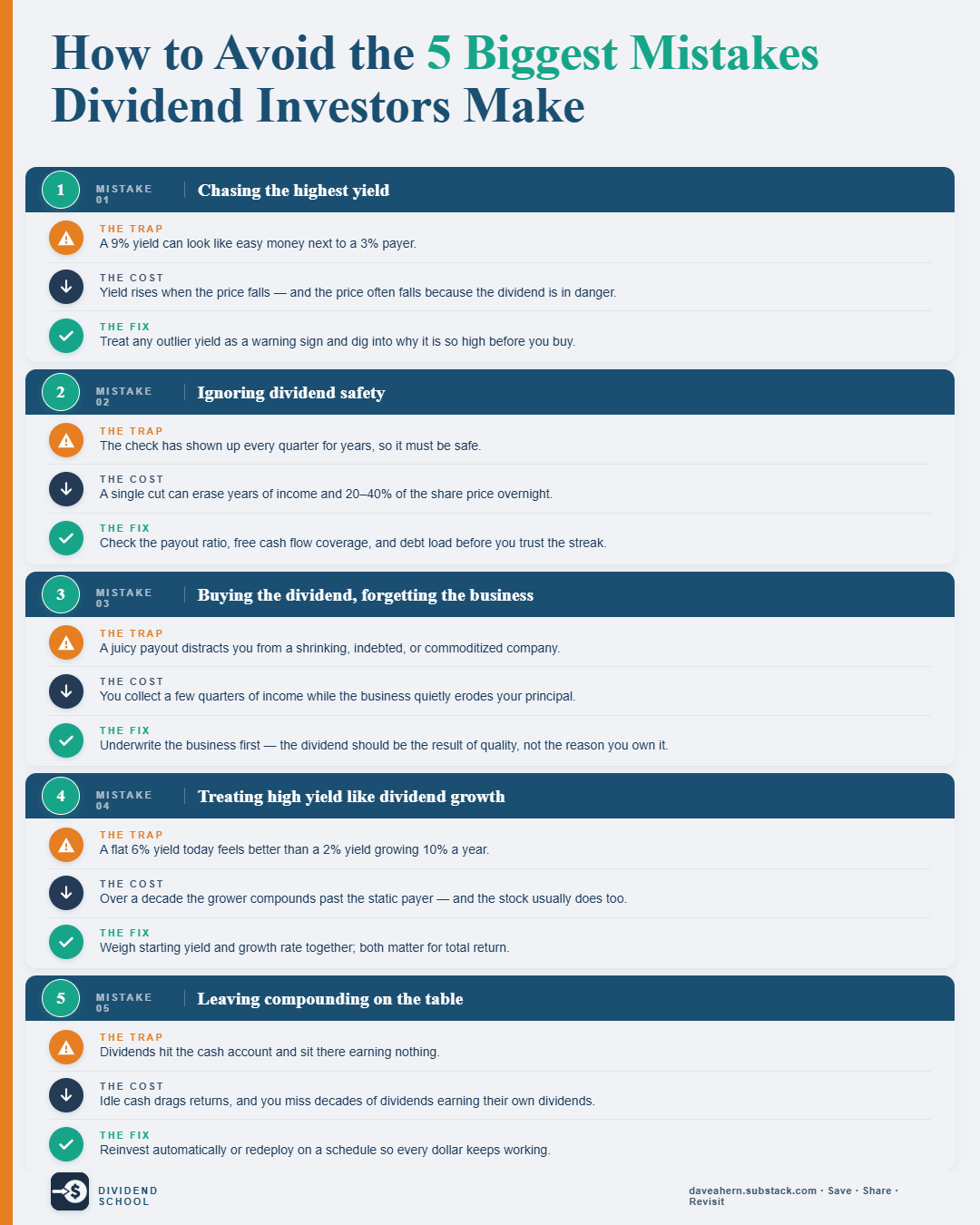

Mistake 1: Chasing the highest yield

Mistake 2: Ignoring dividend safety

Mistake 3: Buying the dividend and forgetting the business

Mistake 4: Treating a high yield like dividend growth

Mistake 5: Leaving compounding on the table

Okay, let’s dive in and learn how to avoid the biggest dividend mistakes.

Mistake 1: Chasing the highest yield

The trap is simple. A 9% dividend yield looks like free money, especially when the rest of the market pays 3%.

But yield is a math problem.

Yield equals annual dividend divided by share price. When the share price falls, the yield rises. And share prices often fall because the dividend itself is in trouble.

This is the textbook “yield trap.” A stock yielding double the market average is rarely a generous payer. The market has already discounted the stock, anticipating a cut.

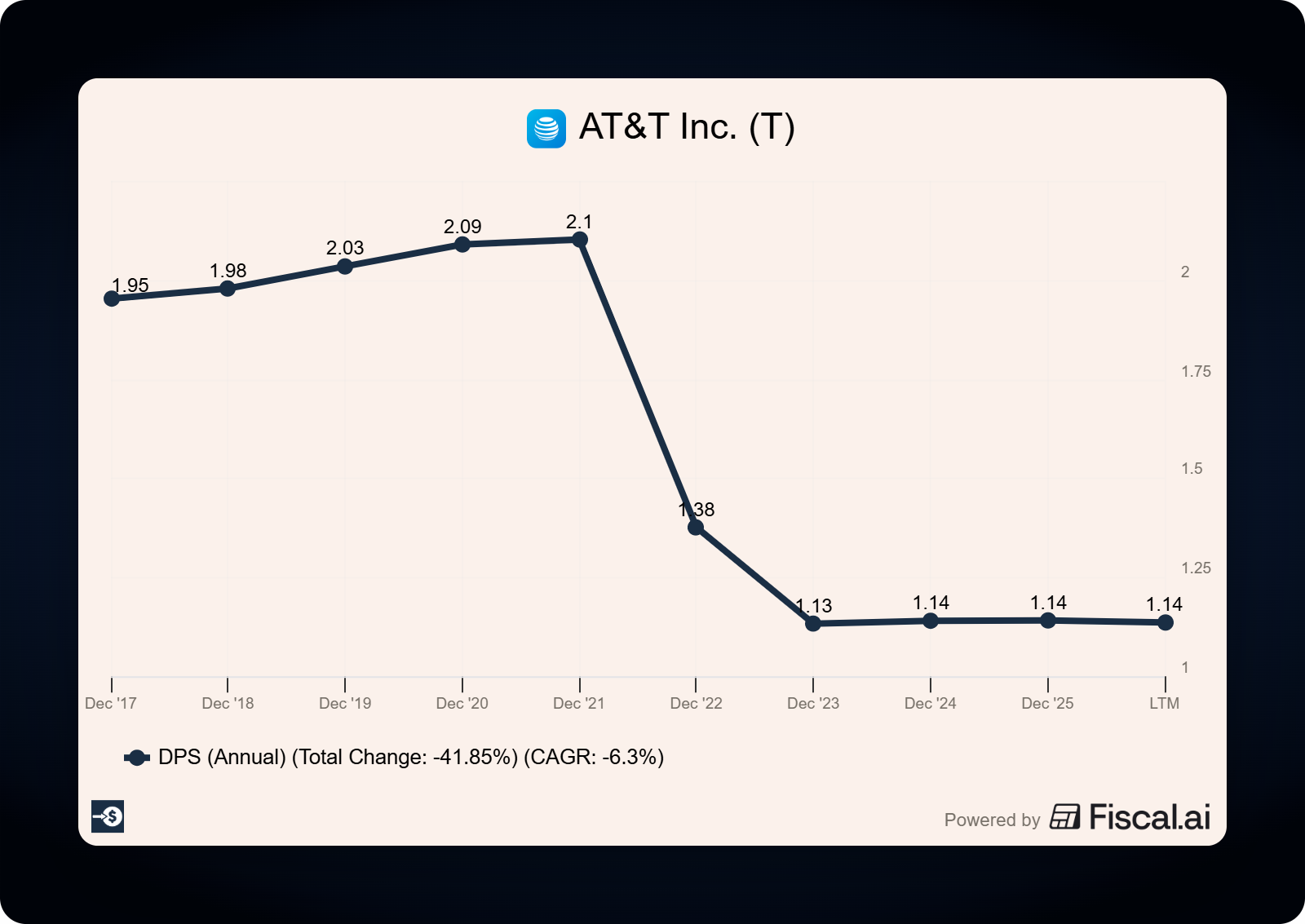

A famous case study is AT&T. In early 2022, the stock yielded well above 8% and looked like a bargain to income investors. Then in April 2022, AT&T spun off WarnerMedia and reset its annual dividend from $2.08 to $1.11 per share, a 47% reduction. Investors who bought for the headline yield woke up with both a smaller dividend and a lower stock price.

The fix: treat any outlier yield as a warning sign. When you see a yield that looks too good, your first question is not “how do I get more of this.” It is “what does the market know that I don’t yet?”

Mistake 2: Ignoring dividend safety

This is the cousin of Mistake 1. Investors see the yield, smile, and skip the boring part. Can the company actually afford the payout?

The number you want is the payout ratio.

Payout ratio equals dividends paid divided by earnings (or free cash flow). It tells you what percentage of profit goes to the dividend.

A payout ratio above 100% means a company is paying out more than it earns. That math runs out. Eventually, the company cuts the dividend, takes on debt to fund it, or both.

Two examples make the point.

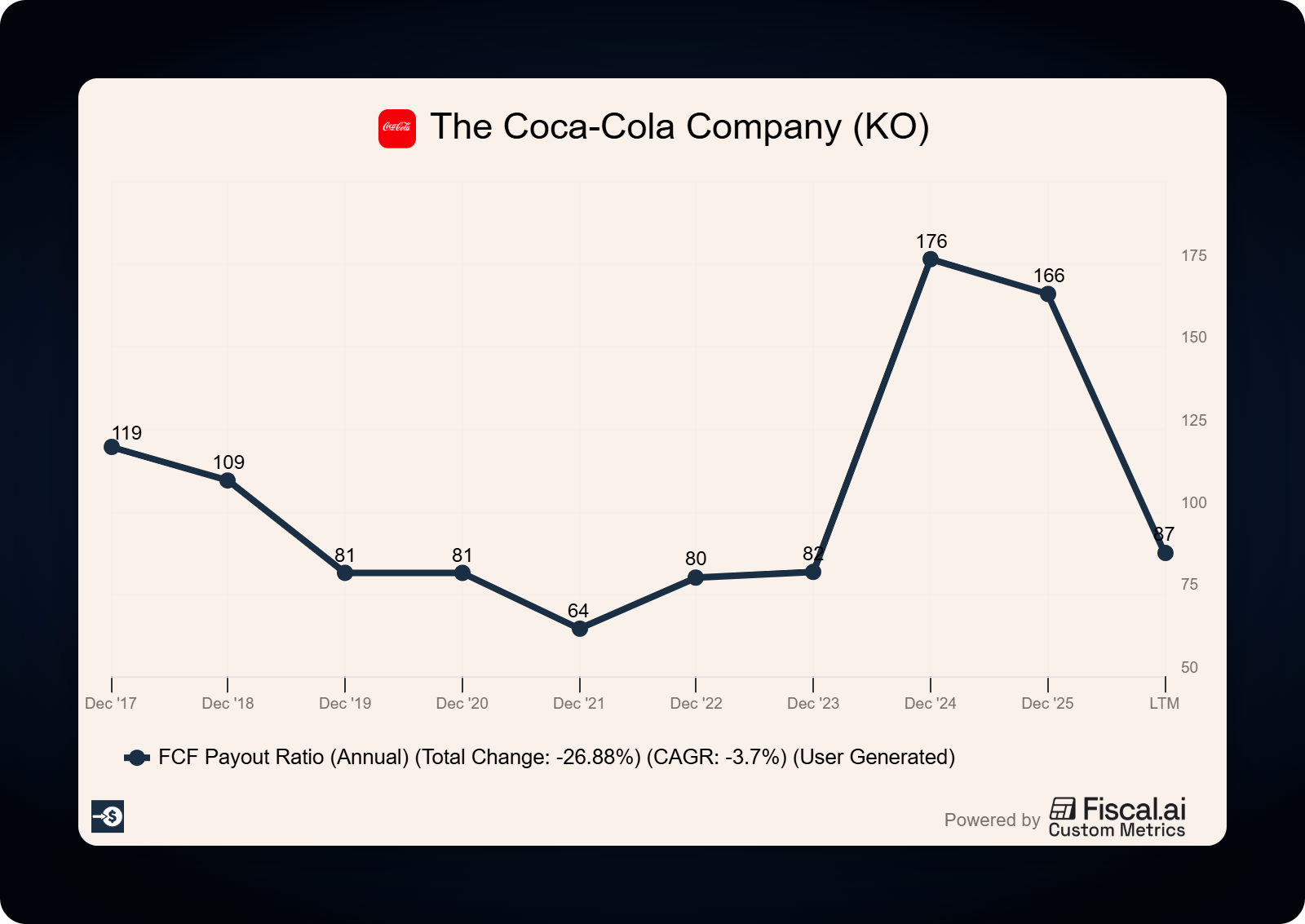

Coca-Cola pays out roughly 70% of its free cash flow as dividends. The remaining 30% funds capital expenditure, share repurchases, and the occasional bolt-on acquisition. That cushion is what lets Coke survive a soft year without touching the payout.

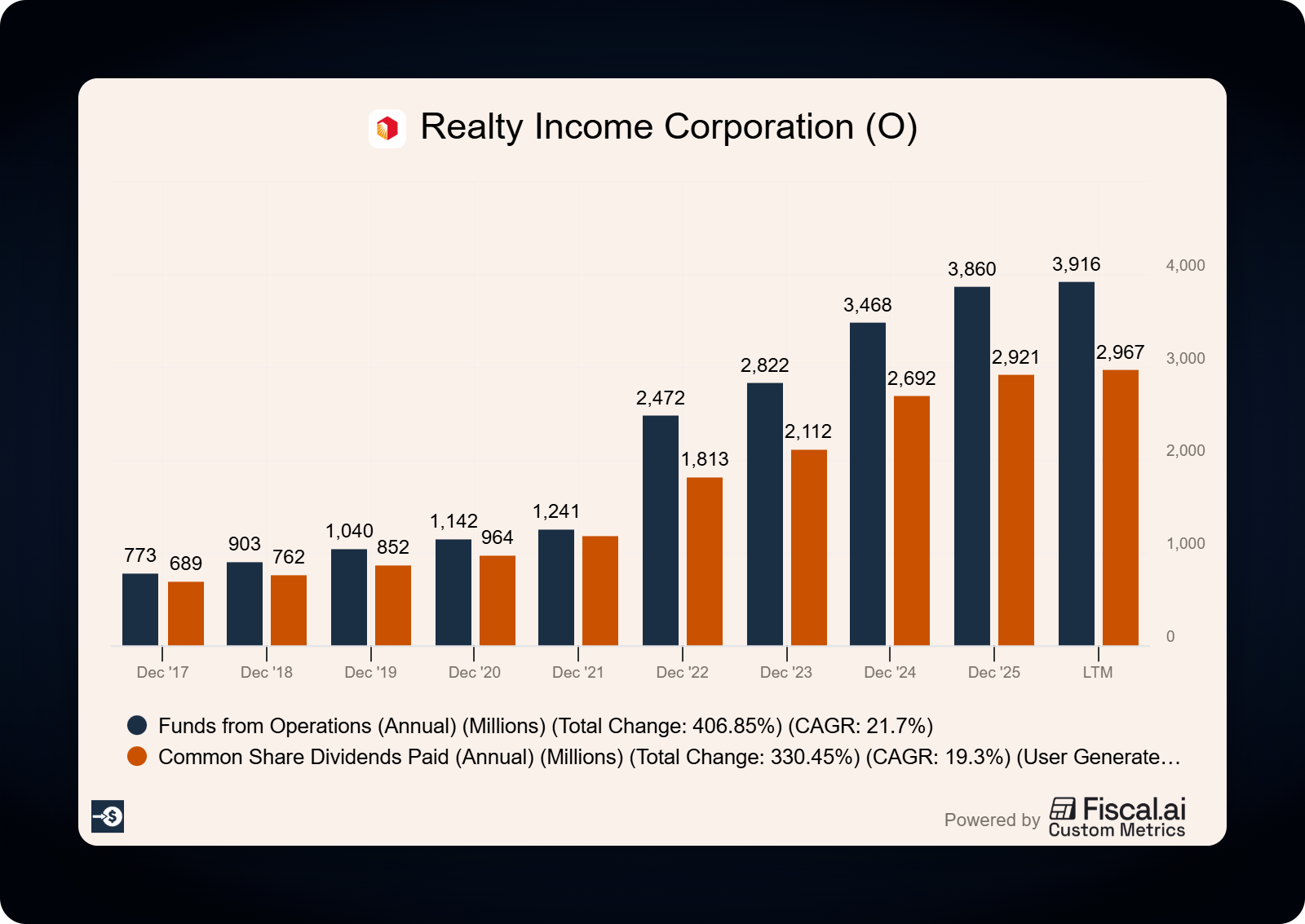

REITs work differently. They must distribute at least 90% of taxable income by law, which makes the standard payout ratio useless. For REITs, look at the AFFO payout ratio instead. Realty Income’s AFFO payout ratio sat at roughly 75% in fiscal 2024, leaving room for the company to keep growing the dividend.

The fix: before you buy the yield, run the math on coverage. The three ratios I look at:

Payout ratio on earnings, ideally under 80% for most companies

Payout ratio on free cash flow, ideally under 80%

For REITs, AFFO payout ratio in the 70% to 85% range

If the dividend is barely covered today, the dividend is barely covered. There is no safety net underneath it.

Do you want to catch a dividend trap before it cuts your income? Do you want to run this same six-point checklist on your own watchlist? Do you want one new company deep-dive in your inbox every Sunday? The paid tier is here.

Mistake 3: Buying the dividend and forgetting the business

This one bites a lot of new dividend investors.

The dividend becomes the whole thesis. The company behind it gets ignored.

But a dividend is only as durable as the business paying it. Weak businesses cut. Strong businesses raise.

General Electric is the textbook cautionary tale. For decades, GE was a dividend stalwart in nearly every income portfolio in America. By the mid-2010s, the business had quietly deteriorated, weighed down by GE Capital and a long list of strategic missteps. In November 2017, GE cut its quarterly dividend from $0.24 to $0.12. A year later, the dividend was cut again to a single penny per share. Investors who bought GE for the income lost both the dividend and most of their capital.

What were they missing? The business itself was eroding. Return on invested capital was falling. Cash flow was unreliable. The dividend was a symptom of a healthy past, not a healthy present.

The fix is the same fix Buffett has been preaching for 60 years. Buy good businesses first and the dividend takes care of itself.

Specifically, I want to see:

Stable or growing revenue across a full economic cycle

Strong free cash flow generation that funds the dividend with room to spare

ROIC consistently above the cost of capital

A real moat (brand, network effects, scale, or switching costs)

A management team that allocates capital sensibly

Get the business right and the dividend follows.

Mistake 4: Treating a high yield like dividend growth

A 6% flat payer can look better than a 2% payer that raises its dividend every year. The 6% wins today. But the math gets interesting fast.

Compare two stocks.

Stock A pays a 6% yield with zero growth. Year ten, you still earn 6% on your original investment.

Stock B pays a 2% yield and grows the dividend 10% annually. By year ten, your yield on cost is around 4.7%. By year fifteen, it sits at roughly 7.6%. By year twenty, it is over 12%.

That second math is the snowball Buffett talks about. He bought Coca-Cola shares starting in 1988 at an average split-adjusted cost of around $2.45 per share. Coke pays roughly $2 per share in annual dividends today. Buffett’s yield on cost on those original shares is approaching 80% per year, every year, before he sells a single share.

The fix: weigh dividend growth alongside yield. A useful starting screen:

Dividend growth rate over the last 5 and 10 years

Years of consecutive dividend increases (Dividend Aristocrats have 25+, Kings have 50+)

Payout ratio trend (if it is climbing toward 100%, growth is borrowed time)

Earnings growth (the dividend can only grow as fast as profits over the long run)

A small yield on a fast-growing dividend will usually beat a large yield on a stagnant one. The compounding is the whole game.

Mistake 5: Leaving compounding on the table

The last mistake is the most common and the most expensive.

Dividends get spent or sit in cash, often in a taxable account. Then investors wonder why their total return looks nothing like the long-run studies they read.

The math here is brutal.

Going back to 1926, roughly 40% of the S&P 500’s total return has come from dividends, and a meaningful share of that comes from reinvesting those dividends, not just collecting them. Reinvested dividends buy more shares. Those shares pay their own dividends. That second layer buys still more shares. The snowball builds on itself.

If you are still in your accumulation phase, take the dividends and put them back to work. Most brokerages let you set up a Dividend Reinvestment Plan (DRIP) that does this automatically and commission-free.

A few practical notes:

DRIPs let you buy fractional shares, so every penny goes to work

In tax-advantaged accounts (IRA, Roth, 401k), reinvested dividends compound tax-free or tax-deferred

In a taxable account, you still owe tax on the dividend even if it is reinvested

REIT dividends are usually taxed as ordinary income, which makes a Roth or IRA the right home for them

The fix is straightforward. Hold dividend payers in tax-advantaged accounts when you can. Reinvest while you are still building wealth. Once you need the income, switch off the DRIP and take the cash. Until then, let it compound.

The through-line

All five mistakes share one root cause.

They come from buying a number on a screen and skipping the company behind it. A healthy company produces a strong dividend. The yield is just the receipt.

Safe, growing dividends come from strong businesses bought at fair prices. Everything else is noise around that core idea.

The dividend investor’s checklist

Save this and run through it before any dividend buy.

Yield check. Is the yield reasonable relative to the company’s history and peers? An outlier yield is a question, not an answer.

Coverage check. Is the payout ratio under 80% on both earnings and free cash flow (or 70% to 85% on AFFO for REITs)?

Business check. Does the company have a real moat, stable free cash flow, and ROIC above its cost of capital?

Growth check. Has the dividend grown over the last 5 to 10 years, and at what rate?

Price check. Is the valuation reasonable on FCF yield, P/FFO, or your preferred tool?

Account check. Am I holding this in a tax-advantaged account where it makes sense, and am I reinvesting?

If you can check all six boxes, you have a candidate worth deeper work.

Investor takeaway

Dividend investing is one of the slowest, surest ways to build wealth, but only if you respect the underlying business. The number on the screen is the consequence of a healthy company, never a substitute for one.

Find good businesses. Verify the dividend is covered. Reinvest while you build. Be patient with the snowball.

That is going to wrap up our discussion for today.

As always, thank you for taking the time to read this post, and I hope you find something of value on your investing journey.

If I can further assist, please don’t hesitate to reach out.

Until next time, take care and be safe out there,

Dave

You just learned the 6-point checklist I run on every dividend stock before I buy. Paid subscribers get a new company deep-dive every Sunday, the dividend safety calculators, the AI prompts I use to read 10-Ks, and the full infographic library.